Monday Jul 13, 2026

Monday Jul 13, 2026

Monday, 20 December 2021 04:31 - - {{hitsCtrl.values.hits}}

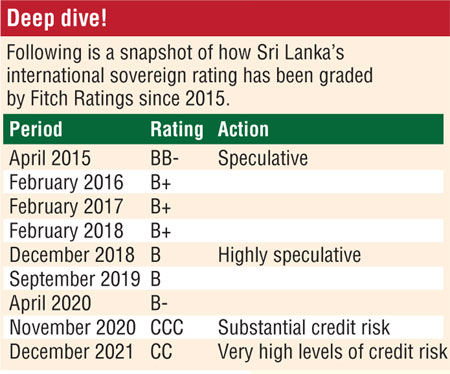

The Government on Saturday faulted and strongly disputed what it described as “hurried” downgrading of Sri Lanka's international sovereign rating to CC (Very high levels of credit risk) from CCC (Substantial credit risk).

The Government on Saturday faulted and strongly disputed what it described as “hurried” downgrading of Sri Lanka's international sovereign rating to CC (Very high levels of credit risk) from CCC (Substantial credit risk).

In a statement the Government said Fitch Ratings in its “hasty move” demonstrating its failure to recognise the positive developments taking place in Sri Lanka, in an environment in which the entire world is grappling with multiple waves of the COVID-19 pandemic.

“This action resembles the recent unwarranted downgrade by Moody’s Investors Service a few days prior to the announcement of the National Budget 2022. The sense of urgency on the part of an internationally recognised rating agency to downgrade Sri Lanka is inconceivable, particularly considering the fact that Fitch was being constantly updated by Sri Lankan authorities on the latest developments in all sectors of the economy and imminent foreign exchange inflows.

“In particular, despite the lockdown measures that had to be introduced in the third quarter of 2021, the real economy averted a deep contraction during the quarter, signalling Sri Lanka’s adaptability to the new normal. Real GDP, in fact, expanded by 4.4% (year-on-year) during January-September 2021, reaffirming the strong possibility of above 4% growth in 2021.

“High frequency data on activity point towards a strong recovery of the economy surpassing the pre-pandemic level. The Manufacturing Purchasing Managers’ Index reached 61.9 in November 2021, the highest reading for a month of November on record, and way above the pre-pandemic level of activity.

“Indices of the Colombo Stock Exchange reached historical highs, with a large number of Initial Public Offerings taking place in 2021. Credit extended to the private sector expanded by over Rs. 685 billion in the 10 months to October 2021, compared to about Rs. 260 billion in the same period last year.

“The trade deficit continued to decline from May 2021 on a month-on-month basis, supported by record high export earnings. Earnings from merchandise exports recorded an all-time high in October 2021, and preliminary information indicates that earnings have exceeded this record level in November 2021.

“With the exchange rate remaining stable since April 2021, excepting a few speculation-driven deviations, the conversion of export proceeds and other foreign exchange earnings has also improved substantially in recent weeks. An exponential growth in tourist arrivals is observed on a monthly basis, indicating an early reversal of the annual foreign exchange revenue loss of around $ 5 billion in the period ahead.

“The prospects for workers’ remittances are bright, with the resumption of worker migration, increased demand for Sri Lankan workers particularly from the Middle East and efforts to facilitate worker remittances through formal channels through an attractive incentive package.

“With such measures, the external current account balance is expected to be maintained at growth supporting levels, thereby accommodating equity capital to the financial account through direct investment to the identified projects in the Colombo Port City and Industrial Zones, in addition to the expected monetisation of non-strategic and underutilised assets. These developments and the rapid vaccination drive, which is being rolled out nationally, would help realise the potential of the economy over the near to medium term.

“Fitch has also failed to recognise the fiscal reforms introduced through the National Budget 2022. With the introduction of new tax measures, upgraded tax administration systems, and the revival of the economy, the year 2022 is expected to deliver a substantial increase in Government revenue.

“Increasing the retirement age of public sector employees and measures to enhance the viability of State-owned business enterprises are notable reforms and issuing quarterly warrants for Government institutions instead of annual warrants are expected to instil financial discipline in the utilisation of the allocations, thereby cushioning the expenditure side.

“Such revenue and expenditure side measures would pave the way for a reduction in the fiscal deficit and financing needs of the Government, contributing to a sustainable debt level.”

The domestic market has responded positively to the expected path of fiscal consolidation, and interest rates have stabilised, following an initial overshooting, at market clearing levels. The Central Bank’s holdings of Government securities have also declined notably as a result of improved subscription at primary market auctions and active open market operations.

“Contrary to Fitch’s unfounded claims on increased probability of a default event over the coming months, the measures undertaken by the Government and the Central Bank to secure support from friendly nations in the region are nearing fruition, thereby offsetting pressures on the balance of payments in the period ahead.

“The Six-Month Road Map for Ensuring Macroeconomic and Financial System Stability clearly articulated the expected cash flows by December 2021 and by March 2022, and the Government and the Central Bank remain confident that these inflows will materialise, and the end-2021 level of Gross Official Reserves will remain above $ 3 billion.

“Fitch appears to have completely ignored the standby SWAP facility with the People’s Bank of China of around $ 1.5 billion, of which the withdrawal is imminent. The credit lines and other inflows expected following high-level meetings in India, the Middle East and other regional economies are also not given due consideration by Fitch in arriving at this decision.

“The fact that Fitch Ratings decided to downgrade Sri Lanka without waiting until the first test date of 31 December 2021 shows nothing but recklessness, which could only hurt investors if decisions are made based on this downgrade.

“It must also be noted that the Government has given a clear assurance that Sri Lanka will honour all debt obligations in the period ahead, and Sri Lanka has not delayed a single payment even under severe stresses that were caused by the COVID-19 pandemic over the past two years.

“Therefore, all stakeholders of the economy, including international investment partners, are requested not to be dissuaded by this unjustified rating action, but instead, work with Sri Lanka to surf the turbulent tides, which are expected to settle in the next few days. A detailed press release on the progress of expected foreign inflows as envisaged in the Six-Month Road Map will be published this week.”

Inflicting a big blow, Fitch Ratings has downgraded Sri Lanka's Long-Term Foreign-Currency Issuer Default Rating (IDR) to ‘CC’, from ‘CCC’, the second negative development for the country in almost a year.

It said the downgrade reflects its view of an increased probability of a default event in the coming months, in light of Sri Lanka's worsening external liquidity position, underscored by a drop in foreign-exchange reserves set against high external debt payments and limited financing inflows. The severity of financial stress is illustrated by elevated Government bond yields and downward pressure on the currency.

“We have affirmed the Long-Term Local-Currency IDR at ‘CCC,’ as authorities have continued access to domestic financing, despite high and still-rising Government debt and an elevated debt service burden,” Fitch said.

It said Sri Lanka's foreign-exchange reserves had declined much faster than Fitch expected at its last review, owing to a combination of a higher import bill and foreign currency intervention by the Central Bank of Sri Lanka.

“Foreign exchange reserves have declined by about $ 2 billion since August, falling to $ 1.6 billion at end-November, equivalent to less than one month of current external payments (CXP). This represents a drop in foreign-currency reserves of about $ 4 billion since end-2020,” Fitch said.

“We believe it will be difficult for the Government to meet its external debt obligations in 2022 and 2023 in the absence of new external financing sources. Obligations include two international sovereign bonds of $ 500 million due in January 2022 and $ 1 billion due in July 2022.

“The Government also faces foreign-currency debt service payments, including principal and interest, of $ 6.9 billion in 2022, equivalent to nearly 430% of official gross international reserves as of November 2021. Cumulative foreign currency debt service, including interest and principal, amounts to about $ 26 billion from 2022 through to 2026.”

The timing and availability of external resources is unclear and may not be readily available for debt service. The Central Bank published a six-month roadmap in October that outlined plans to raise additional external borrowings through a number of channels, including bilateral and multilateral sources, syndicated loans and through the monetisation of underutilised assets in 1Q22.

A drawdown on the existing currency swap facility with the People's Bank of China (PBOC) could boost reserves by up to CNY10 billion ($ 1.5 billion equivalent). However, even with resources from the swap facility, foreign exchange reserves are likely to remain under pressure, in Fitch’s view.

Additional sources of financing could come from an economic support package from India, which contains a swap facility under the South Asian Association for Regional Cooperation (SAARC) currency framework of $ 400 million, a swap facility with the Qatar Central Bank, remittances securitisation and a revolving credit facility with the Bank of China Limited (A/Stable).

However, even if all these sources are secured, Fitch believes it will be challenging for the Government to maintain sufficient external liquidity to allow for uninterrupted debt servicing in 2022.

Press reports suggest the Government may be contemplating IMF financing; an IMF program would unlock multilateral financing, but Fitch believes the Fund could well suggest restructuring to bring about debt sustainability.

“Sri Lanka's external finances are further challenged by a persistent current account deficit, resulting in downward pressure on the exchange rate. We estimate that the deficit widened to about 5.7% of GDP in 2021 and expect it to remain at about 4% in 2022, before falling to 2.1% by 2023.

“A plunge in remittances, a weak tourism recovery and rising imports have contributed to the wider current account deficit. Travel and tourism, an important economic driver, has been hit hard by the COVID-19 pandemic and the outlook for a recovery remains uncertain given the emergence of new highly transmissible virus variants.”

The rupee/dollar spot exchange rate depreciated by 7-8% since end-2020, and the Central Bank intervened to support the currency, exacerbating the decline in reserves.

“Wide fiscal deficits continue to worsen the outlook for debt sustainability. The 2021 fiscal deficit target of 8.9% of GDP was missed by a wide margin, and we expect the Government deficit to widen to about 11.5% of GDP in 2022.

“We believe 2022 revenue targets are optimistic, especially in light of our expectation of weak economic activity. We forecast general Government debt to reach about 110% of GDP by 2022, and to keep rising under our baseline, absent major fiscal consolidation.

“We also believe it is unlikely that Sri Lanka will meet its 2025 Government debt reduction target of about 89% of GDP or narrow the fiscal deficit to 4.8% of GDP. Rising interest payments are a major driver of the widening deficit and the interest/revenue ratio of at about 95% is well above the peer median of 11.3%.

“Sri Lanka's economic performance is likely to weaken in 2022, as the challenging external position and exchange-rate pressure will have knock-on effects on economic activity. Foreign currency shortages in 2021 hampered food and fuel imports, and continued external liquidity stress could worsen supply shortages, hurting economic activity.

“We expect growth to slow to 2% in 2022, from an estimated 3.6% in 2021, before recovering to 4.3% in 2023 partly due to base effects and a gradual easing of domestic pressures, although downside risks to our forecasts remain. Sri Lanka's economy was expanding at a modest pace prior to the pandemic, which led real GDP to contract by 3.6% in 2020.”

ESG – Governance: Sri Lanka has an ESG Relevance Score of ‘5’ for Political Stability and Rights. “This reflects the high weight that the World Bank Governance Indicators (WBGI) have in our proprietary Sovereign Rating Model.

“Sri Lanka has a medium WBGI ranking at the 47th percentile, reflecting a recent record of peaceful political transitions and a moderate level of rights for participation in the political process. As Sri Lanka has a percentile rank below 50 for the governance indicator, this has a negative impact on the credit profile.”

ESG – Governance: Sri Lanka has an ESG Relevance Score of ‘5[+]’ for the Rule of Law, Institutional and Regulatory Quality and Control of Corruption. “This reflects the high weight that the WBGI has in our proprietary Sovereign Rating Model.

“Sri Lanka has a medium WBGI ranking at the 53rd percentile, reflecting moderate institutional capacity, established rule of law and a moderate level of corruption. As Sri Lanka has a percentile rank above 50 for the respective governance indicators, this has a positive impact on the credit profile.”

Sri Lanka has an ESG Relevance Score of ‘5’ for Creditor Rights, as willingness to service and repay debt is relevant to the rating and is a rating driver for Sri Lanka, as for all sovereigns. “Given the increasing possibility of default reflected in the CC rating, this has a negative impact on the credit profile.”

Rating sensitivities

Factors that could, individually or collectively, lead to negative rating action/downgrade:

1.Failure to service bonded debt obligations within grace periods stipulated in relevant documentation, or unilateral declaration of a debt moratorium

2.Launch of a formal debt renegotiation process by authorities or the start of a process that Fitch deems to constitute a default or default-like event

Factors that could, individually or collectively, lead to positive rating action/upgrade:

1.External Finances: Improved external liquidity, supported by higher non-debt inflows or lower external sovereign refinancing risk from an enhanced liability profile that allows for smooth servicing of liabilities

2.Public Finances: Implementation of a credible medium-term fiscal consolidation strategy that supports a sustained decline in the general Government debt/GDP ratio, increasing financing options and reducing the probability of default

3.Structural: Improved policy coherence and credibility, leading to more sustainable public and external finances and a reduction in the risk of debt distress