Tuesday Jun 09, 2026

Tuesday Jun 09, 2026

Friday, 14 November 2025 00:00 - - {{hitsCtrl.values.hits}}

Treasury Secretary Dr. Harshana Suriyapperuma (third from left) speaking at the post-Budget Forum organised by the Daily FT, in partnership with the University of Colombo MBA Alumni Association and sponsored by Standard Chartered Bank at the ITC Ratnadipa, Colombo on Tuesday. Others (from left): University of Colombo MBA Alumni Association President Ajith De Silva, Senior Adviser to the President on Economic Affairs and Finance Duminda Hulangamuwa, Daily FT Chief Editor and CEO Nisthar Cassim (moderator), Standard Chartered Bank Sri Lanka CEO Bingumal Thewarathanthri, Economist Dr. Roshan Perera and Selyn Sri Lanka Business Development Director Selyna Peiris

By Charumini de Silva

By Charumini de Silva

Top private sector figures and public officials on Tuesday shared insights, analysis, implementation challenges and interpretations of the Budget 2026, highlighting its potential to drive investment, innovation and inclusive development of the economy.

Treasury Secretary Dr. Harshana Suriyapperuma on participated as the Chief Guest at the 15th consecutive post-Budget forum organised by the Daily FT, in partnership with the University of Colombo MBA Alumni Association sponsored by Standard Chartered Bank with the creative partnership of Ogilvy Digital at ITC Ratnadipa, Colombo.

Dr. Suriyapperuma engaged in an open, candid discussion on the country’s economic direction with the first fully fledged Budget under the National People’s Power (NPP)-led Government.

He was joined by an eminent panel of economists and business leaders, comprising Senior Adviser to the President on Economic Affairs and Finance Duminda Hulangamuwa, Standard Chartered Bank Sri Lanka CEO Bingumal Thewarathanthri, Economist Dr. Roshan Perera, Selyn Sri Lanka Director Business Development Selyna Peiris and Colombo University MBA Alumni Association President Ajith De Silva.

The discussions were moderated by Daily FT Editor and CEO Nisthar Cassim.

Below are excerpts of the panel discussion.

Q: There have been a lot of concerns expressed about access to finance and credit growth. Last year’s Budget proposed several low-interest loan schemes, yet we continue to hear that access to finance remains a challenge. How do banks view this situation?

Thewarathanthri: There are two aspects to address here, access to credit and credit growth.

On credit to the private sector, we are currently seeing around 21% growth, which is quite substantial. Banks are now disbursing over Rs. 200 billion each month and total disbursements have reached close to Rs. 1.4 trillion. From a growth perspective, that’s a very strong position to be in because banks have been struggling in the last couple of years marked by debt restructuring and now some of those toxic assets are being renegotiated by many clients and settling restructured facilities. The momentum, therefore, is quite positive. At this stage, we are not overly concerned because the growth rate is around 4.8% and it is still manageable. To put this in perspective, in the period between 2015 and 2018, credit growth increased to double digits, exceeding 20% in some years, while economic growth remained around 3.5%. It was a very slow growth and there was no global problem too. That imbalance created vulnerabilities in 2018, we saw spike in non-performing loans (NPLs). Ideally, if credit grows at around 20%, the economy should also expand by at least 5% to maintain stability. Otherwise, problems tend to emerge after a couple of years. However, in the current context, we are emerging from a crisis, and the rise in client borrowing reflects renewed business confidence. PMIs are hovering between 55 and 60, showing expansion across most sectors. The momentum is very good.

Q: Where is this credit growth coming from which sectors are driving it? And are you seeing any concerning trends in credit growth or lending with LTV?

Thewarathanthri: Initially, most of the borrowing came from large corporates and conglomerates, particularly in the services sectors. We didn’t see much SME activity at first. But now, SMEs are increasingly participating, which is a positive shift. At present, around 30% of credit is going into industries, over 30% into services, and about 22% into personal finance of the whole mix, largely linked to vehicle imports. Now that can be a concern. However, when I spoke to players in the leasing industry, they noted that many buyers are individuals who already owned vehicles and had completed earlier leases. They’ve sold those and brought in 30–40% of the new vehicle cost as equity, so the new 50% loan-to-value (LTV) cap will have some impact, but not significantly on this group. Where we’ll see a bigger effect is at the motorcycle level. With prices around Rs. 650,000–700,000, and financing limited to 50%, affordability becomes a real challenge for younger buyers.

Thewarathanthri: Initially, most of the borrowing came from large corporates and conglomerates, particularly in the services sectors. We didn’t see much SME activity at first. But now, SMEs are increasingly participating, which is a positive shift. At present, around 30% of credit is going into industries, over 30% into services, and about 22% into personal finance of the whole mix, largely linked to vehicle imports. Now that can be a concern. However, when I spoke to players in the leasing industry, they noted that many buyers are individuals who already owned vehicles and had completed earlier leases. They’ve sold those and brought in 30–40% of the new vehicle cost as equity, so the new 50% loan-to-value (LTV) cap will have some impact, but not significantly on this group. Where we’ll see a bigger effect is at the motorcycle level. With prices around Rs. 650,000–700,000, and financing limited to 50%, affordability becomes a real challenge for younger buyers.

Q: How is SME credit progressing, especially with the Government’s commitment of Rs. 80 billion in support schemes?

Thewarathanthri: Yes, the 2025 Budget committed about Rs. 80 billion for the SME sector, including low-interest and guarantee schemes. The Credit Guarantee Scheme, which disbursed about Rs. 4 billion last year, is expected to reach Rs. 9 billion this year. However, we have to admit that it’s still not enough. The Industries Ministry has been engaging SMEs, especially those burdened with toxic assets, to come forward with restructuring proposals. Unfortunately, we haven’t seen enough uptake. The Government offered numerous concessions last year and banks also extended relief and timelines for negotiation, but sign-ups were limited. Perhaps communication hasn’t been strong enough, so we’ll need to improve outreach. Out of the total allocation, there are also micro-grants of around Rs. 100,000 for micro-entrepreneurs and small startups. So, there’s real commitment and a wide variety of schemes. The question is how efficiently we can disburse these funds. Banks must also balance growth with prudence, as we’re lending depositors’ money, after all. We must manage our credit appetite carefully and ensure sustainability. On the SME side, we also expect entrepreneurs to become more formal and register their businesses for VAT, maintain P&L and balance sheets and come into the tax net. Transparency is essential for building long-term access to finance. From the Government side, we’ve been recommending the introduction of a cash transaction cap for quite some time. Even a modest cap say, equivalent to one week’s business turnover, can help curb informality and promote digital payments. Right now, Sri Lanka is one of the few countries where someone can carry Rs. 5 million in cash and buy a car outright. That’s not sustainable. Most countries have some form of cash transaction limit, and we should re-examine this as part of our push for formalisation and better tax compliance.

Q: Given the current cash rich Treasury and well capitalised banking system, is there possibility to build buffers for SMEs?

Q: Given the current cash rich Treasury and well capitalised banking system, is there possibility to build buffers for SMEs?

Thewarathanthri: Regarding the Rs. 80 billion SME support package, disbursement will need to happen quickly, especially since the funds come with concessionary rates of 7–8%. I think the banks and the NBFI sector are ready to lend. That said, we are still cautious about certain sectors. Construction, for instance, still has NPLs exceeding 20%, and tourism-related loans are over 30% NPL. So on the new projects, we are still very careful. The overall NPL ratio remains high at 11.2%, one of the highest in the world—let’s not forget that it’s a double digit. So until we bring that down to mid-single digit NPLs, we’ll continue to lend selectively and manage risk carefully.

Q: What are your concerns in terms of the Budget 2026?

De Silva: The Government has increased the revenue threshold. While this may raise revenue, it also creates additional pressure on businesses. There is a potential for price increases, which could impact both SMEs and consumers. The tax administration workload will increase significantly, as authorities need to manage registration, compliance and monitoring for all businesses entering this bracket.

As mentioned earlier, SMEs may see this as a threat to their operations. Therefore, it is critical that the Government communicates clearly with the SME sector about these changes and provides guidance on compliance to minimise disruptions.

Q: Has the Budget addressed the exports strategy sufficiently considering the external challenges? Timelines on FTAs?

Dr. Perera: Despite the external challenges we faced, our exports have grown and it is expected to continue growing next year as well. The question is whether the Budget has taken the global environment into consideration, and whether there’s been any reference to new bilateral trade agreements (FTAs) because while the Budget does mention them, there aren’t any clear timelines. It’s a promising chapter, but implementation will be critical. Now, looking at growth, the Budget has projected a 7% growth target for 2025, which is quite ambitious. To achieve that, we must grow our exports, because historically, Sri Lanka’s growth has been driven largely by domestic, non-tradable sectors such as construction. That model got us into trouble. Sustained growth must come from exports, and the Budget does acknowledge that. If you look at the reforms listed such as the National Export Strategy, new trade agreements, a tariff rationalisation policy, the creation of a single window and virtual special economic zones—these are all important. But we have to ask, what has Sri Lanka’s experience been in implementing such reforms? Looking back at the last 10  Budgets, almost everyone has talked about trade agreements and 8 out of 10 have promised new ones; 7 mentioned export zones and single windows and about 6 discussed tariff reforms. Yet, progress has been limited. Implementation remains our biggest weakness. The authorities have said they’re keen on implementation, but the reality is that there are serious capacity constraints within the public sector. Unless that is addressed, reforms will continue to stall. There are also new proposals under the Strategic Development Projects (SDP) Act and the Port City framework. My view is that Sri Lanka should have one unified incentive regime, transparent and predictable rather than different regimes under different authorities. Investors should clearly understand what incentives are available and they should be justified by job creation and value addition. If, for example, 50% of the projects are real estate or housing-related, we must question what real export or employment benefits they bring. Beyond that, there are reforms pending on investor protection laws, land banks and residency programs. But again, implementation is key. Sri Lanka has repeatedly struggled to execute reforms that are entirely within our control. Countries that have successfully implemented trade and investment reforms now have export-to-GDP ratios of three to four times ours. Sri Lanka’s remains at around 20%. We must accelerate internal reforms, especially as the global environment becomes more challenging with rising nationalism, protectionist industrial policies and growing strategic subsidies in other countries. Market access is becoming more difficult. We need to integrate into supply chains and partner effectively to stay competitive. Otherwise, we risk being bypassed. Another concern is the rise of tariff and non-tariff barriers. Without diversified trade agreements, we are highly exposed to narrow markets. Similarly, global shifts toward on-shoring and near-shoring mean that countries are reorganising their supply chains based on political alignment and logistical resilience. Without high-quality economic zones and streamlined export processes, Sri Lanka is increasingly being bypassed in global FDI allocation. Investors want certainty, efficiency, and timely approvals. Finally, with tightening global financial conditions, risk premiums could rise, making it harder for exporters to borrow. Sri Lanka must therefore attract more non-debt-creating inflows through structural reforms and FDI. Delays in implementing these reforms will erode export competitiveness and reduce our growth potential.

Budgets, almost everyone has talked about trade agreements and 8 out of 10 have promised new ones; 7 mentioned export zones and single windows and about 6 discussed tariff reforms. Yet, progress has been limited. Implementation remains our biggest weakness. The authorities have said they’re keen on implementation, but the reality is that there are serious capacity constraints within the public sector. Unless that is addressed, reforms will continue to stall. There are also new proposals under the Strategic Development Projects (SDP) Act and the Port City framework. My view is that Sri Lanka should have one unified incentive regime, transparent and predictable rather than different regimes under different authorities. Investors should clearly understand what incentives are available and they should be justified by job creation and value addition. If, for example, 50% of the projects are real estate or housing-related, we must question what real export or employment benefits they bring. Beyond that, there are reforms pending on investor protection laws, land banks and residency programs. But again, implementation is key. Sri Lanka has repeatedly struggled to execute reforms that are entirely within our control. Countries that have successfully implemented trade and investment reforms now have export-to-GDP ratios of three to four times ours. Sri Lanka’s remains at around 20%. We must accelerate internal reforms, especially as the global environment becomes more challenging with rising nationalism, protectionist industrial policies and growing strategic subsidies in other countries. Market access is becoming more difficult. We need to integrate into supply chains and partner effectively to stay competitive. Otherwise, we risk being bypassed. Another concern is the rise of tariff and non-tariff barriers. Without diversified trade agreements, we are highly exposed to narrow markets. Similarly, global shifts toward on-shoring and near-shoring mean that countries are reorganising their supply chains based on political alignment and logistical resilience. Without high-quality economic zones and streamlined export processes, Sri Lanka is increasingly being bypassed in global FDI allocation. Investors want certainty, efficiency, and timely approvals. Finally, with tightening global financial conditions, risk premiums could rise, making it harder for exporters to borrow. Sri Lanka must therefore attract more non-debt-creating inflows through structural reforms and FDI. Delays in implementing these reforms will erode export competitiveness and reduce our growth potential.

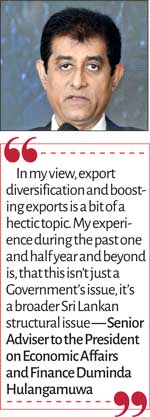

Hulangamuwa: In my view, export diversification and boosting exports is a bit of a hectic topic. My experience during the past one and half year and beyond is, that this isn’t just a Government’s issue—it’s a broader Sri Lankan structural issue. When it comes to exports or attracting foreign investment, the question is: why should an investor choose Sri Lanka? We lack supply chains, raw material access and links to large labour markets like Vietnam. Even with trade agreements, we struggle to benefit. Take the FTA with India—yes, exports increased somewhat, but the Thailand FTA couldn’t be implemented for various reasons. Even where we have agreements, our cost base is too high. In my opinion, it’s not just about signing FTAs or creating zones, it’s about fixing the fundamentals at home. Manufacturing exports are especially challenging. Our comparative advantage lies in services such as tourism, IT/BPM, logistics and shipping. These are the areas we must identify and prioritise. For 30 years, we’ve offered export tax incentives, yet exports remain stagnant at around 8–9% of GDP. That’s because we don’t have access to raw materials, large labour forces, or the scale that countries like Vietnam enjoy. For example, when Uniqlo, the world’s largest apparel retailer, looked at Sri Lanka, they wanted a factory employing 10,000 workers. We simply can’t provide that. So, while manufacturing exports will continue to face structural constraints, our focus should be on services where we have competitive advantages. That’s the realistic path forward.

Thewarathanthri: I largely agree, but I’d add that Sri Lanka should focus on niche manufacturing rather than mass production. We can’t compete with Vietnam or Bangladesh on scale. But we can excel in specialised products like intimate apparel for Victoria’s Secret or solid-tyre manufacturing—areas where we already have capability and done extremely well. We will never succeed in mass manufacturing. There’s also an emerging opportunity to become part of India’s expanding supply chain. Japan, for instance, is looking for alternative manufacturing bases beyond India. Sri Lanka could play an “India Plus One” role in that ecosystem, possibly producing for export markets outside India. That said, FDI is fundamentally an outcome of stability. Political stability drives policy stability and that, in turn, drives investor confidence. Our FDI inflows peaked around 2010–2011 with projects like Shangri-La and again around 2017 with the sale of Port. Beyond that, inflows have been low. Since opening the economy, we’ve attracted around $ 23–24 billion in total, while Vietnam attracts $ 18–20 billion per year. We need to recognise that we’re competing for the same pool of investors as other emerging markets. I’ve a different view about the Strategic Development Projects Act. We need an incentive package for the large investors to come in, provided they are transparent and rule-based. We must not assume that just because land is available in Port City or Hambantota, investors will automatically come. We need consistency and predictability in policies to walk the talk. The other most important thing we spoke of is the Ease of Doing Business Index, again an outcome of stability and policy consistency. Since Sri Lanka missed the bus on rankings in Ease of Doing Business Index, there’s a new Be Ready Index, which now covers 50 countries and will expand to 100 by 2026. This index looks at three key pillars: regulatory framework, Government services and operational efficiency. Sri Lanka should aim to at least get into that and urge the Government to look at Be Ready Index and have a taskforce around it. Because getting some ranking in the top 100 would be critical for us. If we can make meaningful progress there, especially by addressing barriers to entry, exit, labour, and permits; it will go a long way toward restoring investor confidence.

Peiris: I completely agree, particularly on the need for a niche focus. As someone representing SMEs and a niche exporter; we manufacture toys. I’ve seen firsthand the potential in specialised products. Despite global headwinds, we’re seeing increased orders from US buyers because of our craftsmanship and reliability. That’s why I also commend the Government for allocating funding for research and development (R&D), and commercialisation. It’s essential if we’re to find new niches and pockets of competitive strength. However, I would urge the Industries Ministry to narrow its focus. They’ve now identified 28 ‘thrust sectors,’ up from 20. Instead of spreading resources thin, we should focus on five key areas with immediate potential for export earnings and job creation. In this transitional phase for Sri Lanka, we need quick wins and demonstrable success stories to build momentum. We need to drive whatever we have left in this country towards areas of focus that can reap benefits. I also acknowledge that this Government inherited a difficult legacy. But we, in the private sector are ready to work with them to make these reforms succeed.

Q: The Budget speech highlights exports, but there seems to be limited emphasis on service exports. What are your views on this, and could you elaborate on the new National Export Strategy?

Q: The Budget speech highlights exports, but there seems to be limited emphasis on service exports. What are your views on this, and could you elaborate on the new National Export Strategy?

Hulangamuwa: I agree that there are specific niche products we should focus on, but if the goal is to build foreign reserves, service exports have a higher potential than manufactured goods. Even if we manufacture locally, about 70% of inputs are imported, so the domestic value addition is limited unless we focus on mineral exports or similar sectors. For manufactured goods targeting global markets, we would still need to import a significant portion of raw materials, reducing the net benefit to foreign reserves. By contrast, digital and IT services, or other service-oriented exports, provide much higher value addition. Tourism also has a strong effect on foreign reserves because it generates actual foreign currency. So, the strategy is clear: focus on high-value service exports, where Sri Lanka can realistically increase foreign capital. On the logistics front, we are planning to extend the Colombo Port breakwater by next year and start the West Terminal II within a year afterward. We are also aiming to create an international logistics centre, though it won’t be completed immediately, tenders will be called, and implementation will take time. I think to me, those will add more value, but these initiatives may not yield massive revenue immediately, but they are part of a broader export and investment strategy. For example, discussions with Japanese investors have shown that smaller-scale investments of $10–20 million are possible, but if we aim to attract $2–3 billion in FDI, in terms of manufacturing exports. To get that, we need something unique, a competitive supply chain or a differentiated proposition. Even with zero taxes, without such differentiation, attracting large-scale investments will be extremely difficult. I hope the Japanese proposal that we are currently discussing may materialise. But export growth in Sri Lanka is inherently challenging. We already face structural constraints, and we must carefully decide which sectors and strategies to pursue to maximise benefits to the economy.

Q: Did Budget 2026 miss any policies? Was there anything obvious that you felt the Government could have done but didn’t include?

Dr. Perera: Not so much a missing piece, but I’d like to emphasise something important. The key now is to continue with the reform agenda. There’s no room for complacency, because we still need to accelerate growth because reform fatigue can easily set in. We’ve seen this in many countries, and Sri Lanka isn’t immune. Reform fatigue often leads to policy reversals and we’ve seen that here before. When people begin to feel that the costs of reform are too burdensome, public support starts to erode. That’s when Governments backtrack. So, my point is that we need to push through and accelerate reforms. We cannot afford to pause or slow down.

Peiris: The key word right now is focus. There’s a lot in this Budget, but as a country, and as the Government, we need to decide what we’re prioritising. There are many competing needs, but focus is essential if we want meaningful progress.

Q: What’s your advice to the private sector, now that you’re cautiously optimistic?

Thewarathanthri: We need to keep the ball rolling. The macro stability we’re beginning to see with sustainable interest rates and a relatively stable exchange rate, will help. But companies also need to build their own capacity. We can’t simply complain or expect the Government to solve everything, especially when it comes to skills. Universities and vocational training programs will help, but the private sector must also step up and invest in training, build internal capacity and plan for succession. What’s missing in the Budget is a clear implementation roadmap. The “how” piece is not fully laid out. For example, we still need more clarity on the PPP law, on trade facilitation measures and on how initiatives like the single window system will actually be executed. We should identify the four or five critical industries that can drive growth and the 10 enabling factors that support them with clear timelines. Without that focus and execution plan, it’s difficult to convert policy into impact.

Q: A question to both from the Government—a common concern we hear is about capacity constraints within the State. There are many ambitious plans, but does the public sector have the ability to implement them effectively?

Dr. Suriyapperuma: That’s a valid concern. Capacity gaps are real. We’ve seen that in both the private and public sectors. But one of the key ways this is being addressed is through the digital transformation drive. Rather than filling every vacancy with more personnel, the Government is looking at digitising processes and services enabling citizens to track applications, access services online and reduce bottlenecks. That said, there are still critical technical vacancies for valuers, revenue officers, legal officials, many of whom left during the crisis years for the private sector or overseas. There’s a focused recruitment drive to fill these essential roles, while also using digitisation to enhance capacity and efficiency. These challenges are recognised and efforts are underway to address them.

Hulangamuwa: I’d say overall, this is a good Budget. It’s been crafted with growth in mind. But we have to remember that a Budget alone won’t generate growth. It provides the policy direction, but execution goes far beyond that. Attracting FDI remains a major challenge in the current global climate. Western capital is cautious, partly due to geopolitical tensions, protectionism and shifting global priorities. So, we’re competing in a tough environment. That’s why governance and transparency are so important. If we can strengthen institutions like the Debt Management Office, the Port City Commission, and effectively implement the PPP law and State-Owned Enterprise reforms, we can build investor confidence. Ultimately, creating a transparent and predictable governance framework will help stabilise FDI flows, encourage private sector engagement and support sustainable, broad-based growth for the country.

Audience Q&A

Q: If digitisation is being implemented, is constructing a new building for the Inland Revenue Department necessary, given that digital interconnection should reduce the need for physical consolidation?

Q: If digitisation is being implemented, is constructing a new building for the Inland Revenue Department necessary, given that digital interconnection should reduce the need for physical consolidation?

Dr. Suriyapperuma: I appreciate all the perspectives shared as they reflect genuine interest and informed concern. Allow me to clarify a few points and correct some perceptions. Regarding the new IRD building, while your observation on digitisation is valid, the rationale goes beyond connectivity. The IRD currently operates from different locations, leading to high rental and administrative costs. Consolidating operations into a single facility will save costs over time and improve efficiency. It’s not an issue of inadequate digital connectivity, but rather one of long-term rationalisation and cost optimisation.

Q: How will the Government ensure long-term fiscal sustainability of payments and subsidies, particularly for estate sector workers, without creating a permanent financial burden?

Dr. Suriyapperuma: The intention is not to provide indefinite subsidies. The Government’s role is to support these sectors during a transition period, helping them stabilise and integrate into the broader economy. Over time, the expectation is that the industry itself will take over these responsibilities. These decisions are made through consultations with industry stakeholders to ensure sustainability and inclusiveness—leaving no one behind.

Q: With most Ministries achieving less than 25% of planned implementation, what steps will be taken to strengthen Parliamentary and fiscal monitoring through the CoPF?

Dr. Suriyapperuma: We agree that continuous oversight is vital. While capital expenditure has been relatively low this year, partly because the 2025 Budget implementation started later than usual due to election cycle, we are strengthening engagement with line Ministries and stakeholders to ensure timely disbursements. Parliamentary oversight mechanisms will also be reviewed and enhanced to support better Budget execution as we move into 2026.

Q: For medical cannabis exports seven investors are ready to bring in over $ 200 million, but export approvals are stalled despite a Gazetted framework. Why is decision-making delayed, and how can ease of doing business be improved?

Dr. Suriyapperuma: Thank you very much for highlighting that. I understand your concern. In most other areas, decisions are being made, and projects are moving forward. However, as you mentioned, exporting cannabis is a sensitive area. If it were only an administrative decision, it would have been made long ago, but even previous Governments faced similar challenges. I assure you the matter is being reviewed and will be resolved as soon as possible.

Hulangamuwa: I just checked with the BOI. Several agreements are expected to be finalised within about two months.

Q: When gazetted policies such as those on cannabis or mining are not acted upon, investor confidence suffers. How will the Government ensure consistency and follow-through?

Hulangamuwa: Yes, Government policymaking is never easy.

Q: Traffic congestion in Colombo and its suburbs has become a growing problem, with people spending significant time commuting to and from work. In your opinion, does this Budget allocate sufficient funds to improve public transport and related infrastructure?

Hulangamuwa: Yes, traffic congestion in Colombo and the suburbs is indeed a serious issue. The Budget 2026 allocates the highest-ever funding for road infrastructure. For instance, we’ve allocated funds for the Central Expressway and other major expressway extensions, including the Kadawatha Expressway, which has already commenced. We’ve also allocated funds to complete the final stretch connecting to Rambukkana. These projects, once completed within about three years, will ease traffic considerably, particularly along the Kandy Road and also support tourism by improving connectivity to the Central and Southern Expressways. You may recall in the Budget speech, the President mentioned the Lotus Tower-to-Airport Expressway, which was left incomplete because traffic projections were not properly studied. Six months ago, a study revealed that nearly 50,000 vehicles reach the Lotus Roundabout daily — a volume the current infrastructure cannot handle. Hence, a new feasibility report is being prepared to improve that connection and ease traffic flow into Colombo.

Dr. Suriyapperuma: As mentioned, the Government is making large investments not only in road infrastructure, but also in enhancing public transport connectivity and comfort. Funding has been allocated to bring in new buses over the next three years, some of which are low-floor models expected to arrive as early as 2025. Investments are also being made to modernise the railway system, including new locomotives, upgrades to the signalling network and overall infrastructure improvements. We are also developing domestic airports to provide alternative, faster transport options for tourists and business travellers, thereby reducing pressure on road networks. Additionally, digital payment systems for public transport will be introduced this year, with full implementation expected next year. Together, these initiatives aim to make public transportation more efficient, accessible and user-friendly.

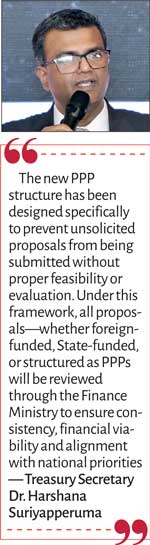

Q: With both the Public Financial Management Act and a new PPP Act being developed under NAPPP, which framework will take precedence, and how will overlaps be avoided?

Dr. Suriyapperuma: Thank you, that’s a very valid question. The new PPP structure has been designed specifically to prevent unsolicited proposals from being submitted without proper feasibility or evaluation. Under this framework, all proposals—whether foreign-funded, State-funded, or structured as PPPs will be reviewed through the Finance Ministry to ensure consistency, financial viability and alignment with national priorities. This process will help prevent the inefficiencies and costs we’ve suffered in the past due to inadequate systems, creating a seamless process under the Finance Ministry. Of course, there will be some teething issues initially, but these will be ironed out soon.

Dr. Suriyapperuma: Thank you, that’s a very valid question. The new PPP structure has been designed specifically to prevent unsolicited proposals from being submitted without proper feasibility or evaluation. Under this framework, all proposals—whether foreign-funded, State-funded, or structured as PPPs will be reviewed through the Finance Ministry to ensure consistency, financial viability and alignment with national priorities. This process will help prevent the inefficiencies and costs we’ve suffered in the past due to inadequate systems, creating a seamless process under the Finance Ministry. Of course, there will be some teething issues initially, but these will be ironed out soon.

Q: With the new requirement for permanent VAT numbers, will exporters who previously operated under temporary VAT registrations have to repay past VAT concessions?

Dr. Suriyapperuma: That’s an important point. Temporary VAT numbers were often misused to avoid paying taxes. After conducting a proper risk analysis, the Government decided to tighten the mechanism and require permanent VAT registration. However, exceptions will be considered case by case by the IRD. If your business partner or operation falls within the new defined threshold, then yes, VAT payments will apply accordingly. The goal is simply to ensure compliance and fairness in the system.

Q: What’s the way forward for large construction projects such as the BIA expansion, JICA-funded road and power projects, etc.? Many of these seem stalled.

Hulangamuwa: The BIA expansion is currently under technical evaluation and financial bids are expected to open in November. If all goes well, contracts could be awarded by the first quarter of next year. It’s important to note that restarting stalled projects is far more difficult than initiating new ones, especially since these are bilateral-funded initiatives. Cost escalations have nearly doubled, requiring renegotiation of terms with donor countries. However, the fourth stage of the Central Expressway is expected to be awarded to local contractors. Overall, by next year, most of these projects should resume, which will bring renewed opportunities for local construction firms and subcontractors.

Q: As a PAYE taxpayer, I expected at least an increase in the personal tax relief threshold from Rs. 50,000 to Rs. 200,000. Why wasn’t this considered?

Dr. Suriyapperuma: That’s a fair question and indeed, it’s something we aspire to. However, given the fragile state of the economy, any relief has to be introduced gradually. The Government’s plan is to increase relief over time in a way the economy can absorb. While it didn’t happen in this Budget, it’s certainly under consideration for the future.