Friday Jul 17, 2026

Friday Jul 17, 2026

Friday, 17 July 2026 00:23 - - {{hitsCtrl.values.hits}}

The announcement that the World Bank has officially restored Sri Lanka to Upper-Middle Income Country (UMIC) status has been widely greeted with political and public relief. Backed by an official 5.0% real GDP expansion and a calculated Atlas Gross National Income (GNI) per capita rise to $4,670, this upgrade is being framed as the definitive turning point of our post-crisis recovery.

The announcement that the World Bank has officially restored Sri Lanka to Upper-Middle Income Country (UMIC) status has been widely greeted with political and public relief. Backed by an official 5.0% real GDP expansion and a calculated Atlas Gross National Income (GNI) per capita rise to $4,670, this upgrade is being framed as the definitive turning point of our post-crisis recovery.

However, macroeconomics is an unforgiving science. For researchers tracking the structural integrity of national accounts, this moment triggers a profound sense of déjà vu.

Sri Lanka has stood on this identical threshold before. In July 2019, we crossed into the UMIC bracket with a GNI per capita of $4,060, only to face a humiliating downgrade back to Lower-Middle Income (LMIC) status just twelve months later. That brief moment of celebration masked severe structural imbalances that ultimately broke our financial system and culminated in the sovereign debt default of 2022. Today, a comprehensive look at the data reveals that we are repeating the exact same mistake. Our second ascent to the upper-middle tier is not a reflection of real industrial or structural growth; it is a mathematical artefact driven by short-term anomalies.

The math behind the mirage: 2019 vs. 2026

To understand why this graduation is built on quicksand, we must contrast the underlying structural frameworks of the 2019 and 2026 upgrades. While both periods achieved the identical result of crossing the World Bank's mathematical line, they did so using entirely different—and highly unstable—economic methods.

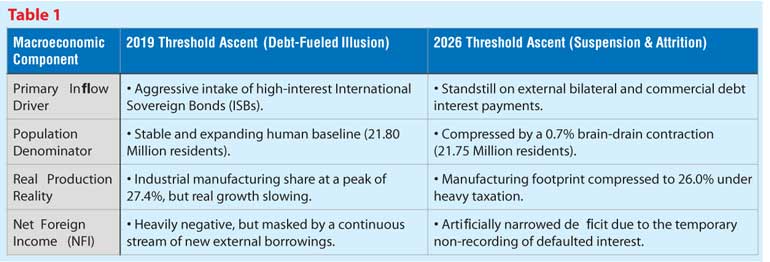

2019 Balance: The illusion of debt accumulation

In 2019, our upper-middle-income status was sustained entirely by external borrowing. Net Foreign Income (NFI)—the crucial economic bridge that reconciles domestic production (GDP) with true national income (GNI)—was heavily negative due to rising interest servicing costs on commercial sovereign bonds.

However, because the state maintained continuous access to global capital markets, a steady influx of international loans artificially propped up the value of the Sri Lankan Rupee (LKR). When processed through the World Bank’s smoothed Atlas three-year exchange rate average, these debt inflows generated a statistical valuation boost. We looked richer because we were borrowing aggressively, not because we were producing efficiently. When the tax cuts of late 2019 destroyed the state revenue base and credit rating downgrades cut off our market access, this fragile model collapsed.

The 2026 Balance: The illusion of suspension and attrition

Seven years later, the math behind our 2026 return to the UMIC bracket reveals a highly unstable foundation. Under System of National Accounts (SNA) standards, GNI per capita is a simple fraction: Total National Income divided by the Total Resident Population. Over the recent assessment cycle, this fraction was artificially altered by two temporary factors:

1.The human denominator attrition: Following the severe hardships of the 2022 crisis, Sri Lanka experienced a massive wave of high-skilled professional migration. This brain drain caused an unprecedented 0.7% absolute contraction in the resident population denominator. When you divide a stabilising economy by a shrinking number of people, the mathematical average income per capita automatically climbs—even if the actual productivity of the workforce has flatlined.

2.The interest suspension freeze: According to international accounting rules, the external interest obligations that a country owes are recorded as a major negative deduction within the primary income account. Currently, Sri Lanka is under a formal standstill on external commercial and bilateral interest tracking while debt restructuring finalised. By temporarily freezing these outflows, billions of dollars are kept within our national accounting books. This creates a temporary, artificial surge in reported national income that does not represent real economic output.

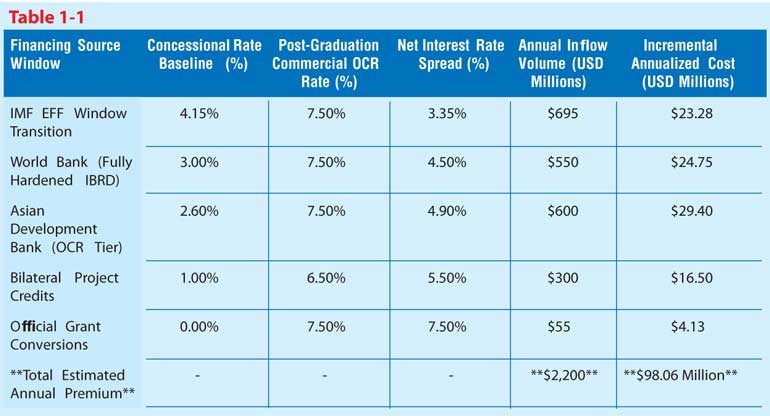

The "Financing Cliff": A $98 million post-graduation bill

The most immediate danger of this reclassification is the automatic financial penalty it carries. The World Bank and the Asian Development Bank (ADB) design their concessional loan windows—which offer very low interest rates and long repayment grace periods—strictly for lower-income states. Currently, the Treasury relies on roughly $2.2 billion in annual external inflows to manage the Balance of Payments gap and fund essential capital development. A staggering 86.3% ($1.90 billion) of this financing is obtained on a highly concessional basis. By graduating to a UMIC, Sri Lanka automatically triggers a mandatory transition toward market-based Ordinary Capital Resources (OCR) and harder IBRD terms.

Our research simulations show the exact financial impact if income and expenditure levels remain unchanged while these soft loan windows slam shut: This structural hardening hands the Treasury an immediate incremental interest bill of $98.06 Million (approximately Rs. 32.9 billion) annually.

Worse still, our repayment grace periods will contract from standard 7-to-10-year windows down to compressed 3-to-5-year commercial timelines. This change will drastically accelerate our external capital amortisation schedule, draining the Central Bank's hard currency reserves just as full commercial and bilateral debt servicing prepares to resume.

The impending export trap: The GSP+ clock begins to tick

The financial penalty extends directly into our export real sector. Under the European Union’s revised GSP guidelines, tariff concessions are strictly reserved for low and lowermiddle-income economies. Graduating to a UMIC sets off an automatic timeline for the mandatory removal of GSP+ preferences.

While Sri Lanka will receive a standard three-year procedural grace period, the end of this window represents a major challenge for our primary formal employer: the apparel sector.

Stripping away GSP+ will introduce standard Most-Favoured-Nation (MFN) tariffs of 9.6% to 12% on Sri Lankan garments entering Europe. Overnight, our factories will face an unmanageable cost disadvantage against regional competitors like Bangladesh and Viet Nam, which operate on highly integrated, low-tariff supply chains.

Breaking the Middle-Income trap: A strategy for structural permanence

If the 2019 upgrade was a mirage built on borrowing money, the current upgrade is a temporary balance built on debt suspension and demographic loss. Taxing the existing formal economy at high rates to maintain an IMF primary surplus functions as a short-term compression strategy rather than a path to long-term wealth creation. To prevent the threshold trap from snapping shut once again when full debt servicing resumes, Sri Lanka must immediately shift toward deep institutional and trade restructuring:

1.Establish Constitutional fiscal rules: Statutory rules like the Central Banking Act remain vulnerable to future political shifts. Sri Lanka must follow Singapore’s model by enacting a constitutional mandate that requires the Government to maintain a balanced Budget on average over each five-year election cycle, insulating public finances from populist spending cycles.

2. Upgrade trade complexity: We must stop relying on low-complexity, traditional export segments like garments and raw agricultural commodities. The Ministry of Trade must establish comprehensive bilateral pacts designed to pull our private sector into high-complexity global value chains, such as advanced electronics and specialised components—replicating the structural transition executed by Viet Nam.

3.Incentivise Human Capital Retention: To halt the professional migration that is shrinking our demographic denominator, the state must offset high income tax rates with non-monetary professional benefits. Establishing dedicated digital infrastructure zones, fast-tracking corporate venture setups, and strengthening intellectual property laws will help retain the talent pool required to drive a modern innovation economy.

Reclaiming our Upper-Middle Income status is an important psychological milestone, but it must not lead to policy complacency. If we look at aggregate numbers and assume the underlying structural crisis has been resolved, we risk facing another major economic reversal. Implementing these deep adjustments is the only way to convert a temporary statistical rebound into a permanent path toward sustainable development.

(The author is the Principal Consultant and CEO of KiWi Strategy Consultants. A Chartered Engineer with a diverse professional portfolio spanning senior corporate leadership, investment management, and strategic consulting, he holds a B.Sc. in Mechanical Engineering from the University of Peradeniya and an MBA from the University of Colombo. His extensive executive career includes tenures as the CEO of Dankotuwa Porcelain PLC and General Manager at ACME Printing & Packaging, alongside active, board-level involvement with the Marga Institute. Leveraging his expertise in industrial systems, macro-policy structures, and professional management frameworks, his current research focuses on structural economic dynamics, trade optimisation, and development economics in South Asia)