Thursday Jul 16, 2026

Thursday Jul 16, 2026

Saturday, 16 May 2026 01:23 - - {{hitsCtrl.values.hits}}

By First Capital Research

Sri Lanka’s debt crisis is not unprecedented. Several countries have experienced similar periods of financial stress and have faced prolonged challenges in restoring market confidence, despite IMF-support and adjustment efforts. Our analysis takes a deep dive into international experience to assess which policy measures proved effective, where responses fell short, and what lessons Sri Lanka can realistically apply as it navigates its post‑crisis recovery, with Greece serving as a particularly relevant benchmark.

Greece’s debt crisis emerged in 2009–2010, stabilised temporarily, and resurfaced in renewed stress in 2015 before transitioning into a sustained recovery. Sri Lanka shares comparable structural features with Greece, including the gradual build‑up of pre‑crisis vulnerabilities, making Greece’s post‑crisis adjustment a relevant benchmark for assessing Sri Lanka’s medium‑term recovery path.

Structural fault lines and political cycles

Greece’s crisis reflected deep economic fault lines that later intertwined with destabilising political cycles. Weak investment incentives, public‑sector and labor‑market inefficiencies, fiscal vulnerabilities, and a narrow export base formed the underlying sources of instability, several of which remain relevant to Sri Lanka today. These structural constraints suppressed growth, weakened fiscal resilience, and increased exposure to external shocks. On the political front, in Greece’s early post‑crisis years, repeated political shifts contributed to delayed recovery, a pattern that mirrors Sri Lanka’s experience as it enters its third political cycle following the crisis.

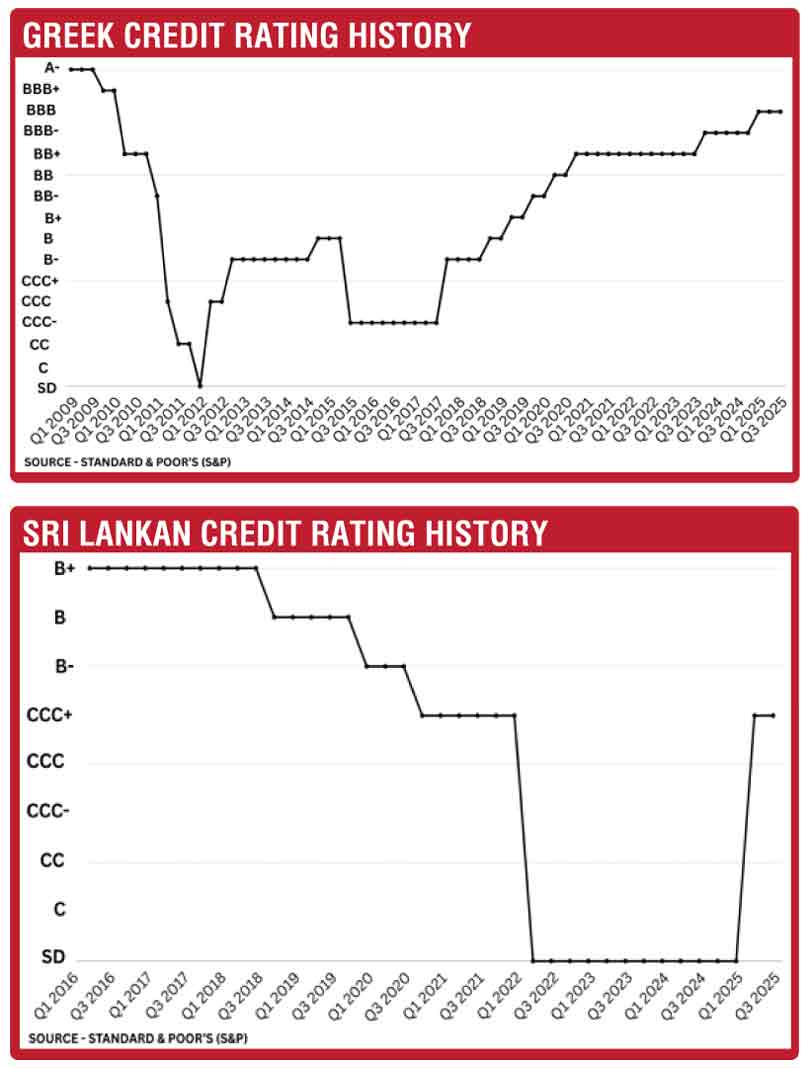

Credit rating dynamics: Early gains, lingering risks

Greece saw early rating upgrades after initial downgrades, but a second crisis halted progress due to a weak recovery. Sri Lanka has seen slower early post‑program upgrades, with the path ahead hinging on reform delivery, debt‑deal execution, and sustained market access.

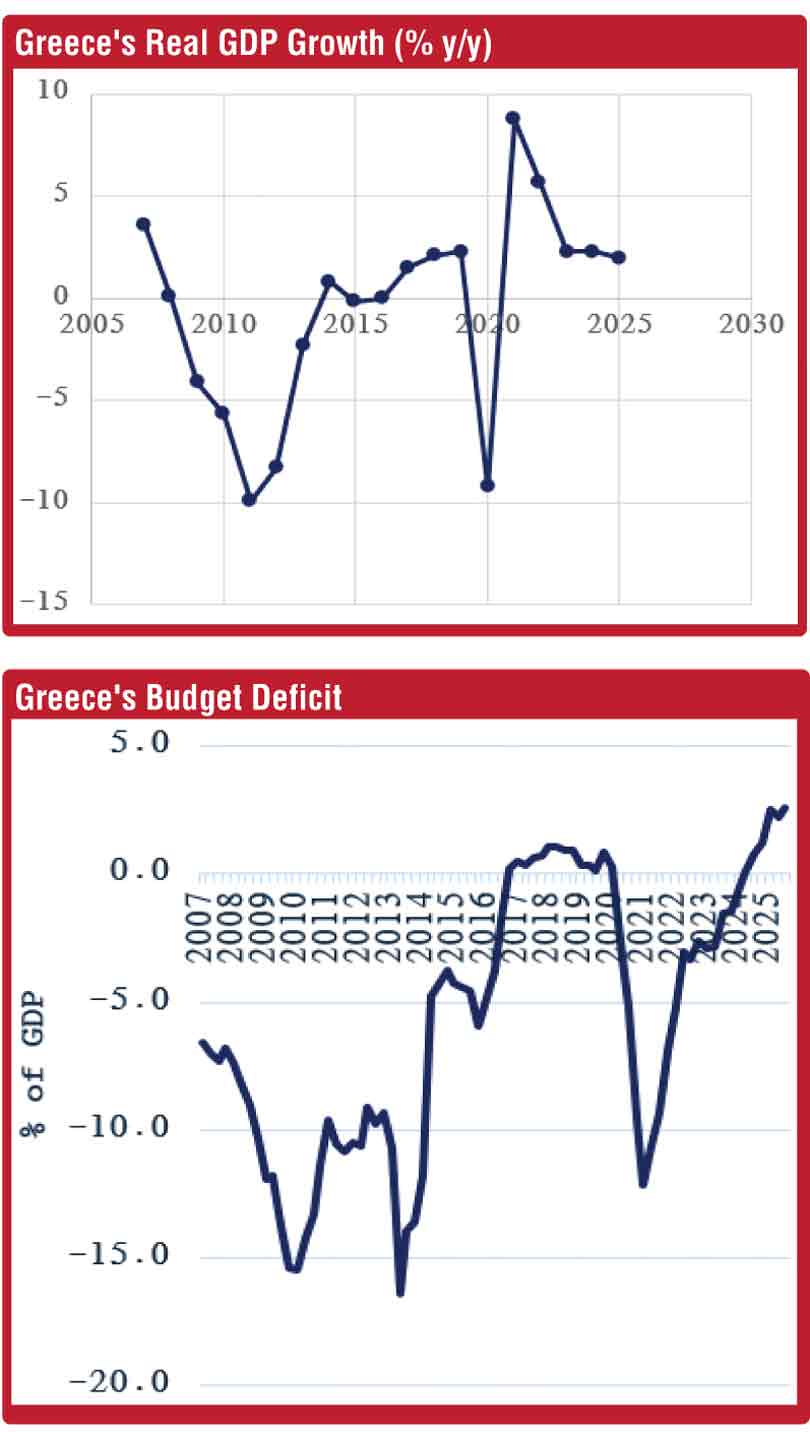

Fiscal adjustment improved stability, but growth lagged

Economic, fiscal, and external sector cycles in Greece show that while front‑loaded fiscal adjustment improved macro stability, still recovery remained fragile without coordinated growth‑oriented reforms. Fiscal consolidation significantly improved Greece’s budget balance but weighed heavily on growth during 2010–2013. Although conditions stabilised briefly in 2013–2014, the recovery proved fragile, with renewed political uncertainty in 2015 undermining confidence and reversing fiscal and economic gains.

Sri Lanka now stands at a crossroads similar to Greece in 2013-2014, where early gains can either evolve into sustained recovery or give way to renewed stress if reform momentum weakens. The policy choices made at this stage will be decisive in defining the next phase of the country’s economic trajectory

Sri Lanka now stands at a crossroads similar to Greece in 2013-2014, where early gains can either evolve into sustained recovery or give way to renewed stress if reform momentum weakens. The policy choices made at this stage will be decisive in defining the next phase of the country’s economic trajectory

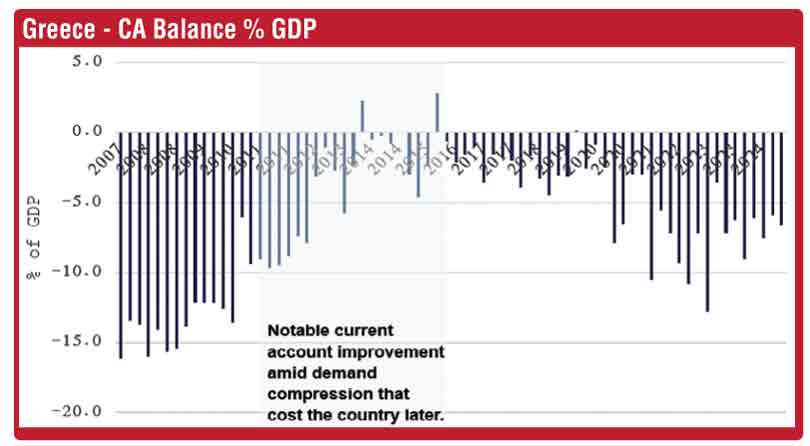

External adjustment driven by demand compression

Greece’s current account dynamics offer further insight, as during periods of heavy austerity without complementary reforms, external adjustment occurred largely through demand compression rather than competitiveness gains. Sri Lanka faces a similar challenge to Greece, where sustaining stability will depend on pairing fiscal discipline with growth‑oriented reforms. So far, the economy, like Greece’s early post‑crisis phase, has adjusted largely through demand compression, as reflected in Sri Lanka’s current‑account surplus driven by weak capital‑goods imports, reinforcing a pattern of “doing less rather than selling more”.

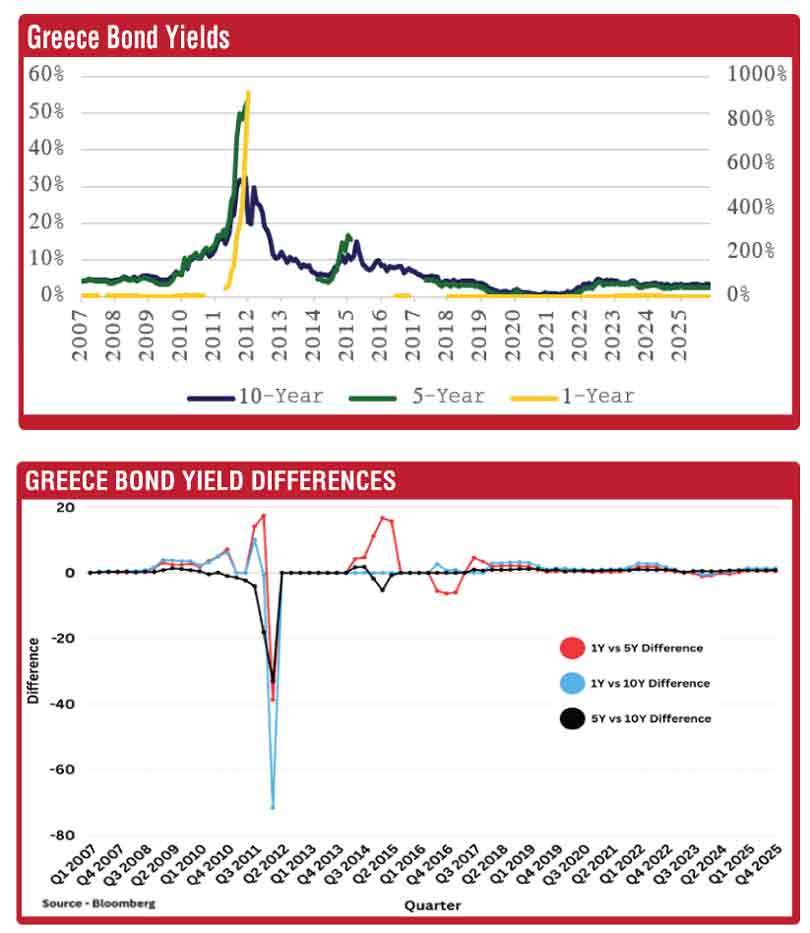

Bond market response across the crisis cycle

Financial markets in Greece and Sri Lanka display a similar pattern, crisis‑driven yield spikes and curve steepening, followed by gradual normalisation as credibility improves. As yields become increasingly market‑driven rather than crisis‑managed, they support recovery by lowering government financing costs and improving investment conditions.

Reform sequencing as foundation of durable recovery

Greece’s recovery was underpinned by reforms implemented in three broad phases:

1) IMFled macrostabilisation,

2) Domestically driven fiscal and institutional reforms, and

3) A later growthoriented reform agenda focused on competitiveness.

The key lesson for Sri Lanka is that stabilisation is only the first step in recovery. Sustaining reform momentum beyond the program period is essential to translate macrostability into durable growth and restored market confidence. Ultimately, recovery outcomes depend less on the speed of initial stabilisation and more on the consistency, depth, and sequencing of reforms.

Where Sri Lanka stands today

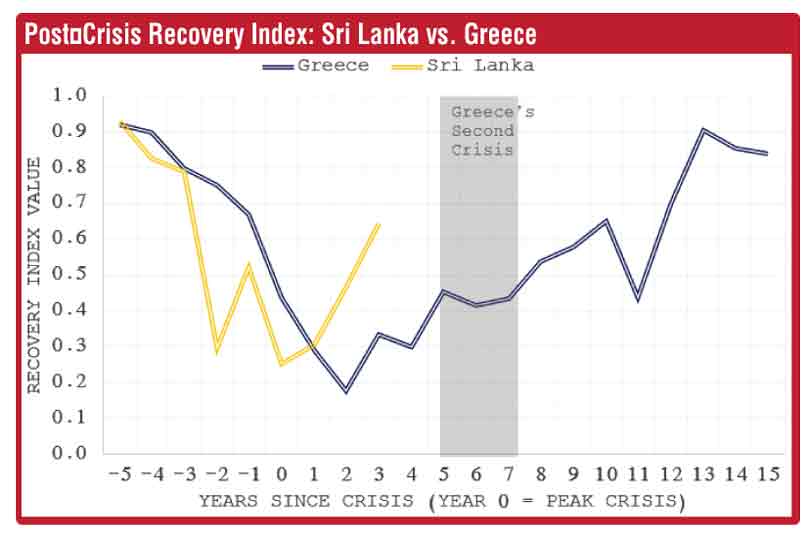

Finally, to benchmark Sri Lanka’s recovery relative to Greece, we constructed a composite index covering Stability, External and Investment Recovery, Growth, and Sovereign Risk. The index indicates that while Sri Lanka’s early stabilisation compares favorably, the durability of recovery hinges on a successful transition from stabilisation to growth.

We conclude that Sri Lanka now stands at a crossroads similar to Greece in 2013-2014, where early gains can either evolve into sustained recovery or give way to renewed stress if reform momentum weakens. The policy choices made at this stage will be decisive in defining the next phase of the country’s economic trajectory.