Tuesday Jun 30, 2026

Tuesday Jun 30, 2026

Wednesday, 20 May 2026 05:16 - - {{hitsCtrl.values.hits}}

Fraud in Sri Lanka’s banking and finance sector has become a growing concern over the past three decades, with major incidents reported from the 1990s to the present, including large-scale financial scams, insider fraud, money laundering, document forgery, loan irregularities, and illegal pyramid schemes. Several of these cases have resulted in significant financial losses and weakened public confidence in banks and financial institutions. The recurrence of such incidents has exposed long-standing weaknesses in regulation, supervision, and corporate governance, while also highlighting gaps in enforcement by authorities. In many instances, fraud has been carried out by individuals within financial institutions who misuse their authority and access for personal gain. Weak oversight, political interference, and outdated or fragmented digital monitoring systems have further limited the ability to detect suspicious activities at an early stage, allowing fraudulent operations to continue for extended periods. The wider economic impact has been substantial, contributing to higher borrowing costs, reduced investor confidence, and increased pressure on regulators, including the Central Bank of Sri Lanka, to strengthen financial supervision, auditing, and anti-fraud mechanisms.

Fraud in Sri Lanka’s banking and finance sector has become a growing concern over the past three decades, with major incidents reported from the 1990s to the present, including large-scale financial scams, insider fraud, money laundering, document forgery, loan irregularities, and illegal pyramid schemes. Several of these cases have resulted in significant financial losses and weakened public confidence in banks and financial institutions. The recurrence of such incidents has exposed long-standing weaknesses in regulation, supervision, and corporate governance, while also highlighting gaps in enforcement by authorities. In many instances, fraud has been carried out by individuals within financial institutions who misuse their authority and access for personal gain. Weak oversight, political interference, and outdated or fragmented digital monitoring systems have further limited the ability to detect suspicious activities at an early stage, allowing fraudulent operations to continue for extended periods. The wider economic impact has been substantial, contributing to higher borrowing costs, reduced investor confidence, and increased pressure on regulators, including the Central Bank of Sri Lanka, to strengthen financial supervision, auditing, and anti-fraud mechanisms.

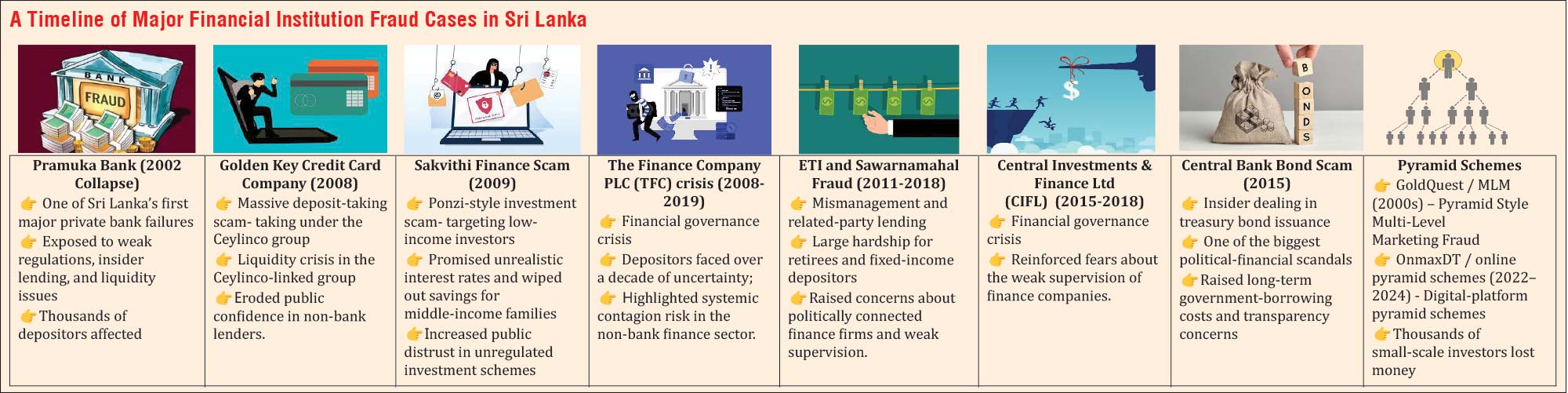

A timeline of major financial institution fraud cases in Sri Lanka

Pramuka Bank (2002 Collapse)

Golden Key Credit Card Company (2008)

Sakvithi Finance Scam (2009)

The Finance Company PLC (TFC) crisis (2008- 2019)

ETI and Sawarnamahal Fraud (2011-2018)

Central Investments & Finance Ltd (CIFL) (2015-2018)

Central Bank Bond Scam (2015)

Pyramid Schemes

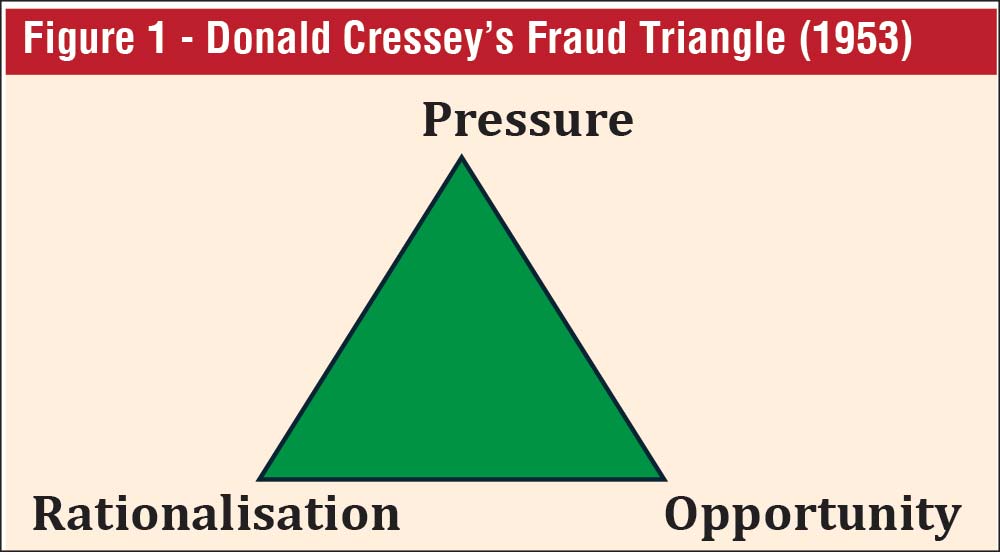

Fraud triangle

Donald Cressey’s Fraud Triangle Theory (1953) remains highly relevant when examining major financial frauds in Sri Lanka. The theory explains that fraud usually occurs when three conditions exist together: pressure, opportunity, and rationalisation. In many Sri Lankan financial scandals, individuals and companies faced strong financial pressure due to debt, competition, or economic instability. At the same time, weak internal controls, poor regulatory supervision, and gaps in monitoring created opportunities for fraud to take place. Many perpetrators also justified their actions by believing the problems were temporary or that future profits would cover the losses.

This theory is important because it helps explain that financial fraud is not only caused by economic problems, but also by human behavior and ethical failures. The repeated collapse of finance companies and pyramid schemes in Sri Lanka shows how weak governance and lack of accountability can encourage fraudulent activities. The Fraud Triangle therefore provides a practical framework for understanding why these financial crimes continue to occur and why stronger regulation, transparency, and ethical standards are necessary to protect depositors and maintain public confidence in the banking and finance sector.

Psychological and behavioural red flags

Psychological and behavioural red flags

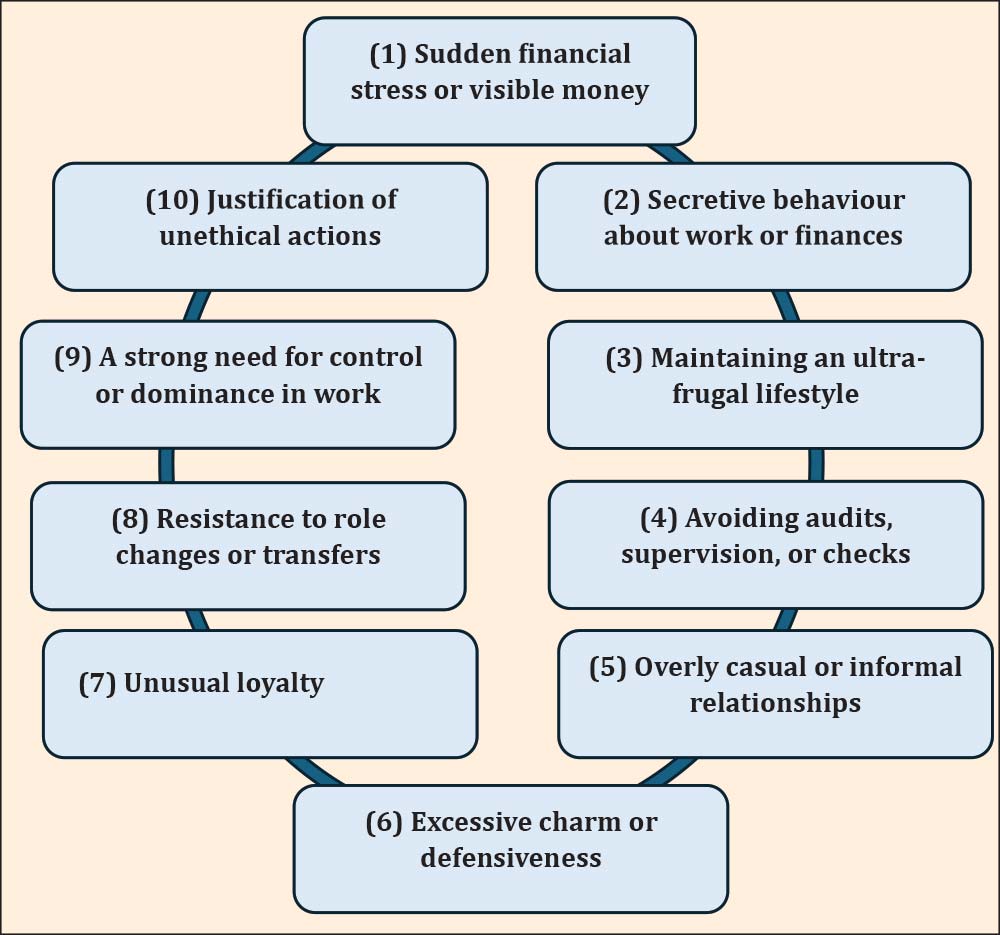

In financial institutions, several psycho-behavioural red flags can be clearly linked to Donald Cressey’s Fraud Triangle of pressure, opportunity, and rationalisation. These include: (1) sudden financial stress or visible money pressure, (2) unusually secretive behaviour about work or finances, (3) maintaining an ultra-frugal or unexplained lifestyle, (4) avoiding audits, supervision, or internal checks, (5) overly casual or informal relationships with colleagues that weaken professional boundaries, (6) excessive charm or defensiveness when questioned, (7) unusual loyalty to certain systems or individuals without clear reason, (8) resistance to role changes or transfers, (9) a strong need for control or dominance in work settings, and (10) justification of unethical actions as “temporary” or “common practice.”

These behaviours directly reflect the Fraud Triangle: pressure is seen in financial stress and hidden struggles, opportunity appears through avoidance of controls and weak oversight, and rationalisation is expressed through justification, charm, or distorted thinking. Together, these red flags are important in financial institutions because they help identify early warning signs of fraud risk before actual misconduct escalates.

1. Sudden financial pressure or visible money pressure refers to situations where individuals or organisations face serious financial difficulties, including heavy debt, cash shortages, business losses, or pressure to maintain a high social status or lifestyle. These conditions can create strong motivation to obtain money quickly or conceal financial problems through dishonest actions. A well-known global example is the Bernard Madoff Ponzi scheme in 2008, where continuous investor withdrawal demands forced Madoff to use funds from new investors to pay existing clients, allowing the fraud to continue for years. Similar patterns were observed in several Sri Lankan financial institution frauds, where financial stress and liquidity problems reportedly contributed to unethical practices, misuse of depositor funds, and unrealistic promises of high returns.

2. Secretive behaviour about work or finances involves situations where individuals intentionally hiding financial activities, limiting access to records, or avoiding transparency in their work. This is considered a major fraud red flag because dishonest actions are easier to conceal from supervisors, auditors, and colleagues. A well-known example is the Enron scandal in 2001, where executives used hidden accounting methods to conceal major financial losses from investors and regulators. Similar behaviour can appear in Sri Lankan financial institution frauds when employees or management hide transaction details, manipulate loan approvals, or avoid proper reporting. Such secrecy often delays detection and allows fraudulent activities to continue unnoticed for long periods.

3. Maintaining an ultra-frugal or unexplained lifestyle refers to situations where individuals intentionally avoid displaying wealth or luxury despite having significant financial resources. This behaviour can reduce suspicion and help conceal hidden financial activities or illicit gains. A well-known example is the Enron scandal, where CFO Andrew Fastow maintained a modest personal lifestyle while managing complex fraudulent financial structures worth billions of dollars. In Sri Lankan financial institution frauds, similar behaviour may appear when employees or managers live unusually simple lifestyles despite having access to large amounts of money or financial authority. This red flag is important because concealed financial behaviour can delay suspicion and allow fraudulent activities to continue unnoticed.

4. Avoidance of audits, supervision, or internal controls occurs when individuals resist reviews, delay inspections, or bypass verification procedures to avoid scrutiny. This is an important fraud red flag because weak oversight creates opportunities to hide dishonest activities. A well-known example is the WorldCom fraud in 2002, where executives manipulated accounting records and avoided proper internal review systems to conceal billions in expenses. Similar behaviour can occur in Sri Lankan financial institutions when employees delay audits, avoid documentation checks, or bypass approval procedures to hide irregular transactions or unauthorised financial activities.

5. Overly casual and informal workplace relationships refer to situations where personal friendships replace professional accountability and formal procedures. This weakens internal controls and makes it easier for fraudulent activities to go unnoticed. A well-known example is the Satyam scandal in 2009, where excessive trust among senior employees allowed financial statement manipulation to continue for years without proper scrutiny. Similar situations can occur in Sri Lankan financial institutions when close relationships between loan officers, managers, or clients influence decisions and reduce independent oversight. Such informal practices can increase the risk of biased approvals, policy violations, and financial fraud within banking and finance institutions.

6. Charm under pressure or defensive communication refers to situations where individuals use confidence, persuasion, or emotional control to avoid suspicion or difficult questioning. This behaviour can hide inconsistencies and reduce scrutiny during investigations. A well-known example is the Theranos case in 2018, where Elizabeth Holmes used strong charisma and carefully controlled communication to maintain investor trust despite serious technological failures. Similar behaviour can appear in Sri Lankan financial institutions when employees become overly defensive or excessively persuasive during audits or questioning, potentially attempting to divert attention from irregular transactions or fraudulent activities.

7. Unusual loyalties to certain systems or individuals without a clear professional reason mean showing strong allegiance to specific people, clients, or processes that cannot be justified by work responsibilities. This behavior can sometimes hide collusion or shared financial benefit. In the Parmalat scandal (2003), internal loyalty networks helped conceal a €14 billion accounting fraud for years. Similarly, in Sri Lankan financial institutions, unexplained loyalty between staff and certain clients or senior officials may discourage reporting of suspicious transactions or financial irregularities.

8. Resistance to job rotation or transfer is when an employee strongly avoids being moved to another role or department, especially in sensitive areas. This is a fraud risk because staying in one position too long allows a person to control processes without oversight. In the HealthSouth case (2003), long-term control over accounting roles enabled large-scale financial manipulation. Similarly, in Sri Lankan banks, reluctance to leave roles like loan processing or cash handling may suggest an attempt to hide or continue fraudulent activities.

9. Strong need for control or dominance in workplace decisions refers to a behaviour where an individual tries to concentrate authority, limit sharing of responsibilities, and reduce independent oversight. This increases fraud risk because it weakens transparency and prevents proper checks. In the Enron case, senior executives controlled financial reporting systems and restricted independent review, enabling large-scale manipulation. Similarly, in Sri Lankan financial institutions, employees who resist delegation or limit access to information may be trying to hide irregular activities or avoid detection of errors or fraud.

10.Rationalisation of unethical behaviour as “normal” or “temporary” means justifying wrong actions by convincing oneself they are acceptable or only short-term, which reduces guilt and makes fraud easier to continue. In the Bernard Madoff case (2008), fraudulent activities were normalised within the organisation, allowing the scheme to operate for many years. Similarly, in Sri Lankan financial institutions, employees who describe rule-breaking as “standard practice” or “temporary adjustment” may gradually engage in more serious financial misconduct over time.

Integrated Risk Management Framework

Integrated Risk Management Framework

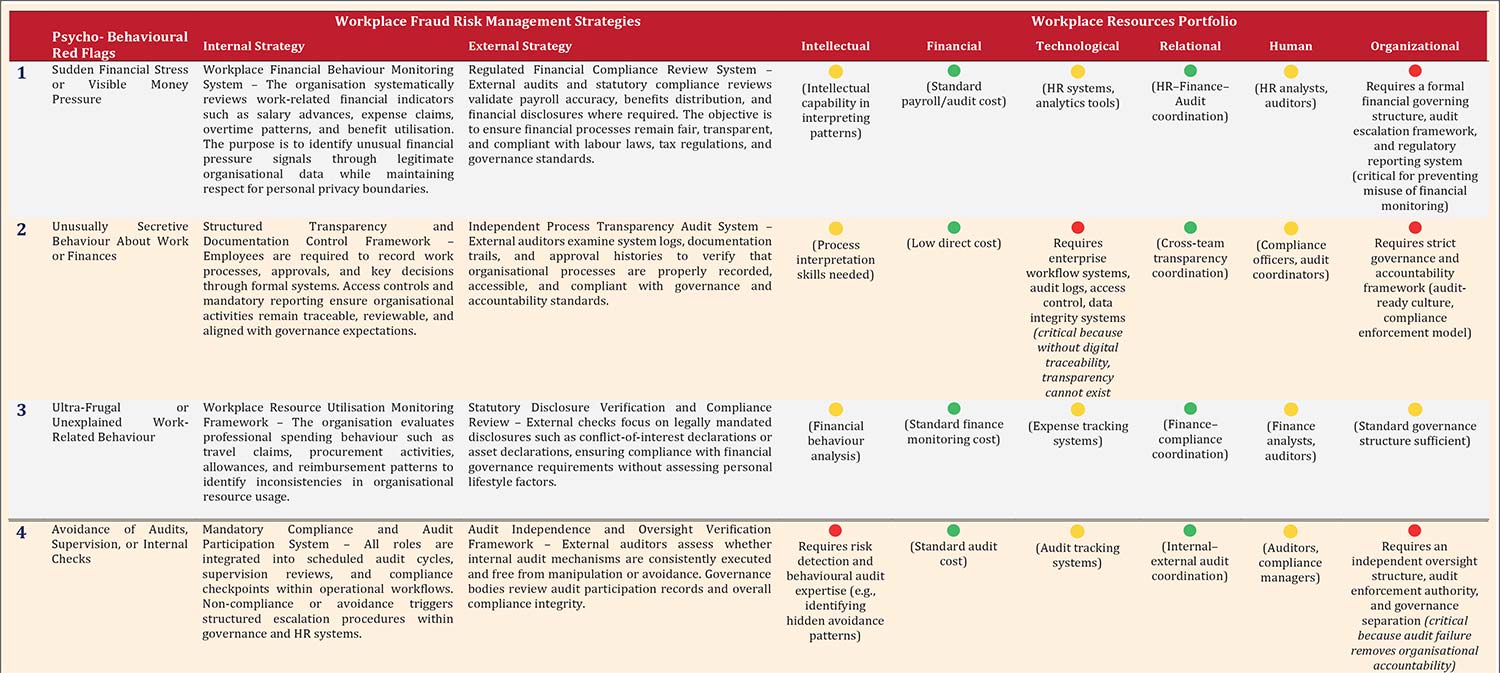

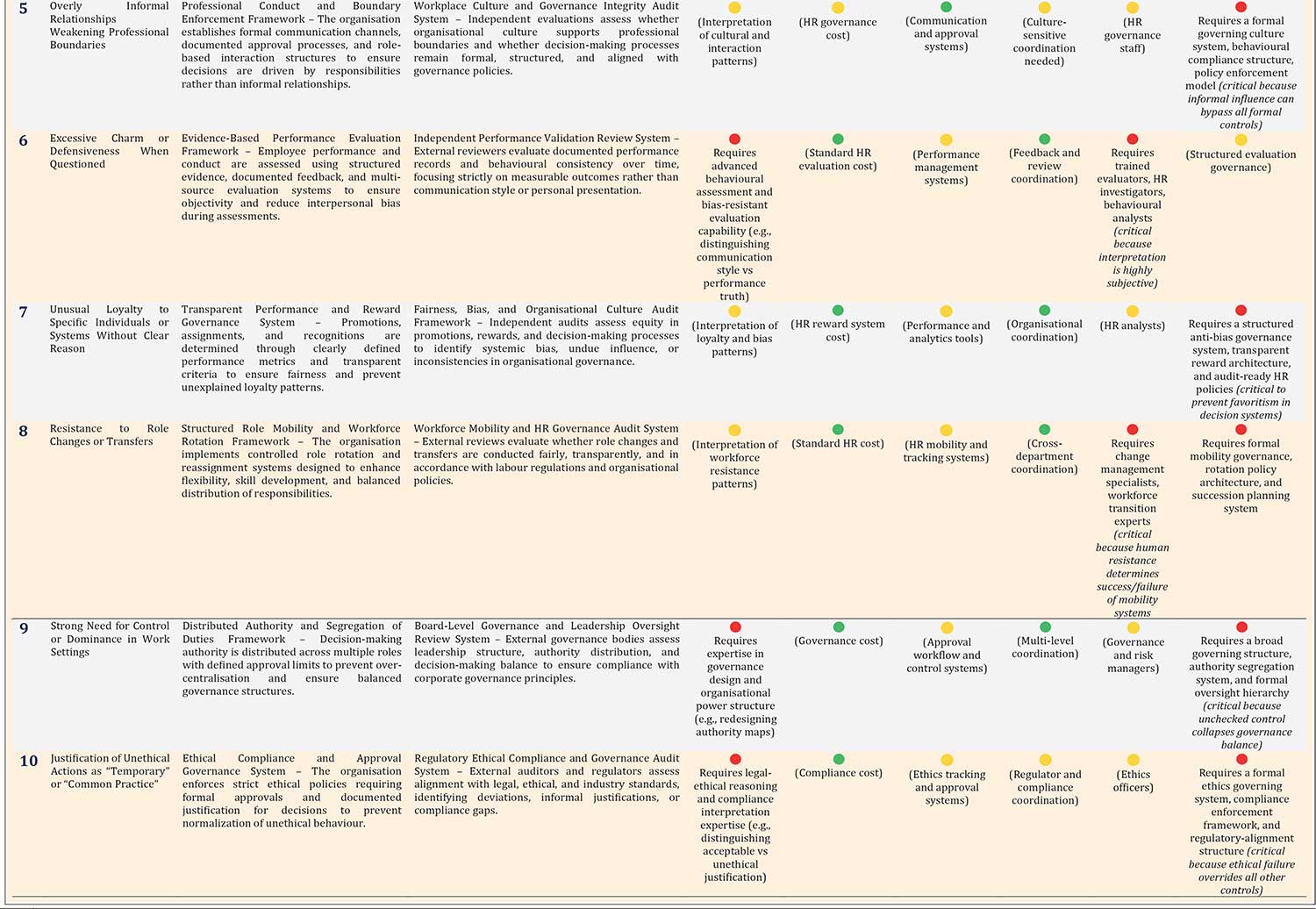

The table provides a structured framework for managing ten psycho-behavioural red flags associated with potential fraud risk in financial institutions. These red flags may not directly show fraud, but they indicate behaviours that need attention. For each red flag, the framework suggests internal and external strategies. Internal strategies strengthen organisational controls. These include clear documentation, close monitoring, defined role responsibilities, and regular performance evaluation. These controls help detect unusual behaviour early and reduce opportunities for misuse of authority. External strategies add independent assurance. These include external audits, regulatory inspections, and governance reviews. Together, both strategies improve transparency, accountability, and early risk detection while respecting employee privacy.

To apply these strategies effectively, organisations need strong and balanced resources. Based on the Resource-Based View (RBV), six key resource types are required. These are intellectual, financial, technological, relational, human, and organisational resources. Intellectual resources help interpret behavioural patterns and identify risk signals. Financial resources support the cost of systems and controls. Technological resources enable monitoring tools and secure data systems. Human resources ensures skilled staff can manage and analyse risk. Relational resources support coordination with regulators and auditors. Organisational resources ensure strong governance and clear structures.

To apply these strategies effectively, organisations need strong and balanced resources. Based on the Resource-Based View (RBV), six key resource types are required. These are intellectual, financial, technological, relational, human, and organisational resources. Intellectual resources help interpret behavioural patterns and identify risk signals. Financial resources support the cost of systems and controls. Technological resources enable monitoring tools and secure data systems. Human resources ensures skilled staff can manage and analyse risk. Relational resources support coordination with regulators and auditors. Organisational resources ensure strong governance and clear structures.

The framework also shows that fraud risk management is not dependent on one resource alone. Instead, it depends on how all resources work together as an integrated system. The traffic light system explains resource intensity.

This system helps organisations quickly understand priorities and allocate resources effectively for managing behavioural fraud risks.

(Pethmi Omalka De Silva is PhD Candidate, Postgraduate Institute of Management (PIM), University of Sri Jayewardenepura; Professor Madurika Nanayakkara, Professor in Finance, University of Kelaniya; and Dr. Ravi Bamunusinghe, Senior Lecturer, Postgraduate Institute of Management (PIM), University of Sri Jayewardenepura)