The revised tax framework significantly eases the financial pressure on importers by introducing predictable and manageable tax costs. This improves cash flow stability and enables better business planning, particularly for small and medium-scale operators. Lower tax exposure reduces the incentive for under-invoicing and informal trading practices, thereby promoting greater compliance, transparency, and regulatory discipline across the sector. With taxes no longer acting as a major deterrent, gem imports are expected to recover steadily, ensuring a consistent supply of raw materials for downstream value-added activities. Improved availability of raw gems will strengthen cutting, polishing, and jewellery manufacturing operations, enhancing Sri Lanka’s export competitiveness. Importantly, the reduced tax burden lowers entry barriers for new businesses and creates opportunities for young entrepreneurs to enter gem importing, lapidary work, jewellery manufacturing, and re-export operations.

Strategic importance for Sri Lanka’s economy

The gem and jewellery sector plays a vital role in export earnings, employment generation, rural economic development, and tourism-linked retail trade. Sri Lanka is internationally recognised for its blue sapphires, cat’s eye chrysoberyl, and a wide range of precious and semi-precious stones. Maintaining competitiveness therefore requires not only product quality, but also a supportive and realistic policy environment.

Should Income Tax exemptions on gem exports be reconsidered?

Historically, income earned from gem exports in Sri Lanka was exempt from Income Tax, a policy that helped position the country as a competitive global gem trading hub. The removal of this exemption, though intended to broaden the tax base, has reduced Sri Lanka’s relative attractiveness compared to competing gem-exporting centres such as Thailand, Hong Kong, Dubai, and certain African markets. Given Sri Lanka’s urgent need for foreign exchange and economic recovery, policymakers may need to reconsider targeted tax incentives for strategic export industries such as gems and jewellery.

The international gem trade is highly mobile, with traders and processors able to relocate quickly to jurisdictions offering lower tax burdens, faster regulatory approvals, and export-friendly policies. Reintroducing Income Tax exemptions could attract international gem traders to Sri Lanka, encourage regional trading hubs to relocate operations, and increase re-export and processing activity.

Gem exports generate high-value foreign currency earnings with relatively low import dependency. Even modest export growth can significantly strengthen the balance of payments, stabilise the exchange rate, and support essential imports. In this context, tax exemptions should be viewed not as revenue losses, but as strategic investments that multiply foreign currency inflows and long-term fiscal sustainability.

Policy balance and way forward

The experience of 2024–2025 demonstrates that excessive tax pressure can be counterproductive. Lower import volumes reduce VAT collections, export earnings, employment contributions, and foreign exchange inflows. The revised tax model adopts a balanced approach that ensures reasonable revenue for the Treasury while supporting industry sustainability and long-term growth.

To maximise the benefits of the new regime, policymakers and industry stakeholders should streamline Customs procedures, enhance gem certification and valuation standards, expand lapidary training programmes, promote Sri Lanka’s gem brand internationally, and develop digital gem trading platforms.

Conclusion

The revised SSCL and VAT calculation method marks a positive turning point for Sri Lanka’s gem and jewellery industry. By replacing a value-based tax system with a fixed-rate model, the Government has addressed industry concerns, reduced operational costs, and reopened growth opportunities for importers and exporters alike. Reconsidering targeted Income Tax exemptions on gem export income could further transform Sri Lanka into a global business hub for gemstones, boosting foreign exchange inflows, creating employment, and strengthening economic resilience. With renewed investor confidence and a supportive fiscal framework, Sri Lanka’s gem sector is well positioned to reclaim its place on the world stage.

(The author is a Chartered Accountant)

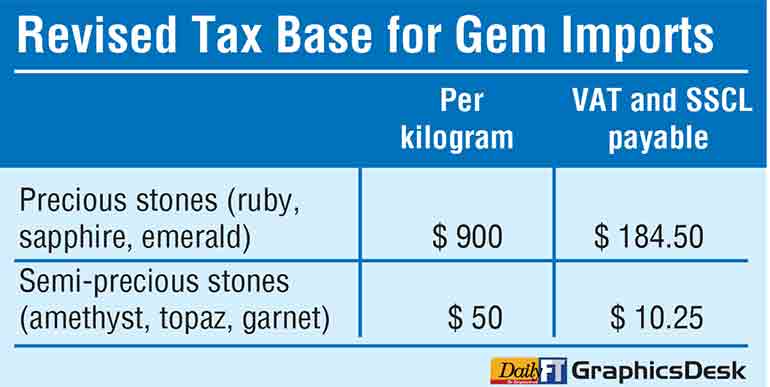

Sri Lanka’s globally renowned gem and jewellery industry has received a timely boost with the introduction of a revised tax calculation method for gem imports. The new framework for applying the Social Security Contribution Levy (SSCL) and Value Added Tax (VAT) is expected to ease the financial burden on importers, revive declining import volumes, and strengthen the country’s gem export performance.

Sri Lanka’s globally renowned gem and jewellery industry has received a timely boost with the introduction of a revised tax calculation method for gem imports. The new framework for applying the Social Security Contribution Levy (SSCL) and Value Added Tax (VAT) is expected to ease the financial burden on importers, revive declining import volumes, and strengthen the country’s gem export performance.