Thursday Jul 16, 2026

Thursday Jul 16, 2026

Tuesday, 3 March 2026 05:45 - - {{hitsCtrl.values.hits}}

File photo of shipping in the Strait of Hormuz, which has now ground to a halt

Moody’s Analytics has published the following new comment on the implications of conflict in the Middle East over Asia Pacific economies.

Escalating hostilities in the Middle East risk renewed energy, trade and inflation shocks.

Conflict in the Middle East intensified over the weekend as the U.S. and Israel launched military strikes on targets in Iran. Tehran retaliated with missiles and drones aimed at Israel and countries hosting U.S. forces, including the United Arab Emirates, Qatar, Kuwait, Bahrain, Iraq, Jordan and Saudi Arabia. Media reports suggest the conflict has led to the effective closure of the Strait of Hormuz, a major oil shipping route. This raises the risk of further disruptions in the Red Sea and across the wider Middle East. Airspace closures have compounded the strain, affecting passenger travel and cargo flows through one of the world’s most important trade corridors.

Asia is particularly exposed as it buys the lion’s share of oil and gas produced in the region. Roughly a third of global seaborne crude oil exports pass through the Strait of Hormuz, with most volumes destined for large Asian economies such as China, India, Japan and South Korea. Around 20% of global liquefied natural gas shipments also transit the strait. Brent crude oil prices jumped to around $80 per barrel in early Monday trading in Asia, up from around $72 per barrel at the close on Friday, while equity markets slipped in initial trading.

A broader or more drawn-out conflict would risk increasing the strain on emerging Asian economies that have, in past years, struggled with external debt repayment. the surge in energy and food prices after Russia’s invasion of Ukraine played a key role in the crises in Sri Lanka, Bangladesh and Pakistan. A sustained disruption to Gulf oil exports or maritime traffic could revive debt concerns

The conflict injects fresh uncertainty into the trade outlook. Although China is a major buyer of Iran’s discounted crude oil, it maintains sizeable reserves that could cushion short-term supply disruptions. Chinese officials have called for an immediate cessation of military operations. But renewed tensions with the U.S. cast a shadow over the upcoming China-U.S. presidential meeting and add uncertainty to their already fragile trade truce. The conflict also complicates matters for India, which imports large amounts of Middle East oil and has agreed to wind down purchases of Russian oil as part of a trade deal with the U.S.—a deal which now sits in limbo after the U.S. Supreme Court struck down U.S. President Donald Trump’s country-based tariffs.

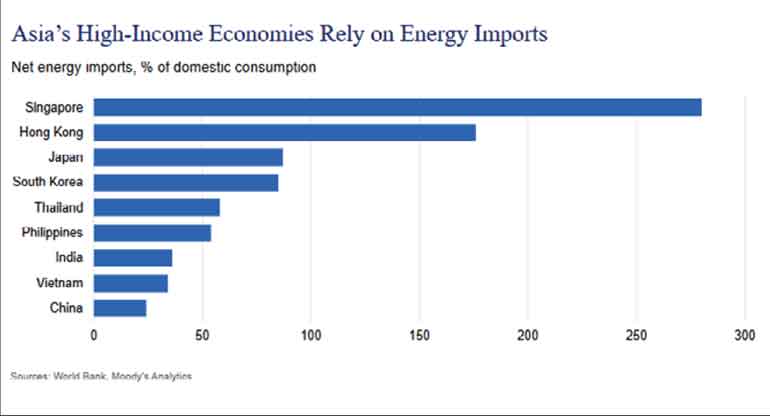

Asia’s high-income economies, which heavily rely on commodity imports, are particularly vulnerable to the direct economic fallout from the conflict. Japan, South Korea, Taiwan (China), Singapore and Hong Kong import more than 80% of the energy they consume domestically. They also depend heavily on food imports. Higher commodity prices would raise consumer and producer inflation, potentially forcing central banks to pause their easing cycles or even raise policy rates. Higher prices would also inflate import bills, weakening trade balances. As imports become more costly, greater financial outflows would weaken currencies.

A broader or more drawn-out conflict would risk increasing the strain on emerging Asian economies that have, in past years, struggled with external debt repayment. The surge in energy and food prices after Russia’s invasion of Ukraine played a key role in the crises in Sri Lanka, Bangladesh and Pakistan. A sustained disruption to Gulf oil exports or maritime traffic could revive debt concerns.

We are monitoring developments and assessing the implications for our baseline forecast, which we plan to publish next week. Our S6 alternative scenario examines the effects of more severe trade and supply-chain disruptions and higher commodity prices.