Thursday Jun 04, 2026

Thursday Jun 04, 2026

Wednesday, 27 May 2026 00:02 - - {{hitsCtrl.values.hits}}

In 2022, Sri Lanka did not simply run out of foreign exchange. It ran out of fuel. Power cuts stretched to thirteen hours a day. Factories fell silent. Hospitals rationed generators. Long queues for petrol became the defining image of a nation's unraveling. The energy crisis was not a symptom of the economic collapse — it was one of its primary causes.

In 2022, Sri Lanka did not simply run out of foreign exchange. It ran out of fuel. Power cuts stretched to thirteen hours a day. Factories fell silent. Hospitals rationed generators. Long queues for petrol became the defining image of a nation's unraveling. The energy crisis was not a symptom of the economic collapse — it was one of its primary causes.

Four years on, the emergency has faded but the structural wound remains wide open. Electricity tariffs have swung violently between politically motivated cuts and IMF-mandated hikes, leaving households and industries alike in a state of chronic uncertainty. Meanwhile, Sri Lanka's regional competitors — Bangladesh, Pakistan, India — continue to export goods at prices Sri Lanka simply cannot match. The reason, more often than not, comes down to one line item: the cost of electricity.

This is the story of how an energy policy failure became an economic pain point — and what it will take to reverse it.

Anatomy of an energy-driven economic crisis

Sri Lanka's relationship with energy is structurally precarious. Unlike Nepal or Bhutan, which sit atop vast hydropower reserves, or India and Pakistan, which hold domestic coal reserves, Sri Lanka imports the overwhelming majority of its primary energy — oil, coal, and increasingly liquefied natural gas (LNG). This dependence is not a recent policy failure or the result of any single crisis. It is a decades-long structural condition that has been allowed to deepen without serious corrective action.

The arithmetic is unforgiving. Crude oil and petroleum imports grew from $ 752 million in 2010 to over $ 2 billion annually by the late 2010s — and when global oil prices surged in the early 2020s, the bill became catastrophic, accounting for an estimated 27% of total import costs. A 2023 study found that imported fuels consumed up to 50% of Sri Lanka's export income in crisis years — a level of exposure that would be considered reckless in any serious national planning framework.

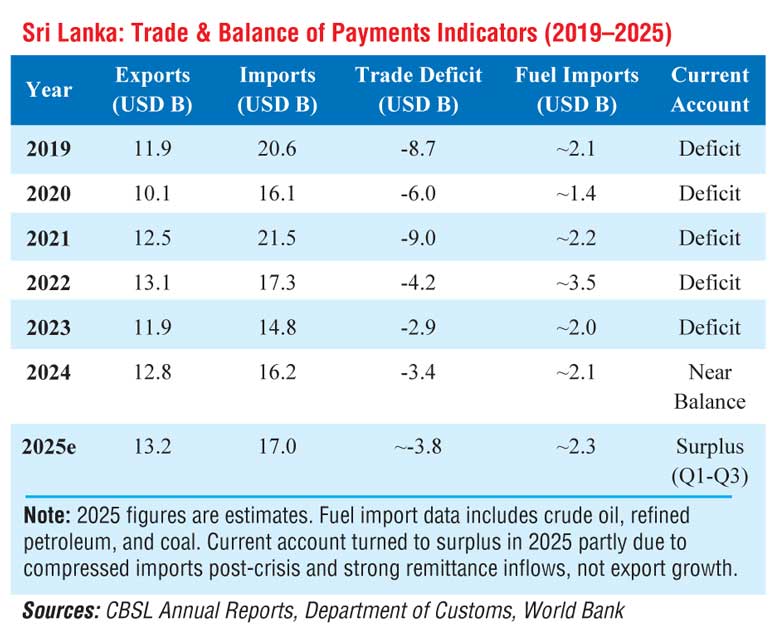

Every dollar spent on fuel imports is a dollar that drains foreign reserves. When oil prices rise in Rotterdam or coal prices spike in Indonesia, Sri Lanka's economy feels it immediately — at the factory floor, in the household electricity bill, and ultimately in the foreign exchange position that underpins the entire financial system. The 2022 crisis, which saw foreign reserves collapse to $ 1.7 billion and the country default on its sovereign debt, was not the product of any single external shock. It was the culmination of two decades of unaddressed fuel import dependency.

Tariff whiplash: When policy becomes its own crisis

Between August 2022 and February 2023, the Ceylon Electricity Board (CEB) raised electricity tariffs by 75% and then 66% respectively — among the steepest increases in the region's recent history. The hikes were not arbitrary. They were required under Sri Lanka's $ 2.9 billion IMF Extended Fund Facility agreement, which demanded cost-reflective pricing as a condition of continued program support.

For households already battered by inflation, the increases were devastating. Survey data from 2024 found that 31% of Sri Lankan families considered electricity unaffordable — even after partial tariff reductions introduced later that year. Industries faced even starker pressures. Apparel factories in Free Trade Zones reported tariff increases of 8% to 30% on their industrial rates, squeezing margins that were already thin in a globally competitive sector.

Then came the political whiplash. The newly elected National People's Power (NPP) Government, which had campaigned on promises of dramatically lower electricity bills, implemented a tariff cut in January 2025. The move was popular. It was also financially ruinous. The CEB, already struggling with hydropower deficits from a dry season and costly thermal generation, swung into loss. By June 2025, the IMF required a course correction: tariffs were raised again, more than 20% for industrial consumers, partially reversing the relief households had just begun to feel.

The Vicious Cycle of Tariff Populism

Political pressure drives tariff cuts → CEB incurs losses → IMF conditions require restoration → tariffs spike → public anger → political pressure for cuts. Each rotation of this cycle erodes investor confidence, destabilises industrial planning, and delays the structural reforms that could break it.

This cycle — tariff populism followed by IMF-mandated correction — is not merely a political headache. It represents a systemic failure to build a financially sustainable energy sector. And it has direct, quantifiable consequences for the broader economy.

The competitiveness gap: How high electricity costs are killing exports

Sri Lanka's apparel and textile sector accounts for more than 50% of total export earnings. It is, in every sense, the engine of the nation's foreign exchange. It is also among the most electricity-intensive manufacturing categories. And it is losing ground — not because of tariffs at its destination markets, but because of the cost of keeping the lights on at home.

The Bangladesh benchmark

Consider Sri Lanka's position in the United Kingdom market. Under the Developing Countries Trading Scheme (DCTS), Sri Lanka enjoys 0% tariff access for virtually all goods exported to the UK. Bangladesh enjoys the same. On paper, both nations compete on equal footing.

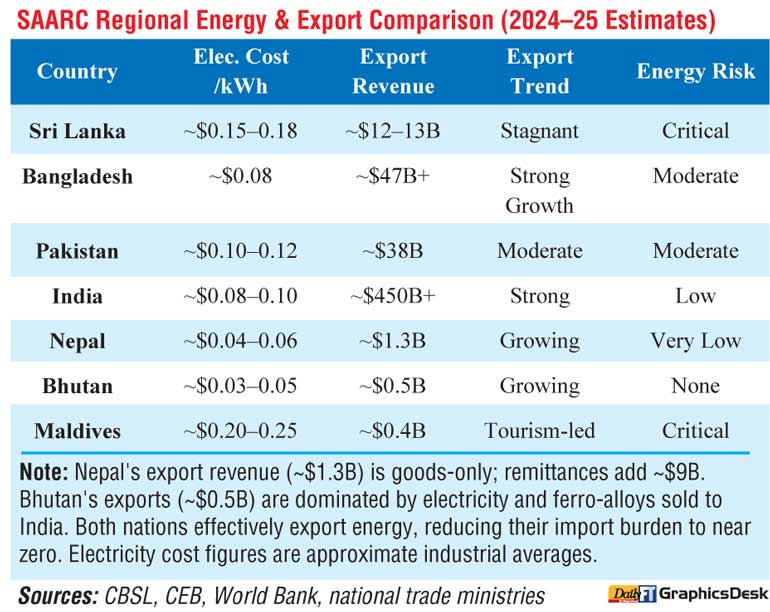

In practice, they do not. Bangladesh's average industrial electricity tariff sits at approximately $0.08 per kilowatt-hour. Sri Lanka's ranges between $0.15 and $0.18 per kWh — nearly double. For a garment factory running energy-intensive machinery across multiple shifts, this differential translates directly into lower production costs, thinner prices, and greater price competitiveness in UK retail.

The result is predictable. UK importers, when comparing comparable quality garments from Sri Lanka and Bangladesh, consistently find Bangladeshi imports cheaper. The tariff advantage Sri Lanka theoretically holds — the product of years of diplomatic effort and trade policy — is effectively neutralised by the cost of domestic electricity.

This is not a hypothetical risk. Sri Lanka's export revenue has stagnated in the range of USD 12–13 billion annually, while Bangladesh has surged past USD 47 billion to become the world's second-largest apparel exporter after China. Pakistan, also running higher industrial electricity costs than Bangladesh but lower than Sri Lanka, has grown exports to approximately USD 38 billion.

The ripple effects

The export competitiveness problem does not stop at garments. Tea processing, rubber manufacturing, food production, and fisheries all rely on electricity as a direct input cost. When tariffs rise, processing margins compress. When margins compress, export prices must rise or production volumes must fall. Either outcome weakens Sri Lanka's position in global commodity markets where price is the primary competitive variable.

The National Chamber of Exporters has repeatedly flagged that tariff hikes are eroding profit margins and jeopardising competitiveness. Chambers of commerce warn that foreign exchange earnings — the lifeblood of a dollarised debt-servicing economy — are at structural risk. These are not alarmist projections. They are the arithmetic of energy-cost pass-through in an export-dependent economy.

Balance of payments trap

Energy costs do not only affect export revenue. They shape the entire balance of payments position — simultaneously suppressing the export income side of the ledger while inflating the import expenditure side.

Sri Lanka's fuel import bill is among the largest categories of foreign exchange outflow. Every kilowatt-hour generated from imported coal or oil represents a claim on the nation's scarce dollar reserves. In dry seasons, when hydropower generation falls, the CEB ramps up thermal generation — purchasing fuel on international spot markets at premium prices and paying in hard currency. This pattern repeats annually with predictable consequences: higher generation costs, higher tariffs, and a wider current account deficit.

Meanwhile, lower export revenues mean fewer dollar inflows. The combination — high import bills and weak export earnings — maintains persistent pressure on the rupee, making imported inputs even more expensive in local currency terms, which in turn raises production costs further. It is a trap that tightens with each rotation.

Sri Lanka's neighbours have managed this dynamic with varying degrees of success. Nepal and Bhutan, endowed with surplus hydropower, have turned energy into an export commodity, selling electricity to India and accumulating foreign exchange in the process. Bangladesh has leveraged domestic natural gas reserves — though those are depleting — and aggressive solar park deployment to keep industrial tariffs competitive. Pakistan, despite its structural inefficiencies, has diversified its generation mix through nuclear capacity and is rapidly expanding solar to reduce fuel import dependence.

Sri Lanka, by contrast, has substantial untapped renewable potential — particularly in solar — but has struggled to translate that potential into grid-connected capacity at scale.

Solar paradox: Potential without absorption

Sri Lanka receives some of the highest solar irradiation in South Asia. The theoretical case for a solar-led energy transition is compelling: abundant resource, rapidly falling panel costs, and a geographic footprint that suits distributed rooftop generation. Solar deployment has in fact accelerated significantly since 2022, driven partly by households seeking relief from high tariffs and partly by policy incentives for rooftop systems.

The problem is not generation. It is absorption. Sri Lanka's transmission and distribution network was not designed to accommodate large volumes of intermittent renewable energy. During peak daylight hours, solar generation can exceed what the grid is able to absorb, store, or redistribute. Without battery storage systems, pumped hydro facilities, or smart grid infrastructure capable of managing variable input, solar power is wasted at precisely the moment it is most abundantly available.

This is not an unsolvable problem — it is an investment and execution problem. Bangladesh is deploying solar parks with dedicated transmission infrastructure. Pakistan is integrating large-scale solar with wind and hydro in hybrid projects to improve grid stability. Even the Maldives, operating at a fraction of Sri Lanka's scale, has piloted battery storage programs to reduce diesel dependency.

Sri Lanka's grid modernisation has lagged behind its renewable ambitions. Policy timelines for smart grid investment, storage procurement, and regional interconnection have moved slowly against a backdrop of fiscal austerity and shifting political priorities. The result is that the nation has access to an essentially free fuel source — sunlight — but lacks the infrastructure to fully exploit it.

Path forward: What structural reform actually requires

Breaking Sri Lanka's energy-economy trap requires more than tariff adjustments. It requires structural transformation across four interconnected dimensions.

1. Grid modernisation and storage investment: Expanding solar and wind capacity without simultaneously upgrading grid infrastructure will only shift the bottleneck, not remove it. Sri Lanka needs sustained capital investment in transmission upgrades, battery storage facilities, and smart grid technology that can manage variable renewable input. This is capital-intensive but commercially viable — and international climate financing, through mechanisms such as the Just Energy Transition Partnership framework, can help bridge the funding gap.

2. Regional energy cooperation: Sri Lanka does not need to solve its energy security problem alone. The SAARC region contains substantial complementary energy assets: Nepal and Bhutan have surplus hydropower that could stabilise Sri Lanka's dry-season demand; India has an expanding renewable sector with growing regional transmission ambitions. Bilateral energy trade agreements — modest in diplomatic complexity but significant in economic impact — could buffer seasonal volatility, reduce thermal generation costs, and improve tariff stability.

3. Demand planning and industrial policy alignment: Sri Lanka has historically practiced reactive energy planning — building capacity in response to crises rather than in anticipation of demand. Bangladesh, Pakistan, and Nepal have more structured forecasting systems tied to industrial growth projections and hydropower seasonality. Sri Lanka needs a long-term national energy demand plan that is integrated with industrial policy, export strategy, and fiscal planning — and that is insulated from the short election cycles that have driven tariff populism.

4. Tariff rationalisation with social protection: Cost-reflective electricity pricing is fiscally necessary and economically sound. But the social pain of sharp tariff increases falls disproportionately on low-income households — a distributional failure that generates political backlash and drives the populist cuts that undermine financial sustainability. Sri Lanka needs a tiered tariff architecture that maintains industrial cost-competitiveness, ensures CEB financial viability, and provides targeted subsidies to vulnerable households — rather than the blunt instrument of across-the-board cuts that benefit the wealthy and undermine the utility's balance sheet.

FDI dimension: How electricity costs shape investment decisions

The electricity tariff problem does not only affect existing businesses. It shapes the decisions of foreign investors before they arrive — and in many cases, prevents them from arriving at all. Foreign direct investment is not simply a measure of confidence in a country’s future. It is a forward-looking cost calculation. When investors evaluate manufacturing or export-oriented projects, energy reliability and cost rank among the top three site-selection criteria, alongside labour costs and regulatory stability. Sri Lanka’s persistent tariff volatility and elevated industrial electricity costs have quietly become one of the most significant deterrents to the large-scale, job-creating FDI the country requires.

Three years of FDI performance: 2022–2025

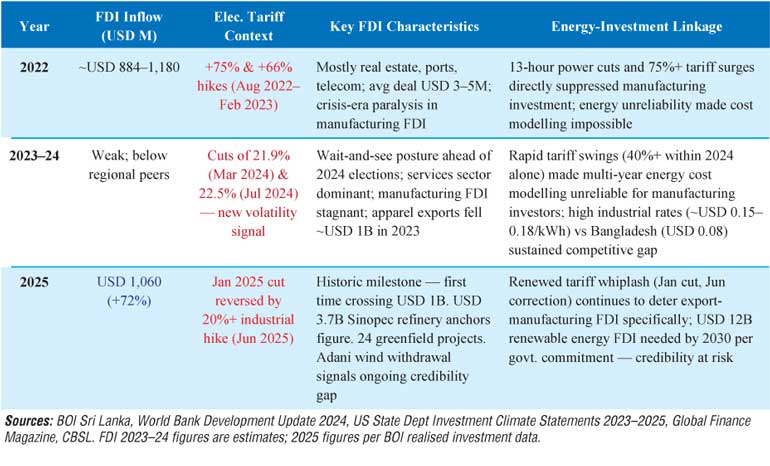

Sri Lanka’s FDI trajectory over the past three years reflects both the depth of the 2022 crisis and the slow, uneven recovery since. In 2022 — the year of the collapse — gross FDI including foreign loans reached approximately USD 1.18 billion, elevated partly by crisis-era infrastructure commitments and import-substitution investments rather than new productive capacity. Beneath that headline figure, however, the investment climate was deteriorating sharply: the combination of 13-hour power cuts, industrial tariff surges of 75% and 66% in rapid succession, and extreme macroeconomic uncertainty made Sri Lanka one of the least attractive manufacturing destinations in South Asia. Most FDI transactions during this period remained in the USD 3 to 5 million range — modest, cautious, and heavily concentrated in real estate, ports, and telecommunications rather than the export-oriented manufacturing the economy requires.

In 2023 and 2024, FDI flows remained structurally weak even as macroeconomic stabilisation progressed. The IMF program provided external discipline, and inflation fell dramatically from its 2022 peak. But tariff volatility continued to undermine investor confidence: the 2024 tariff reductions — a 21.9% cut in March followed by a further 22.5% reduction in July — while welcome for households, introduced a new form of uncertainty. Investors evaluating 10-to-20-year manufacturing projects cannot model energy costs when tariff policy shifts by over 40% within a single calendar year. The World Bank’s October 2024 Development Update noted explicitly that Sri Lanka’s FDI inflows had remained below regional peers for decades, concentrated in services rather than in the productive, job-intensive sectors that drive export growth.

By 2025, there are more encouraging signs — but the picture remains mixed. The Board of Investment reported that realised FDI reached a historic USD 1.06 billion in 2025, representing a 72% surge from prior years and crossing the billion-dollar threshold for the first time. The first quarter alone recorded USD 203 million in realised FDI, a 90% increase on the same period in 2024. Investment proposals at mid-year 2025 totalled $ 4.67 billion, with 40 greenfield projects reflecting genuine long-term commitment. The $ 3.7 billion Sinopec oil refinery at Hambantota — the largest single FDI commitment in Sri Lanka’s history — anchors this figure. Yet even this milestone carries a caveat: in February 2025, Indian firm Adani Green Energy withdrew from a proposed $ 400 million, 484 MW wind energy project in the north, citing Government attempts to renegotiate a previously awarded contract. The episode illustrated precisely the reputational damage that policy instability inflicts on investor confidence.

What investors are actually saying

The pattern across three years is consistent. Experienced investors in Sri Lanka emphasise that policy stability, regulatory reform, and improved transparency must precede any significant uptick in large-scale investment — and that energy cost predictability sits at the centre of those concerns. The Government’s own target of USD 5 billion in FDI by 2025 has been missed; the USD 1.06 billion achieved, while a milestone, reflects how far Sri Lanka remains from attracting the volume and quality of investment needed to structurally transform the economy.

The electricity tariff dimension is not peripheral to this assessment — it is structural. An investor evaluating a garment or light manufacturing facility in Sri Lanka faces a simple arithmetic: electricity costs roughly twice what the same facility would pay in Bangladesh. That differential, compounded by the risk that the tariff could shift by 20–40% within a single year in either direction, makes Sri Lanka a difficult investment case relative to regional alternatives. Until electricity pricing is stable, cost-competitive, and supported by reliable grid infrastructure, Sri Lanka will continue to attract investment at the margin — in ports, services, and real estate — while losing the manufacturing FDI that generates exports, employment, and foreign exchange in the volumes the recovery requires.

Short-term survival vs. long-term sustainability

Sri Lanka’s energy policy has, for the better part of two decades, been governed by the logic of immediate political survival rather than structural economic sustainability. This distinction is not merely rhetorical — it is the central fault line running beneath every tariff decision, every delayed grid investment, and every deferred renewable transition.

Short-term survival thinking produces predictable outputs: tariff cuts timed to electoral cycles, deferred maintenance of generation assets, subsidies that outlast their fiscal justification, and an institutional reluctance to absorb the short-run pain of structural adjustment. Each of these choices is individually defensible in a narrow political window. Cumulatively, they compound into a structural deficit that grows more expensive to remedy with each passing year.

Long-term sustainability, by contrast, demands a different institutional architecture. It requires energy planning horizons that extend beyond the five-year election cycle — anchored in independent regulatory bodies capable of withstanding political pressure, transparent cost-recovery frameworks that insulate tariff-setting from cabinet interference, and capital budgeting processes that treat grid infrastructure as a strategic national asset rather than a discretionary spending line. Bangladesh and India have not escaped political interference in energy pricing, but both have built institutional buffers — sector regulators, long-term capacity auctions, multi-year power purchase agreements — that create durable structural momentum even when Governments change.

The critical tension is this: survival-mode governance is not irrational in a context of acute fiscal stress and public suffering. When thirteen-hour power cuts are the daily reality, political leaders who promise immediate relief are responding to a genuine crisis. The failure is not in addressing the immediate — it is in treating the immediate as the permanent. Sri Lanka’s energy problem will not be resolved by the next tariff announcement. It will be resolved when the institutional framework makes it structurally impossible to sacrifice long-term investment on the altar of short-term electoral arithmetic.

Decision outcomes focused, consequences ignored

Across Sri Lanka’s energy policy history, a recurring pattern emerges: decisions are evaluated by their immediate, visible outcomes — the announcement, the tariff cut, the ribbon-cutting at a new generation facility — while their second and third-order consequences remain largely unexamined, unaccounted for, and politically invisible until they crystallise into the next crisis.

Consider the January 2025 tariff reduction. The outcome was clear and measurable: household electricity bills fell, public approval ratings rose, and the NPP Government delivered on a visible campaign promise. What was not immediately visible were the consequences: the CEB’s balance sheet deteriorating, IMF program benchmarks being missed, and industrial consumers facing a sharper corrective spike months later. The decision was assessed by what it produced; its costs were assessed only when they became unavoidable.

This outcome-focused framing extends beyond tariff policy. Grid modernisation has been deferred because the outcome of investment — stable, affordable, renewable-supplied electricity — is a decade away, while the consequence of deferral — continued thermal dependency and wasted solar capacity — accumulates quietly. Fuel import contracts have been signed under emergency conditions because the outcome of securing supply was immediate, while the consequence of locking in unfavourable pricing terms was absorbed gradually across the balance of payments. Renewable capacity auctions have stalled because their outcomes are commercially complex and institutionally demanding, while the consequence of inaction — a widening competitiveness gap with regional peers — is diffuse and attributable to no single decision-maker.

This governance deficit — consequence-blindness — is not unique to Sri Lanka, but it is particularly damaging in an energy sector where investment decisions carry 20-to-30-year consequences and where policy reversals impose compound costs. The solution is not better intentions; it is better institutional design. Mandatory consequence assessments for major tariff and procurement decisions, independent fiscal impact modelling required before legislative passage, and structured review mechanisms that attribute deferred costs to the decisions that produced them would each contribute to a more accountable decision-making environment. Governance that can see the full cost of its choices — not just the visible outcome — is the prerequisite for an energy sector that serves the economy rather than periodically destabilising it.

Conclusion

The connection between energy costs and economic performance is not abstract. It is visible in every garment that UK importers choose to source from Dhaka rather than Colombo. It is measurable in every dollar of foreign exchange that leaves Sri Lanka to pay for imported coal that keeps the lights on. It is felt by every factory manager calculating whether the next tariff hike will tip a thin margin into a loss.

Sri Lanka's 2022 crisis was widely attributed to foreign exchange mismanagement, tax cuts, and debt accumulation. These were real factors. But the energy dimension of that crisis — the role of import dependence, structural tariff distortions, and underinvestment in renewables — deserves equal weight in the post-crisis diagnosis.

The nation stands at a genuine inflection point. It has established IMF program discipline. It has a nascent solar sector ready to scale. It sits in a region with complementary energy assets it has barely begun to leverage. The question is whether the political will exists to prioritise long-term structural reform over short-term tariff populism.

The lights staying on is not a technical achievement. It is an economic one. And in Sri Lanka's case, it may well determine whether the country builds the export-competitive, resilient economy it needs — or remains trapped in a cycle where energy costs consume the gains that trade policy was supposed to deliver.