Saturday Jul 04, 2026

Saturday Jul 04, 2026

Wednesday, 13 May 2026 04:29 - - {{hitsCtrl.values.hits}}

The UAE has demonstrated, providing investors with a predictable tax environment and unfettered capital mobility naturally builds the monetary base required to maintain a stable, working-currency environment

The strategic realignment of Sri Lanka’s economic architecture, modelled after the proven fiscal and monetary strategies of global hubs like the UAE, represents more than a recovery effort; it is a fundamental shift toward institutional stability and global capital integration. By leveraging the Colombo Port City as such a jurisdiction, Sri Lanka can actively dismantle the historical barriers of currency volatility and regulatory ambiguity that once catalysed capital flight. The transition from the opaque incentive structures of the past to the rules-based governance codified in the 2025 Regulations and 2026 Amendment ensures that the nation can attract high-tier international expertise and foreign direct investment (FDI) without sacrificing long-term fiscal control

Sri Lanka’s economic trajectory has reached a pivotal moment following a severe sovereign debt crisis, prompting a comprehensive restructuring of its financial and fiscal framework to restore stability and international credibility. This shift emphasises fiscal sustainability through rules‑based governance, a predictable tax regime, and mechanisms to channel capital into high‑return strategic sectors, while moving away from fragmented taxation and excessive reliance on indirect revenues. The most visible expression of this transformation is the Colombo Port City, conceived as a multi‑currency Special Economic Zone modelled on global financial hubs such as UAE. Its success hinges on establishing a credible working currency system, where reliable access to dollars is not ad hoc but structurally embedded in the banking system through a rigid currency framework and deep foreign exchange markets.

Sri Lanka’s economic trajectory has reached a pivotal moment following a severe sovereign debt crisis, prompting a comprehensive restructuring of its financial and fiscal framework to restore stability and international credibility. This shift emphasises fiscal sustainability through rules‑based governance, a predictable tax regime, and mechanisms to channel capital into high‑return strategic sectors, while moving away from fragmented taxation and excessive reliance on indirect revenues. The most visible expression of this transformation is the Colombo Port City, conceived as a multi‑currency Special Economic Zone modelled on global financial hubs such as UAE. Its success hinges on establishing a credible working currency system, where reliable access to dollars is not ad hoc but structurally embedded in the banking system through a rigid currency framework and deep foreign exchange markets.

1.Simplicity as a catalyst for capital inflow

A) The UAE’s evolution in corporate taxation and compliance

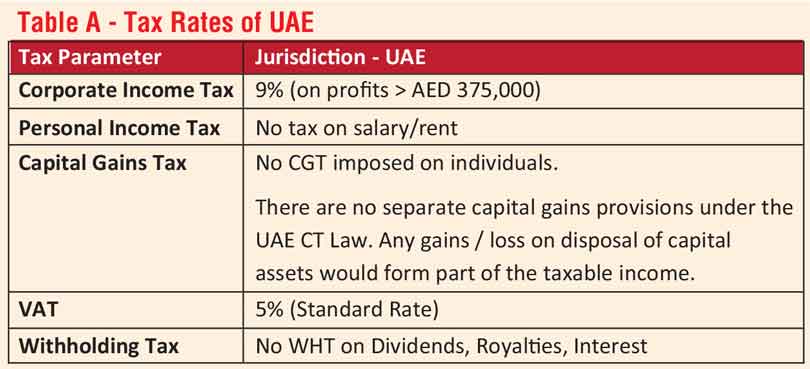

On 1 June 2023, the UAE implemented a federal corporate tax of 9% on taxable profits exceeding AED 375,000, approximately $ 102, 000

This threshold was specifically designed to protect the SME sector and domestic entrepreneurship while capturing revenue from larger commercial entities. For entities operating within Free Zones, a 0% rate continues to apply to “Qualifying Income,” ensuring that the UAE remains a premier destination for multinational corporations (MNCs) seeking to optimise their global tax footprint.

B) The elimination of personal and indirect tax burdens

A key factor in the UAE’s ability to park funds is the total absence of personal income tax, inheritance tax, and capital gains tax on individual investments. This fiscal neutrality for individuals ensures that high-net-worth individuals and global professionals view the jurisdiction not just as a workplace, but as a long-term wealth preservation hub. Sri Lanka, in contrast, has struggled with “brain drain” as professionals in medicine, IT, and academia perceive the high domestic tax burden as disproportionate to the public services provided. Adopting a framework that mirrors the fiscal clarity found in established global hubs, specifically through targeted employment income tax concessions within the Colombo Port City, serves as a strategic imperative for the retention of local talent and the attraction of high-tier international expertise.

C) The institutional mechanism of fund parking and capital mobility

The term “parking funds” in the context of the UAE refers to the strategic accumulation of capital in local banks and financial institutions due to the ease of repatriation, the lack of currency controls, and the high degree of regulatory certainty. The UAE’s financial ecosystem is built to ensure that once capital enters the country, it remains mobile and liquid.

D) Repatriation ease and regulatory frameworks

A defining feature of a global financial hub is the free movement of capital, and the UAE achieves this by allowing profits, dividends, and invested capital to be repatriated without foreign exchange controls, while relying on risk-based banking supervision and AML monitoring rather than monetary restrictions. For Sri Lanka to replicate this model, it must reduce longstanding concerns over foreign exchange scarcity and create a framework that gives investors confidence in capital mobility. In this regard, the Colombo Port City can function as a pilot jurisdiction in which capital is brought in from abroad and allowed to move out freely.

E) The role of offshore and Special Economic Zones

The Dubai International Financial Centre (DIFC) and the Abu Dhabi Global Market (ADGM) provide independent legal jurisdictions based on Common Law, which are exempt from UAE federal civil and commercial laws. This “jurisdiction within a jurisdiction” creates a safe harbor for international banking, asset protection, and offshore trusts. Sri Lanka is directly replicating this through the Colombo Port City Economic Commission (CPCEC), which serves as a “Single Window” facilitator for investors, providing regulatory certainty that is separate from the mainland’s administrative bureaucracy.

II) Maintaining dollar liquidity: The Central Bank of UAE monetary Sstrategy

A) The mechanics of the AED-USD Peg

The UAE Dirham (AED) has been pegged to the US dollar at 3.6725 for a significant period.7 To maintain this, the Central Bank of UAE ensures that the monetary base is fully backed by foreign currency reserves. As of 2026, the UAE’s foreign exchange reserves exceed AED 1 trillion ($ 270 billion), with a monetary base cover ratio of 119%. This high cover ratio provides absolute confidence that Dirhams can be converted to dollars at any time.

B) Advanced liquidity management facilities

The Central Bank of UAE manages surplus liquidity and safeguards the dirham’s dollar peg through an integrated set of advanced facilities: the Overnight Deposit Facility, launched in 2020, remunerates excess reserves at the Base Rate, anchored to the US Federal Reserve’s Interest on Reserve Balances, thereby setting a firm floor under overnight money market rates; Monetary Bills, introduced in 2021, absorb structural liquidity, support a dirham yield curve, and, together with the 2024 buy‑back program, allow liquidity to be withdrawn or injected as conditions require; standing credit windows such as the Marginal Lending Facility and the Shariah‑compliant Commodity Murabaha Facility provide overnight funding at a rate 50 basis points above the Base Rate, forming a symmetric interest rate corridor; and contingent facilities, including intraday and stress‑period liquidity lines backed by M‑Bills collateral, ensure continuous access to central bank reserves. Collectively, this floor‑based liquidity framework keeps UAE interest rates closely aligned with US dollar rates, reinforcing peg credibility while providing a stable monetary environment for international banking and trade finance.

III) Reinvestment of funds and the strategic shift to assets and infrastructure

The UAE has moved beyond passively parking capital, transforming its sovereign wealth funds and banks from portfolio custodians into active system builders that shape entire industries. This shift is evident in 2024, when 61% of sovereign capital was allocated to infrastructure and real estate, marking the first time in a decade that hard assets outweighed equities, and reflecting a deliberate “resilience through construction” strategy focused on building the foundations of future growth. Through large‑scale investments in renewable energy, semiconductors, aerospace, and digital infrastructure, the UAE is prioritising long‑term productive capacity over the passive acquisition of existing cash flows.

A) The AED 1 trillion sustainable finance goal

At COP28 in December 2023, the UAE banking sector, through the UAE Banks Federation, committed to mobilising over AED 1 trillion (about $ 270 billion) in sustainable finance by 2030, aligning the financial system with the country’s Net Zero 2050 objective and already building on more than AED 190 billion directed to green projects by six major banks. This pledge reflects a strategic pivot away from hydrocarbon dependence towards a diversified, knowledge‑based, and low‑carbon economy, with commercial banks financing renewable energy, green buildings, transition finance, and the decarbonisation of existing industries. In parallel, sovereign and government‑linked capital is being deployed into strategic sectors such as agri‑tech to strengthen food security and artificial intelligence, which the UAE increasingly treats as national infrastructure. Together, these coordinated streams of private and public investment illustrate how the UAE is using sustainable finance not only to drive green growth, but also to build technological sovereignty, economic resilience, and long‑term diversification.

IV) Sri Lanka’s application of the UAE blueprint

A) Category-Based Incentives Under the Port City Framework

The Colombo Port City (Guidelines on the Grant of Exemptions or Incentives to Businesses of Strategic Importance) Regulations, No. 1 of 2025, which replaced the expired 2023 Regulations, established a structured, tiered system for Primary and Secondary Businesses of Strategic Importance (BSI). Primary BSIs are land-lease developers who must meet minimum investment and employment thresholds:

Corporate Income Tax relief begins only after the Project Implementation Period, while during implementation Primary BSIs enjoy broad exemptions from customs duties, PAL, and selected other levies. Secondary BSIs operating in Port City receive a reduced 7.5% Corporate Income Tax rate for four years from the start of commercial operations, alongside exemptions from foreign exchange controls and certain labor laws. Once these time‑bound incentives lapse, all entities transition to the standard Inland Revenue Act framework, with the 2025 Regulations making all incentives uniform, non‑negotiable, and non‑transferable.

B) The 2026 CPCEC Act amendment: Fiscal discipline and regulatory tightening

The Colombo Port City Economic Commission (Amendment) Act of 2026 represents a decisive shift from concession‑granting principle towards a tighter fiscal discipline and regulatory accountability, responding to post‑crisis fiscal commitments and parliamentary scrutiny. It replaces open‑ended employment income tax exemptions with a transitional framework, granting employees of pre‑amendment entities a time‑limited exemption until 31 January 2029, while denying exemptions to later entrants, and imposes stricter, time‑bound, and periodically reviewed incentive requirements for Businesses of Strategic Importance, supported by Ministry of Finance analysis and public tax‑expenditure reporting. The Amendment also closes key regulatory gaps by subjecting foreign exchange transactions to the Foreign Exchange Act, placing offshore banking under Central Bank of Sri Lanka supervision, restricting offshore licenses to foreign‑incorporated entities, and empowering regulators to enforce corrective action or revocation for non‑compliance. Collectively, these reforms preserve Port City’s investment appeal while ensuring incentives are transparent, reviewable, and compatible with Sri Lanka’s broader objective of attracting capital without undermining fiscal control.

C) Comparative analysis of investment and fiscal structures

1) Performance-based incentives and evaluation

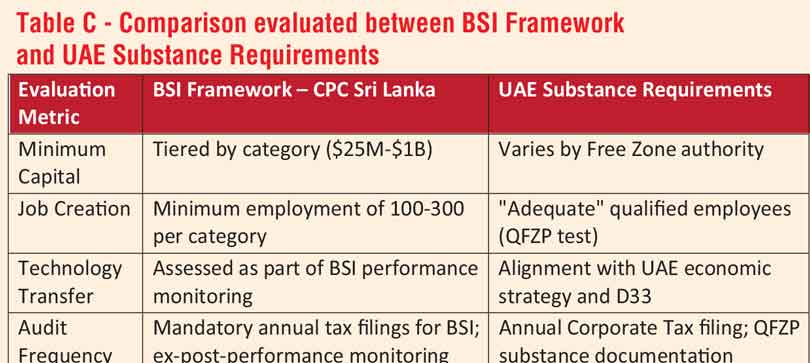

The 2026 Amendment to the CPCEC Act introduces a more disciplined, performance‑based incentive regime by requiring all incentives for Businesses of Strategic Importance to be justified by Ministry of Finance technical analysis, reviewed every five years, and subject to suspension or withdrawal for underperformance or non‑compliance. This mirrors the UAE’s substance‑driven approach, where tax benefits in Free Zones are conditional on demonstrable economic activity, such as maintaining adequate staff, expenditure, and core income‑generating functions within the zone, now embedded directly into the Corporate Tax framework through Qualifying Free Zone Person requirements. By replacing the historically ad hoc granting of concessions with a statutory, reviewable process, the new model enhances legal certainty for investors while ensuring that incentives remain contingent on real economic contribution and aligned with the state’s fiscal interests.

2) Reinvestment in human capital and the Golden Visa analogy

The UAE has successfully linked capital attraction with residency through its Golden Visa program, which grants long-term residency to investors, entrepreneurs, scientists, specialists in priority fields, and outstanding students. This ensures that the capital parked in the country is accompanied by the talent needed to deploy it productively. Sri Lanka is attempting a similar strategy through the Port City framework, where the Commission holds authority over immigration matters within the zone and can facilitate residency for employees and residents. The ambition is to create a city that attracts global talent rather than merely global capital.

3) Technical liquidity operations

For a jurisdiction to ensure that dollars are always available, it must have a central bank capable of managing structural excess liquidity. In the UAE, this arises from current account surpluses driven by hydrocarbon exports. The CBUAE manages this through a floor system, a method of setting up the price of money that has become the standard operational framework for pegged regimes with structural liquidity surpluses.

4) The floor system and the base rate

The UAE’s floor system works by paying banks a Base Rate on excess reserves held at the central bank’s Overnight Deposit Facility, which, given the system’s structural liquidity surplus, anchors overnight interbank rates firmly to that Base Rate and prevents volatility; because the Base Rate is linked to the US Federal Reserve’s Interest on Reserve Balances, it also underpins the credibility of the dirham’s dollar peg. For Sri Lanka’s Port City to operate as a truly dollarised zone, a comparable dollar-denominated reserve facility would be required, ensuring banks can meet USD withdrawals without recourse to LKR conversion and thereby preserving confidence in the working currency. The 2026 Amendment, by explicitly placing offshore banking licensees under CBSL’s supervisory framework for capital, liquidity, risk management, and disclosure in line with Basel and FSB standards, represents an important step toward building the institutional and monetary infrastructure needed to support such a system.

5) The role of M-Bills in financial depth

The UAE’s issuance of M-Bills does more than absorb excess liquidity; it provides the infrastructure for the domestic issuance of securities. By creating a Dirham-denominated yield curve through regular auctions of zero-coupon instruments at maturities ranging from 28 to 308 days, the central bank allows private corporations to issue their own bonds and sukuk with a clear benchmark for pricing. Sri Lanka lacks a deep corporate bond market. By adopting the UAE’s M-Bill model for the Port City, Sri Lanka could enable BSIs to raise capital in US dollars through a structured yield curve, further integrating parked funds into productive investment rather than leaving them idle in deposits.

D) Strategic reinvestment: High-return sectors and ambition

The UAE’s reinvestment model is defined by strategic co-investment, or Coalition Capital, in which sovereign funds partner with global private and institutional investors to build high-return sectors such as AI infrastructure, semiconductors, data centers, and power systems. Vehicles such as MGX, backed by Mubadala and G42, show how the UAE is using large-scale capital deployment not only to capture future growth but also to build what it describes as technology sovereignty through control over critical digital and industrial supply chains. For Sri Lanka, the relevance of this model lies in using the Colombo Port City’s highest investment tier to attract similarly ambitious long-duration projects.

E) Sri Lanka’s reinvestment strategy

Sri Lanka’s most credible reinvestment strategy lies in port-linked logistics, export-oriented services, and industrial upgrading, using the Port of Colombo’s position on major East–West shipping routes and Colombo Port City’s offshore, foreign-currency platform to channel capital into productive export capacity. Rather than pursuing broad energy ambitions, a more realistic direction is port-based decarbonisation, logistics efficiency, and green maritime services, which aligns with the Port of Colombo’s stated vision and wider goals of trade facilitation and sustainable logistics. The broader policy lesson is that reinvestment should be built on stable rules, carefully chosen sectors, and measurable productivity gains, since uncertainty weakens FDI and public debt crowds out investment; accordingly, Sri Lanka should focus on transparent screening and performance-based incentives that convert incoming capital into output, exports, and jobs.

Concluding points

The strategic realignment of Sri Lanka’s economic architecture, modelled after the proven fiscal and monetary strategies of global hubs like the UAE, represents more than a recovery effort; it is a fundamental shift toward institutional stability and global capital integration. By leveraging the Colombo Port City as such a jurisdiction, Sri Lanka can actively dismantle the historical barriers of currency volatility and regulatory ambiguity that once catalysed capital flight. The transition from the opaque incentive structures of the past to the rules-based governance codified in the 2025 Regulations and 2026 Amendment ensures that the nation can attract high-tier international expertise and foreign direct investment (FDI) without sacrificing long-term fiscal control. Ultimately, the success of this blueprint hinges on the delicate interplay between clarity and liquidity. As the UAE has demonstrated, providing investors with a predictable tax environment and unfettered capital mobility naturally builds the monetary base required to maintain a stable, working-currency environment. Further, it will depend on continued alignment with international standards, including taxation standards such as BEPS Pillar Two, which imposes a global minimum effective tax rate of 15%, and on the ability to maintain the diplomatic neutrality that makes Sri Lanka attractive.

(The author is an Assistant Manager - Tax Advisory at Bakertilly UAE, holding a LL.B (Honours) degree from University of London. With prior Sri Lankan taxation experience at EY and Bakertilly in Sri Lanka, and later as a UK Tax Consultant, Sheron brings cross jurisdictional expertise in Corporate, VAT, and International Taxation. Her legal experience includes collaborations with various Barristers and Solicitors in England for legal research and practice. Beyond professional accomplishments, Sheron has co-authored a research publication on AI and Corporate Governance for the 19th IRCMF 2024 Conference organised by the Faculty of Management and Finance, University of Colombo)

References:

CBUAE | How the Monetary System Works, accessed April 15, 2026, https://centralbank.ae/en/our-operations/monetary-policy-and-domestic-markets/how-the-monetary-system-works/

Middle East & South Asia (MESA) Tax Guide - KPMG agentic corporate services, accessed April 15, 2026, https://assets.kpmg.com/content/dam/kpmgsites/qa/pdf/2022/08/mesa-tax-guide.pdf

Sri Lanka Can Move to a More Balanced Fiscal Policy, Says World Bank Public Finance Review, accessed April 15, 2026, https://www.worldbank.org/en/news/press-release/2025/09/09/sri-lanka-can-move-to-a-more-balanced-fiscal-policy-says-world-bank-public-finance-review

Sri Lanka: Amended tax incentives and exemptions (Colombo Port City), accessed April 15, 2026, https://kpmg.com/us/en/taxnewsflash/news/2026/01/tnf-sri-lanka-amended-tax-incentives-and-exemptions-colombo-port-city.html

Sri Lanka Port City Regulations 2025 – Tax & Investment Rules, accessed April 15, 2026, https://www.desaram.com/sri-lanka-port-city-regulations-2025-tax-investment-rules/