Friday Jul 03, 2026

Friday Jul 03, 2026

Wednesday, 1 July 2026 00:23 - - {{hitsCtrl.values.hits}}

I generally support greater market liberalisation and a more competitive economy. However, unrestricted imports of non-essential and luxury goods cannot be viewed solely through the lens of free-market theory, particularly in a country such as Sri Lanka that has a long history of balance-of-payments crises, chronic foreign exchange shortages, and recurring currency depreciation.

I generally support greater market liberalisation and a more competitive economy. However, unrestricted imports of non-essential and luxury goods cannot be viewed solely through the lens of free-market theory, particularly in a country such as Sri Lanka that has a long history of balance-of-payments crises, chronic foreign exchange shortages, and recurring currency depreciation.

Sri Lanka’s economic experience repeatedly demonstrates that periods of unrestricted imports of non-essential goods—especially motor vehicles and other high-value consumer products—place enormous pressure on foreign exchange reserves and contribute to currency instability. Maintaining adequate foreign exchange reserves is not merely a technical policy objective. It is essential for financing fuel, medicines, food, industrial inputs, and capital equipment, while preserving economic stability and protecting living standards.

The debate on import liberalisation often overlooks a critical question: who ultimately bears the cost when foreign exchange shortages lead to currency depreciation? The answer is clear. It is not the wealthy.

Luxury imports are largely driven by a relatively small segment of high-income consumers whose purchasing power remains largely insulated from economic shocks. Yet when the rupee depreciates, the burden falls overwhelmingly on ordinary citizens whose incomes fail to keep pace with rising prices.

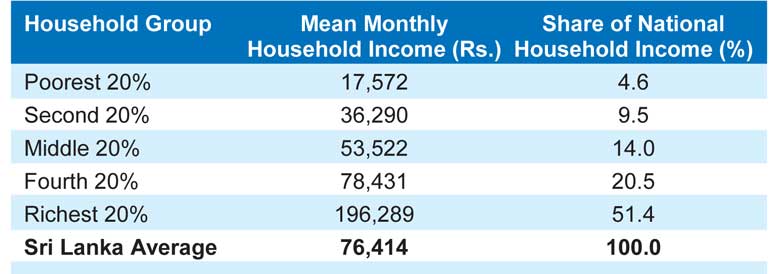

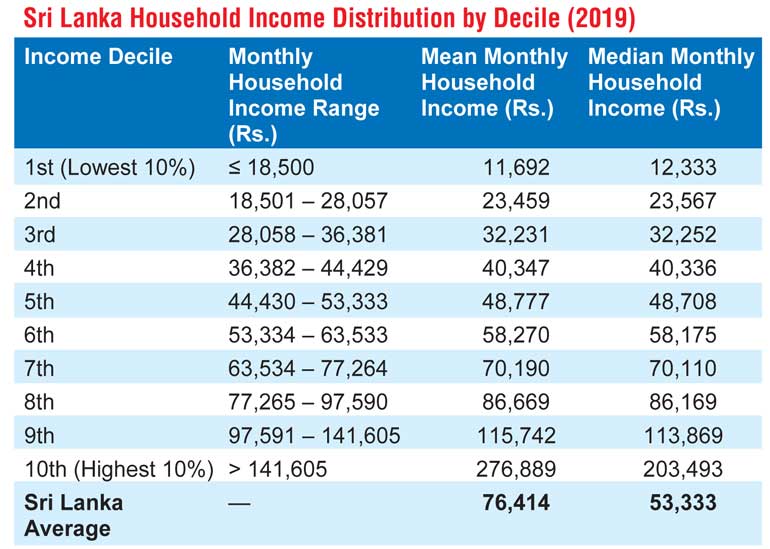

According to the latest nationally representative Household Income and Expenditure Survey (HIES) conducted by the Department of Census and Statistics, approximately three-quarters of Sri Lankan households earn less than Rs. 70,000 per month. These households neither drive excessive borrowing nor account for the bulk of luxury imports. Nevertheless, they bear the heaviest burden when currency depreciation erodes purchasing power and increases the cost of living.

The distribution of income in Sri Lanka further highlights this reality. The richest 20% of households receive more than half of all household income, while the poorest 20% receive less than 5%. This stark inequality means that the benefits of unrestricted imports accrue disproportionately to a relatively small affluent minority, while the costs of exchange- rate instability are borne by the broader population.

This reality becomes even more significant when one considers the magnitude of the rupee’s depreciation. At the end of 2019, the exchange rate stood at approximately Rs. 178 per US dollar. Today it is around Rs. 335 per Dollar—a depreciation of nearly 88%. During this period, wages for most workers have not increased by a comparable amount. In many cases, real incomes have fallen substantially following the economic crisis of 2022–2023.

Consequently, policies that contribute to further exchange-rate pressure cannot be assessed solely in terms of consumer choice or market efficiency. They must also be evaluated in terms of their impact on living standards, income distribution, and social welfare.

IMF policy prescriptions

This is where current IMF policy prescriptions warrant closer scrutiny.

Import liberalisation may be appropriate in economies with strong external balances, deep foreign exchange markets, and diversified export sectors. Sri Lanka, however, possesses none of these characteristics. Applying a standard liberalisation framework without adequately accounting for the country’s structural foreign exchange constraints risks producing outcomes that are economically and socially damaging.

Citizens have every right to question policies that advocate unrestricted imports while paying insufficient attention to the consequences of currency depreciation.

A more balanced and pragmatic approach would involve establishing annual foreign exchange allocations for non-essential and luxury imports. These allocations could be progressively increased as export earnings, tourism receipts, remittances, and foreign direct investment expand. Such a framework would provide greater predictability for businesses while safeguarding external stability.

Vehicle imports offer a useful illustration. A controlled annual allocation of approximately $1.2 billion would allow a gradual reopening of the market while preserving foreign exchange reserves. By contrast, import volumes approaching $2.6 billion annually could rapidly recreate the balance-of-payments pressures that contributed to previous crises.

Recent developments suggest that policymakers themselves may recognise these risks. The Government’s decision to impose a 50% surcharge on vehicle imports reportedly until August indicates concern about import demand and foreign exchange outflows. If such safeguards are removed without alternative measures in place, renewed pressure on the exchange rate could quickly emerge.

Managing import demand cannot rely exclusively on monetary tightening through higher interest rates, stricter credit conditions, and increased reserve requirements. Such measures suppress investment across the entire economy, including sectors that generate employment, exports, and long-term growth. Moreover, a considerable share of purchasing power remains concentrated among wealthier households that often do not depend heavily on bank credit to finance consumption.

This is precisely the type of issue that Sri Lanka’s policymakers should actively negotiate with the IMF. The objective should be to ensure that scarce foreign exchange is prioritised for productive investment, export expansion, technological upgrading, industrial development, and essential imports rather than disproportionately financing luxury consumption.

The argument that currency depreciation improves competitiveness must also be examined more critically.

In theory, a weaker currency can make exports more competitive. In practice, much of Sri Lanka’s export sector remains concentrated in lower-value-added industries where workers already struggle to meet basic living expenses. While depreciation may improve export competitiveness in nominal terms, it simultaneously increases the cost of imported food, fuel, transport, medicine, and other necessities.

The result is that workers effectively subsidise export competitiveness through a decline in their own living standards.

Economic competitiveness

This raises a fundamental question: should economic competitiveness be built on productivity and innovation, or on reducing the real incomes of workers?

Sustainable competitiveness cannot be achieved through currency depreciation alone. It requires investment in productive capacity, technology, skills, innovation, logistics, and infrastructure.

This is why the Government must play a central role in providing the strategic investments necessary to support long-term economic transformation. Investments in education, research and development, vocational training, transport networks, energy security, and industrial infrastructure are essential to attract private-sector investment into higher-value industries capable of generating quality, high-paying employment.

Unfortunately, Sri Lanka continues to lag behind many of its regional peers, including India, Bangladesh, Vietnam, and China, in developing the industrial capabilities and human capital required to compete in higher-value sectors of the global economy.

It is increasingly evident that strict adherence to IMF-prescribed fiscal targets and austerity measures has constrained many of these critical public investments. While macroeconomic stability is important, stability alone does not generate prosperity. If pursued without an accompanying development strategy, austerity risks suppressing economic transformation, limiting job creation, and perpetuating low productivity and poverty.

Currency depreciation by itself does not automatically attract productive investment. On the contrary, when household purchasing power declines, domestic demand weakens, reducing incentives for businesses to expand production or invest in new capacity. Under such conditions, economic growth becomes increasingly fragile and dependent on consumption rather than productivity gains.

The central policy challenge therefore is not whether imports should be liberalised, but how liberalisation can be balanced with external stability and long-term development objectives.

A carefully managed foreign exchange allocation framework for luxury imports is far more consistent with Sri Lanka’s economic realities than an unrestricted approach that risks repeating the mistakes of the past.

More importantly, Sri Lanka requires a people-centred development strategy focused on expanding productive capacity rather than merely increasing consumption. Such a strategy must prioritise rising real incomes for working families while directing national resources toward sectors that strengthen the country’s long-term economic potential.

This requires targeted investment in infrastructure, education, research and development, logistics, transport, energy security, modern agriculture, and export-oriented manufacturing. It requires an industrial policy that promotes technology transfer, entrepreneurship, value addition, and international competitiveness.

Over time, these investments would generate productive employment, broaden the export base, strengthen government revenues, and create the fiscal space necessary to build a more effective and sustainable social protection system.

Ultimately, the success of economic policy should not be judged by the extent of market liberalisation or compliance with external policy prescriptions. It should be judged by whether it creates productive employment, raises living standards, strengthens economic resilience, and improves the well-being of the majority of citizens.

Current policy trajectory

Economic policy must serve people first. Regrettably, the current policy trajectory appears to be moving in the opposite direction. By prioritising import liberalisation without adequately addressing structural foreign exchange constraints, Sri Lanka risks once again drifting towards a balance-of-payments crisis. Under such circumstances, the principal adjustment mechanism available to restore external equilibrium would almost certainly be further currency depreciation.

The burden of that adjustment would fall overwhelmingly on ordinary citizens.

A weaker rupee would further erode purchasing power, increase the cost of essential goods and services, and diminish already strained household incomes. For millions of Sri Lankans, this would mean a further decline in living standards and economic security.

Sri Lanka cannot build lasting prosperity through a recurring cycle of foreign exchange crises, currency depreciation, and declining real incomes. Sustainable development requires a deliberate strategy that expands productive capacity, strengthens exports, enhances technological capability, and raises the living standards of working people.

The objective is not permanent protectionism or indefinite administrative control of trade. Rather, it is a sequenced and pragmatic liberalisation strategy that expands in line with the country’s capacity to generate foreign exchange through exports, tourism, remittances, and productive investment.

This approach broadly reflects the development paths followed by countries such as China and Vietnam during their formative years of industrialisation, where market liberalisation was implemented gradually and strategically alongside the development of domestic productive capacity and export competitiveness.

Sri Lanka must learn from these experiences. The choice is not between liberalisation and protectionism. The real choice is between an economic strategy that serves a narrow consumer elite and one that advances the prosperity and economic security of the majority.

That is the debate Sri Lanka should be having.

(The author is Former Research and Development Director at Ansell Ltd., He is an inventor with six patents in latex-based product innovations. He is also a writer and commentator on macroeconomics, geopolitics, and global affairs, with a particular focus on political economy, industrial development, and international strategic issues. He could be reached via email [email protected])