Saturday Apr 11, 2026

Saturday Apr 11, 2026

Friday, 10 April 2026 00:00 - - {{hitsCtrl.values.hits}}

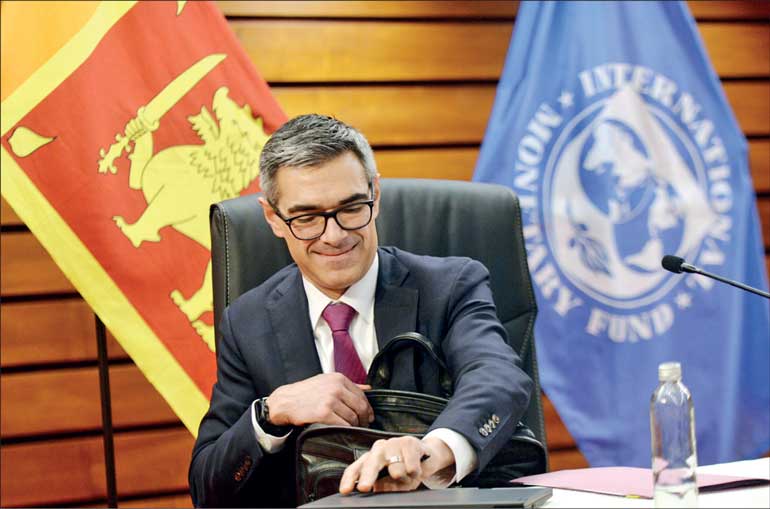

Satisfied so far? IMF Mission Chief for Sri Lanka Evan Papageorgiou captured with a smile at the conclusion of the media briefing yesterday

in Colombo – Pic by Pradeep Pathirana

By Nisthar Cassim

The International Monetary Fund (IMF) yesterday reiterated that it remains a steadfast partner and committed to helping Sri Lanka turn recovery into lasting prosperity for all.

This assurance comes as Sri Lanka nears the completion of its four-year $ 3 billion program of Extended Fund Facility (EFF) mid-next year with the country making impressive progress in stabilising its economy despite facing major challenges.

Given the global volatility and possible external and internal shocks in the future, the IMF is stressing that Sri Lanka should boost financial buffers and press ahead with reforms that strengthen economic resilience.

“Sri Lanka is emerging from its worst economic crisis in decades and has made notable strides in regaining stability – though we also stress that the economy remains fragile and continued reforms are needed to cement and build on these hard-won achievements,” the IMF mission team lead Evan Papageorgiou told the Daily FT in an exclusive interview following the conclusion of the 15-day staff visit yesterday.

“Sri Lanka is emerging from its worst economic crisis in decades and has made notable strides in regaining stability – though we also stress that the economy remains fragile and continued reforms are needed to cement and build on these hard-won achievements,” the IMF mission team lead Evan Papageorgiou told the Daily FT in an exclusive interview following the conclusion of the 15-day staff visit yesterday.

IMF said yesterday its staff and the Sri Lankan authorities reached staff-level agreement on the combined Fifth and Sixth Reviews under the EFF arrangement. Upon completion of the IMF Executive Board review, Sri Lanka would have access to about $ 700 million, bringing the total IMF financial support disbursed under EFF arrangement to $ 2.4 billion.

Here are excerpts of the interview with Papageorgiou in which he recaps the progress made by Sri Lanka so far and challenges ahead and how the country can overcome the latter.

Q: What is the IMF's broader assessment of Sri Lanka's progress under the four-year EFF program so far, especially given the external and domestic challenges the country has faced? What are the key achievements so far?

A: Sri Lanka has made impressive progress in stabilising its economy under the IMF-supported program, despite facing major challenges at home, including from external shocks. After the severe 2022 crisis – when the economy contracted sharply and inflation peaked at almost 70% y/y– Sri Lanka is now experiencing a robust recovery.

Economic growth has bounced back to about 5% in 2025, a remarkable turnaround from the deep recession of 2022. Inflation has been tamed to low single digits (around 2% as of early 2026), indicating that consumer prices have largely stabilised after last decade’s extreme surge. On the fiscal front, Government revenues have roughly doubled as a share of GDP – from about 7% in 2022 to over 15% in 2025 – thanks to substantial tax reforms and improved compliance. The country’s public debt is being restructured and put on a sustainable path, with the debt restructuring process now nearly complete.

Meanwhile, the Central Bank of Sri Lanka has rebuilt foreign currency reserves from near-zero levels during the crisis to $7.3 billion at end-February 2026, significantly boosting Sri Lanka’s financial buffers against external shocks. All these achievements – renewed growth, restored price stability, stronger public finances, and higher reserves – reflect the fruits of the authorities’ commitment to difficult but necessary reforms under the program.

These gains have been achieved despite significant headwinds, including the devastating Cyclone Ditwah in late 2025, which caused extensive damage and forced a deferment in the program’s review schedule, and the ongoing Middle East conflict, which raised Sri Lanka’s import costs and is threatening its tourism and export earnings and remittances. Sri Lanka’s program performance was strong until the latest EFF assessment, with most targets met even amid these shocks.

In short, Sri Lanka is emerging from its worst economic crisis in decades and has made notable strides in regaining stability – though we also stress that the economy remains fragile and continued reforms are needed to cement and build on these hard-won achievements.

Q: How can Sri Lanka further build its buffers and strengthen resilience to handle external shocks, especially since these shocks seem to be happening in quick succession?

Q: How can Sri Lanka further build its buffers and strengthen resilience to handle external shocks, especially since these shocks seem to be happening in quick succession?

A: The key is to both boost the country’s financial buffers and press ahead with reforms that strengthen economic resilience. In practical terms, this means:

Continue rebuilding fiscal and external buffers: Sri Lanka should maintain prudent policies that increase its financial safeguards, such as further accumulating foreign exchange reserves and sustaining a healthy Budget position (for example, by keeping the Budget in surplus or reducing public debt). Having larger reserves and more fiscal space provides the Government a cushion to absorb unexpected shocks without derailing the economy.

Keep policies flexible in the face of shocks: Resilience also comes from policy flexibility. This includes allowing the exchange rate to adjust when external pressures rise – a flexible currency can act as a shock absorber for the economy. Likewise, monetary and fiscal policies should be nimble; for instance, if global oil prices surge or export demand falls, the CBSL and Government need to respond promptly, for example through interest rate adjustments or temporary support measures that are well targeted and carefully costed. Importantly, targeted assistance for vulnerable groups (like subsidies or cash transfers for low-income households) can help cushion the impact of higher living costs or job losses during a crisis.

Strengthen economic fundamentals: Over the longer term, the best defense against rapid-fire external shocks is a stronger, more diversified economy. That’s why continuing the structural reforms is vital. Sri Lanka should keep working on measures that boost its long-term resilience: for example, making it easier for businesses to invest and create jobs (thus diversifying the economy and export base), solidifying the financial sector’s stability, improving public finances (so the Government has resources to respond in a downturn), and expanding social safety nets to protect the most vulnerable when crises hit. By focusing on these areas, Sri Lanka can build up its “rainy day” funds and resilience, ensuring that each new shock – whether a global conflict, a commodity price spike, or a natural disaster – has a more limited impact on people’s livelihoods and the overall economy.

Q: There is a growing call to lower Sri Lanka’s inflation target from the current 5%. Does the IMF believe a 5% inflation target remains appropriate for the medium term, or should Sri Lanka consider aiming for a lower figure?

A: The current 5% inflation target has anchored expectations and guided policy during Sri Lanka’s stabilisation phase. The CBSL will review the target under the Central Bank Act (every 3 years).We believe it is premature to say whether 5% is “too high” or should be changed – the decision will depend on data and analysis of what target best supports Sri Lanka’s long-term stability and growth.

It is important to note that setting an inflation target is a complex decision with many factors at play. Policymakers need to consider the country’s economic structure and development level, inflation expectations, as well as the recent inflation history and the need for relative price adjustments after a high-inflation period. Often, emerging-market economies initially set slightly higher inflation targets (around 4–5%) because their economies are growing and changing rapidly – some inflation can help relative prices shift as needed. If conditions improve further and the monetary policy framework matures, there could eventually be grounds for a lower target. But any adjustment to the inflation target should be done only after careful study and should be well-communicated.

It is important to note that setting an inflation target is a complex decision with many factors at play. Policymakers need to consider the country’s economic structure and development level, inflation expectations, as well as the recent inflation history and the need for relative price adjustments after a high-inflation period. Often, emerging-market economies initially set slightly higher inflation targets (around 4–5%) because their economies are growing and changing rapidly – some inflation can help relative prices shift as needed. If conditions improve further and the monetary policy framework matures, there could eventually be grounds for a lower target. But any adjustment to the inflation target should be done only after careful study and should be well-communicated.

Q: In what areas would the IMF like to see improved commitment and execution from the Sri Lankan Government?

A: The authorities have already implemented many difficult reforms with commendable outcomes, including restoring macroeconomic stability, passing a new Public Financial Management (PFM) Act, and advancing governance reforms. Going forward, we encourage continued momentum in a few key areas. These include full implementation of the PFM law and improved transparency in public procurement; better planning and oversight of public investment and PPPs; and strong follow-through on state-owned enterprise (SOE) reforms, including implementation of the new SOE Act and continued publication of audited financials.

We also encourage continued improvements to the Aswesuma social safety net, including completing the recertification process and strengthening the empowerment program. On the fiscal side, while revenue performance has improved, further revenue-based consolidation is needed—particularly through better tax administration and new, efficient sources like a property tax. Broader structural reforms to support investment and job creation should also continue.

Q: With the EFF program scheduled to conclude by mid-2027, does the IMF believe Sri Lanka will be able to manage on its own after the program ends?

A: Sri Lanka’s IMF-supported program aims to help the country get back on its feet – by restoring macroeconomic stability, addressing underlying problems, and laying the groundwork for sustainable growth. Sri Lanka is on track to achieve the objectives under the EFF, with good progress towards raising revenue, mitigating fiscal risks, restoring debt sustainability, ensuring price stability, rebuilding foreign reserves, safeguarding financial stability, and strengthening governance. But success will depend on the authorities’ commitment to maintain sound policies and stay the course on reforms, even after the EFF arrangement ends.

A: Sri Lanka’s IMF-supported program aims to help the country get back on its feet – by restoring macroeconomic stability, addressing underlying problems, and laying the groundwork for sustainable growth. Sri Lanka is on track to achieve the objectives under the EFF, with good progress towards raising revenue, mitigating fiscal risks, restoring debt sustainability, ensuring price stability, rebuilding foreign reserves, safeguarding financial stability, and strengthening governance. But success will depend on the authorities’ commitment to maintain sound policies and stay the course on reforms, even after the EFF arrangement ends.

For example, Sri Lanka’s Government will need to keep strengthening its public finances – the revenue gains achieved under the program should be preserved and further enhanced, through better tax administration and compliance, and perhaps new measures like the property tax we discussed.

Prudent Budget management must continue, to ensure that debt stays on a sustainable downward path and that there are resources for development and social spending, including for education and health. The CBSL will need to continue refraining from monetary financing, maintaining low and stable inflation, and ensuring adequate reserves, which will help preserve investor confidence and exchange rate stability.

Importantly, the end of the EFF in 2027 does not mean the end of IMF engagement with Sri Lanka. We will continue our regular Article IV consultations, which serve as routine check-ups of the economy, and our provision of capacity development. The IMF remains a steadfast partner and is committed to helping Sri Lanka turn recovery into lasting prosperity for all.