Wednesday Jun 17, 2026

Wednesday Jun 17, 2026

Saturday, 2 November 2019 00:07 - - {{hitsCtrl.values.hits}}

Premier blue chip John Keells Holdings (JKH) has faced a challenging second quarter with its overall performance showing mixed results with some sectors improving and others lagging. JKH reported a 3% growth in Group revenue during the second quarter of the year of Rs. 33.7 billion. First half Group revenue was up 4% to Rs. 65.4 billion.

Premier blue chip John Keells Holdings (JKH) has faced a challenging second quarter with its overall performance showing mixed results with some sectors improving and others lagging. JKH reported a 3% growth in Group revenue during the second quarter of the year of Rs. 33.7 billion. First half Group revenue was up 4% to Rs. 65.4 billion.

Results from operating activities was up 14% to Rs. 1.2 billion in the second quarter and down 5% to Rs. 1.69 billion in the first half.

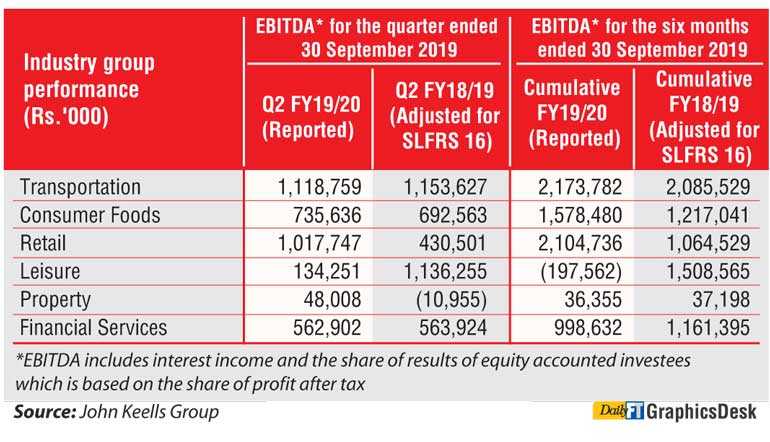

Group EBITDA at Rs. 4.80 billion in the 2Q was a dip of 25% over FY2019. The cumulative EBITDA for the first half of FY20 was Rs. 8.50 billion, down by 21% from a year earlier.

Second quarter Group pre-tax profit was down 45% to Rs. 2.59 billion and for the first half, it was lower by 48% to Rs. 3.95 billion. JKH's bottom line was down 55% to Rs. 2.29 billion in the second quarter and by an equal percentage to Rs. 3.28 billion in the first half.

JKH said the profit attributable to equity holders in the second quarter to 2018/19 includes a recognition of a deferred tax asset at Union Assurance PLC. Profits for the quarter were mainly impacted by the Easter Sunday impacts on the Sri Lankan Leisure businesses and the decline in finance income and exchange gains at the holding company.

JKH Chairman Krishan Balendra said the performance of the Consumer Foods, Retail, Leisure, and Property industry groups continued its growth momentum from the first quarter despite the disruptions post the Easter Sunday terror attacks.

“The Group’s year-on-year performance for the quarter was impacted by the downturn in the Group’s Sri Lankan Leisure business which continued to be significantly impacted post the Easter Sunday terror attacks, lower finance income as a result of the deployment of cash in new investments, and lower exchange gains recorded at the Holding Company on its foreign currency denominated cash holdings,” he added.

JKH said the Retail industry group recorded a robust revenue growth of 21% which was driven by a strong performance in the Supermarkets business, also driven by a notable contribution from new outlets and strong growth in customer footfall. Retail recorded an EBITDA of Rs. 1.02 billion compared with the adjusted EBITDA of Rs. 431 million in the same period last year. Two new outlets were opened during the quarter, increasing the total store count to 100 as at 30 September.

The Group’s Sri Lankan Leisure business continued to be significantly impacted by the Easter Sunday terror attacks in April. The quarter performance was also impacted by the partial closure of Cinnamon Dhonveli Maldives for refurbishment and start-up costs related to Cinnamon Hakuraa Huraa Maldives and the Group’s new resort, Cinnamon Velifushi Maldives. EBITDA for the second quarter of 2019/20 was Rs. 134 million, compared to the Rs. 1.14 billion (adjusted) recorded in 2018/19 Q2. However, the Group is encouraged that the forward bookings for the Sri Lankan hotels have witnessed an upward trend and expect occupancy in the peak season to be in line with the previous year, albeit at a moderately lower room rate.

The City Hotels sector and the Sri Lankan Resorts segment recorded a decline in both occupancies and average room rates. However, despite the challenging operating environment, the City Hotels sector maintained its fair share of available rooms in the five-star category in the quarter under review.

During the quarter under review, the Group added a fourth resort property to its Maldivian hotel portfolio, Cinnamon Velifushi Maldives. The hotel was handed over to Cinnamon on an operating lease, in line with the Group’s asset light investment strategy, and will commence operations in October. Cinnamon Velifushi Maldives, consisting of 90 rooms, is positioned as a five-star deluxe resort. Initial bookings for the resort are above expectations. With the completion of the partial refurbishment of Cinnamon Dhonveli Maldives in November, and the completion of the reconstruction of Cinnamon Hakuraa Huraa Maldives in December, the Group will have the full complement of all its four Maldivian hotels operational from the fourth quarter of this financial year, with a new and premium product offering. The newly re-constructed Cinnamon Bentota Beach hotel in the Sri Lankan resorts segment will also commence operations in December, as planned. This flagship Cinnamon property will be positioned as the epitome of luxury in the Group’s leisure portfolio.

In the Property Industry Group, the quarter under review marked the first tranche of revenue recognition for the ‘Tri-Zen’ residential development project. The revenue recognition of the project will ramp up over the next few quarters as the project progresses. Whilst sales for the previous quarter were impacted by the Easter Sunday terror attacks in April, the sales momentum is now improving, where interest has reverted to pre-incident levels with both the months of August and September recording encouraging sales.

The installation of external facades, mechanical and electrical services and the interior works are nearing completion for the Cinnamon Life Residential and Office Towers, for handover from April 2020 onwards. The full completion of the project is on track for March 2021.

The Financial Services industry group recorded a marginal drop in EBITDA (2019/20 Q1: Rs.563 million versus 2018/19 Q1: Rs.564 million), while Other, including the Information Technology and Plantation Services sectors, recorded an EBITDA of Rs. 1.18 billion in the second quarter of 2019/20 over the adjusted EBITDA for the second quarter of the previous financial year (2018/19 Q1: Rs. 2.44 billion), as a result of the decline in finance income as a result of the deployment of cash in new investments and lower exchange gains recorded at the holding company on its foreign currency denominated cash holdings.