Saturday Jul 04, 2026

Saturday Jul 04, 2026

Tuesday, 28 April 2026 01:49 - - {{hitsCtrl.values.hits}}

Sri Lanka’s improved Treasury liquidity masks a weaker fiscal position, with cash balances swinging from a deficit of Rs. 832 billion in 2022 to a surplus exceeding Rs. 1.2 trillion by August 2025, driven by Rs. 1.78 trillion in excess borrowing that has raised the interest burden on unused funds, Verité Research warned.

“Sri Lanka’s treasury cash balance has improved sharply. At first glance, that looks like a striking fiscal turnaround. It suggests the Government has rebuilt financial space. But that reading is incomplete,” the think tank said in brief yesterday.

“This rise in cash balances did not come from revenue left over after the Government met its expenses. It came from borrowing more than was needed at the time and holding the excess as cash in the Treasury,” it noted.

Verite said:

A large cash balance can create the impression that the Government has money to spare – or has come into a substantially better financial position. Is that what has happened?

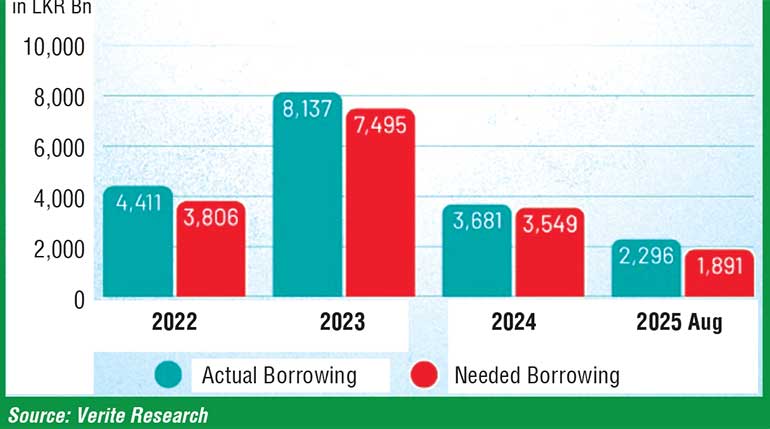

The Finance Ministry’s cash flow statements show that, from 2022 to August 2025, the Government borrowed more than it needed to cover its Budget shortfall and debt repayments. The extra borrowing was then accumulated as cash in the Treasury, instead of being used to reduce debt (see table).

The pattern is clearest in 2023, when the cash buffer grew the most.

That year, the Government’s total financing need was Rs. 7,495 billion. This included Rs. 5,331 billion in debt repayments and a Budget deficit of Rs. 2,164 billion. Yet, the Government borrowed Rs. 8,137 billion. In effect, it borrowed around Rs. 642 billion more than it needed at the time. That excess was added to the Treasury cash balance.

The same pattern can be seen across the full 2022 to 2025 period.

Between 2022 and August 2025, the Treasury borrowed in total Rs. 1,783 billion more than it needed for its financing requirements. This extra borrowing was used to build up the cash buffer, which was negative Rs. 832 billion at the start of 2022 and increased, by these means, to a positive Rs. 1,205 billion by August 2025.

A simple example helps. Imagine a person that takes a loan and leaves the money in their bank account. Their cash balance goes up; but so does their level of debt. In fact they go up equally, leaving the net asset position same. The same dynamics and logic applies to the Treasury cash balance and the Government.

Is the Government better off?

A rising cash buffer can be easily misinterpreted as a sign of a stronger fiscal position. However, with a debt financed cash buffer, this is not the case.

Yes, in terms of liquidity, the Government is in a better position. The cash buffer enables the Treasury to meet urgent financing needs without coming to the market to borrow; and more importantly, creates space to reduce borrowing at the regular Bond auctions, when the asking yields of lenders seems too high.

Now, in terms of interest cost, the Government is in a worse position. The Government is effectively paying to keep borrowed money that it isn’t using. The cash balance can earn an interest, but almost surely a lower rate than what was paid to borrow it – making a net loss for every day that it holds the cash balance.

Therefore, while a positive cash balance can ease short-term liquidity pressures, it does not put the government in a better fiscal position.

In fact, when the cash balance is in excess of liquidity requirements, the fiscal outcome is negative – because it increases the debt and interest burden. So, while having a cash buffer is positive – it allows the government to push back on auction bids that ask for yields that are too high; having a lot of it is negative – the Government ends up carrying an additional interest burden for holding cash that it does not immediately need, the think tank said.

Sri Lanka’s fiscal position strengthened sharply in January 2026, with the primary surplus rising 86.7% YoY to Rs. 222.82 billion and the overall Budget deficit narrowing 96.8% to Rs. 3.81 billion, indicating a near-balanced position. Revenue growth remained strong, up 35.3% on higher tax collections, while expenditure was largely contained, rising just 1.4%.

The improved performance, despite a Rs. 500 billion post-Ditwah spending allocation, reflects continued fiscal consolidation and has created space for a Rs. 100 billion short-term relief package to cushion the impact of global energy shocks.