Thursday Feb 19, 2026

Thursday Feb 19, 2026

Tuesday, 12 March 2019 00:59 - - {{hitsCtrl.values.hits}}

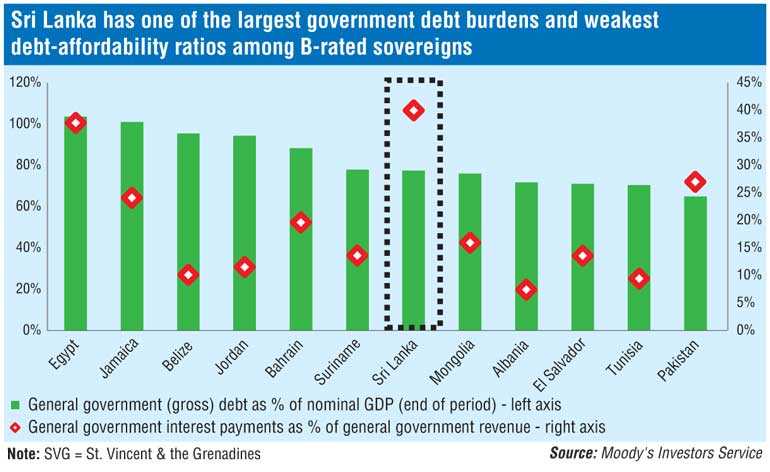

Sri Lanka’s fiscal consolidation plans will be challenging without greater policy effectiveness and faster GDP growth, rating agency Moody’s warned yesterday, projecting that debt would remain at about 83% of GDP in 2020 with interest payments absorbing about 40% of Government revenue.

On 5 March, Sri Lanka (B2 stable) presented its Budget for 2019, highlighting the Government’s credit-positive commitment to revenue-led fiscal consolidation and debt reduction, Moody’s said in a statement. After a fiscal deficit of 5.3% of GDP in 2018, the Government aims to reduce it to 4.4% of GDP in 2019 and to 3.5% in 2020, in line with its International Monetary Fund (IMF) program targets.

However, achieving its deficit and debt targets will be challenging without a significant increase in fiscal policy effectiveness and faster GDP growth.

Sri Lanka’s ambitious fiscal consolidation targets – when the country has not had a fiscal deficit below 5.0% since at least 1990 – will rely on effective tax collection and administration and increases in some taxes. The Government has lifted revenue to 14% of GDP in 2018 from as low as 11.6% in 2014 by raising the value-added tax rate in October 2016 and implementing the Inland Revenue Act (IRA) in April 2018.

The Budget anticipates that this trend will continue, projecting revenue increasing to 15.8% of GDP in 2019 and 16.8% in 2020, which equates to annual growth of about 22% in 2019 and 16% in 2020 and exceeds what the government has achieved, on average, in recent years

Although a full-year of IRA implementation will support revenue growth, newly introduced exemptions will limit some of the gains. Taxes on cigarettes, liquor, international credit card transactions and gambling will rise, although the potential for lower consumer demand would reduce the revenue benefits. The Government aims to strengthen tax collection by establishing a Revenue Intelligence Unit at the Ministry of Finance.

“The Budget also anticipates non-tax revenue increasing in 2019 and 2020, but historically non-tax revenue has been volatile and its trajectory will be influenced by the sale of state assets and dividends from financially strained state-owned enterprises,” the report said.

Political risk can disrupt fiscal and economic policymaking, and restraining spending will be difficult ahead of the presidential election in 2019 and general election in 2020. Large recurrent spending commitments, which the government estimates will account for around 76% of all expenditures in 2019 amid civil servant wage increases, payments for pensioners and subsidies for agriculture, tend to be difficult to curb.

The Government expects real GDP growth to accelerate to 3.5% in 2019 and 4% in 2020, after a 17-year low of 3% in 2018. This is much lower than the 5.6% average annual real GDP growth that occurred in Sri Lanka over the 10 years to 2017.

“Slow real and nominal GDP growth will challenge the Budget’s revenue projections and hinder the government’s ability to pursue fiscal consolidation at the pace it projects. Underperforming revenue or disappointing economic growth would delay or limit more durable strengthening of the fiscal position. Such a scenario may cause the Government to curb spending to meet its fiscal targets, but that would hurt GDP growth and lower revenue collection,” Moody’s said.

“We expect a slower pace of fiscal consolidation, projecting fiscal deficits to gradually narrow below 5% of GDP in 2019-20. As a result, we expect that Government debt will remain around 83% of GDP in 2020, higher than the Government’s projection and higher than many B-rated sovereigns. Interest payments will continue to absorb around 37%-40% of Sri Lanka’s Government revenue in the next few years, one of the weakest debt-affordability ratios among B-rated sovereigns.”