Sunday Jun 14, 2026

Sunday Jun 14, 2026

Friday, 29 August 2025 03:38 - - {{hitsCtrl.values.hits}}

Several Sri Lankan banks have issued fresh warnings to customers about an increase in phishing scams targeting online banking users.

According to notices released this week, scammers are sending links through emails and text messages that direct users to fake websites designed to steal personal and financial information.

Authorities said the fraudulent sites often mimic official banking portals, using altered spellings or unusual characters to mislead customers. Users have been urged to avoid clicking on suspicious links and instead type official web addresses directly into their browsers.

Banks have also advised customers to double-check website URLs before entering sensitive details, such as login credentials, and to report any suspicious activity immediately.

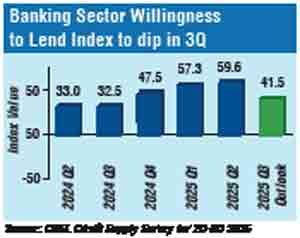

A new Central Bank of Sri Lanka (CBSL) report last week said the banking sector’s Willingness to Lend Index grew in the second quarter of 2025, continuing a nine-quarter upward trend to reach a five-quarter high. However, while the trend is expected to continue into the third quarter, the Index, or willingness to lend, shows a slight dip.

The Willingness to Lend Index reached 59.6 in Q2 2025, up from 57.3 in the previous quarter.

“This observed increase was led by prevailing economic and political stability, stable interest rates, improved liquidity positions in banks, and expectations regarding general economic activities,” the CBSL said in its Credit Supply Survey: Trends in Q2 and Outlook for Q3 2025. The survey covers Licenced Commercial Banks and Licenced Specialised Banks, and the Willingness to Lend Index is much like a business confidence index for banks.

During Q3 2025, the increasing trend is expected to continue due to favourable liquidity positions of banks, economic revival, and positive economic outlook, the banking regulator said.

However, the Index value shows a dip from 59.6 in Q2 2025 to 41.4 in Q3 2025, lower than the previous three quarters and Q4 2024’s Index value of 47.5.

The CBSL report said that during Q2 2025, the upward trend in demand for loans increased due to reduced interest rates, increased wages, vehicle imports, and improvements in business activities. Due to the expected further reduction in interest rates, increase in vehicle imports, and improved business confidence, the demand for loans is expected to further increase during Q3 2025, it said.

On non-performing loans (NPLs), the CBSL said the overall number of NPLs decreased during Q2 2025 as well. This could be attributed to a reduction in interest rates, improved cash flow generation, effective recovery and collection efforts, ongoing flexible payment options, and supportive economic conditions.

The CBSL noted: “The decline in NPLs is expected to continue in Q3 2025 as well, due to continuation of flexible payment options, expected further reduction of interest rates, and positive sentiments on economic outlook.”

The number of rejected loan applications decreased in Q2 2025 compared to the previous quarter, possibly due to quality proposals and improved economic conditions, the CBSL noted.

“Due to the expected economic recovery, improved cash flow generation, and better business conditions, loan application rejections are expected to further decline during Q3 2025,” it said.

In Q2, lending grew across retail, corporate, and Small and Medium Enterprise (SME) borrowers. Tourism, stronger exports, and domestic manufacturing supported this growth, while lending to State-owned enterprises slowed due to tighter evaluations.

Loan demand was lifted by lower rates, wage growth, vehicle imports, and improved business activity. The CBSL expects this momentum to continue into Q3, with rising consumer confidence and a favourable economic outlook.

NPLs fell across corporates, SMEs, and State-owned enterprises in Q2, though retail defaults rose slightly due to higher living costs. The CBSL expects overall NPLs to decline further in the coming quarter, with stronger collections, better cash flows, and lower rates.

Loan application rejections eased in Q2, supported by stronger borrower profiles and better business conditions. They are expected to fall further in Q3 as economic stability improves credit quality.

Credit data underline that private borrowing is driving the recovery, not State demand. In June, private sector credit rose by Rs. 221.5 billion, the highest monthly increase of 2025, lifting the outstanding stock above Rs. 8.85 trillion.

By contrast, Government borrowing from banks was Rs. 98 billion, while credit to public corporations fell by Rs. 1.3 billion. The pattern points to a recovery steered by private sector demand, rather than the State drawing down funds.

The CBSL added liquidity through $ 1 billion in foreign exchange purchases in the first half of 2025, boosting reserves to $ 6 billion by June. With liquidity in surplus, banks had space to expand lending without being crowded out by State borrowing.

In the past, excess liquidity was often blamed on CBSL monetary expansion to finance Government deficits, driving inflation and import demand, and leading to Balance of Payments pressures and International Monetary Fund (IMF) bailouts, as it artificially props up the currency or controls interest rates. This time, it stems from foreign currency purchases to build reserves, marking a structural shift in the drivers of credit expansion.

Private investors also see the shift as significant.

Addressing the Invest Sri Lanka Forum in Singapore earlier this month, Lynear Wealth Managing Director Dr. Naveen Gunawardane said the Government’s fiscal reforms and the Public Finance Management Act are creating a different macroeconomic environment than in past recoveries.

He noted that, unlike before, “the Central Bank is no longer printing money to finance deficits,” which has kept interest rates stable and supported investor confidence.

“Provided that we stick to the reforms that were done, provided that the Government sticks to fiscal discipline, provided that we keep the CBSL independent, Sri Lanka is going to see a period of relatively stable interest rates and relatively stable exchange rates. We have not seen that in the past,” he said.

Still, lending to SMEs remains constrained. Despite Government-backed concessional loan pools and credit guarantees, utilisation has been low. Deputy Industries and Entrepreneurship Development Minister Chathuranga Abeysinghe told an SME forum earlier this month that only Rs. 458 million has been disbursed from a Rs. 6 billion concessional facility and Rs. 1 billion from a Rs. 15 billion guarantee program.

Officials have criticised banks for their reluctance to extend risk capital to smaller firms even as overall credit growth accelerates. The contrast highlights a gap: while the broader economy is being financed, SMEs remain at the margins of the recovery.