Saturday Jul 18, 2026

Saturday Jul 18, 2026

Monday, 25 May 2026 00:39 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

The Sri Lanka secondary Bond market last week experienced a predominantly bearish week, with yields rising through the first four trading sessions.

The Sri Lanka secondary Bond market last week experienced a predominantly bearish week, with yields rising through the first four trading sessions.

This came against the backdrop of prolonged geopolitical tensions in the Middle East and persistently elevated and volatile global crude oil prices, which weighed on investor sentiment. Concerns over the inflationary implications of elevated energy prices and broader macroeconomic risks prompted market participants to adopt a cautious and defensive stance. This mirrored the upward adjustment seen in global Bond yields which experienced a sell-off.

Selling pressure remained the dominant theme early in the week, driving yields higher for four consecutive sessions. However, intermittent buying interest emerged at elevated yield levels, helping to contain sharper upward movements in rates. Despite the risk-off sentiment, market turnover remained healthy throughout the week, supported largely by several block transactions and selective institutional demand.

However, sentiment improved on Friday, as renewed buying interest emerged at the higher yield levels, prompting a recovery in the secondary Bond market. The move was further supported by a sharp intraday appreciation of the Sri Lankan rupee, while global Bond yields also showed signs of recovery. However, despite the partial retracement on Friday, secondary market two-way quotes closed the week notably higher.

In terms of the Secondary Bond Market Trade Summary, the market was seen moving in an inverted U-pattern:

In the secondary bond market, the 01.08.26 maturity traded up from an intraweek low of 8.25% to a high of 8.68%. The 15.12.27 and 15.09.27 maturities changed hands at the rates of 9.20% and 9.16% respectively.

In the 2028 space, the 01.07.28 maturity saw a sharp upward move, trading from an intraweek low of 9.95% to a high of 10.55%, however recovered partially at the end of the week to trade back down at the rate of 10.25%. Similarly, the 15.02.28 and 15.03.28 maturities changed hands within the range of 10.00%–10.10% and the 01.05.28 maturities traded up the range of 10.40%–10.55%.

Moving into the 2029 segment, the 15.09.29 and 15.12.29 maturities were seen trading up from intraweek lows to highs of 10.05%–10.95%, before recovering to trade at the rate of 10.40%.

In the 2030 space, the 01.03.30, 15.05.30, and 01.07.30 maturities changed hands within the ranges of 10.30%–10.80%, 10.40%–10.80%, and 10.20%–10.45% respectively, before trading back down to trade at 10.40%.

The 01.06.33 maturity traded up from an intraweek to low of 11.05% to a high of 11.60%, before recovering to trade at 11.38%. The 15.06.34 maturity initially traded up from an intraweek low of 11.25% to 11.70%, before recovering to trade at 11.45% at the tail end of the week.

At the longer end, the 15.06.35 maturity traded within the range of 11.42%–11.50%, while the 15.08.36 maturity was seen changing hands between 11.35%–11.60%. The 01.07.37 maturity traded at the rate of 11.50%.

To recap the weekly Treasury Bill auction conducted last Wednesday, was undersubscribed, raising the only 48.03% or Rs 67.24 billion out of the Rs. 140 billion on offer at the first phase in competitive bidding. The bid to offer ratio stood at 1.66 times.

Rates were seen increasing reversing the decline observed the previous week. Accordingly, the weighted average yield rates on the 91-day tenor increased by five basis points to 8.18% and the 182-day tenor increased by two basis point to 8.25%. However, the 364-day tenor remained unchanged at 8.49%.

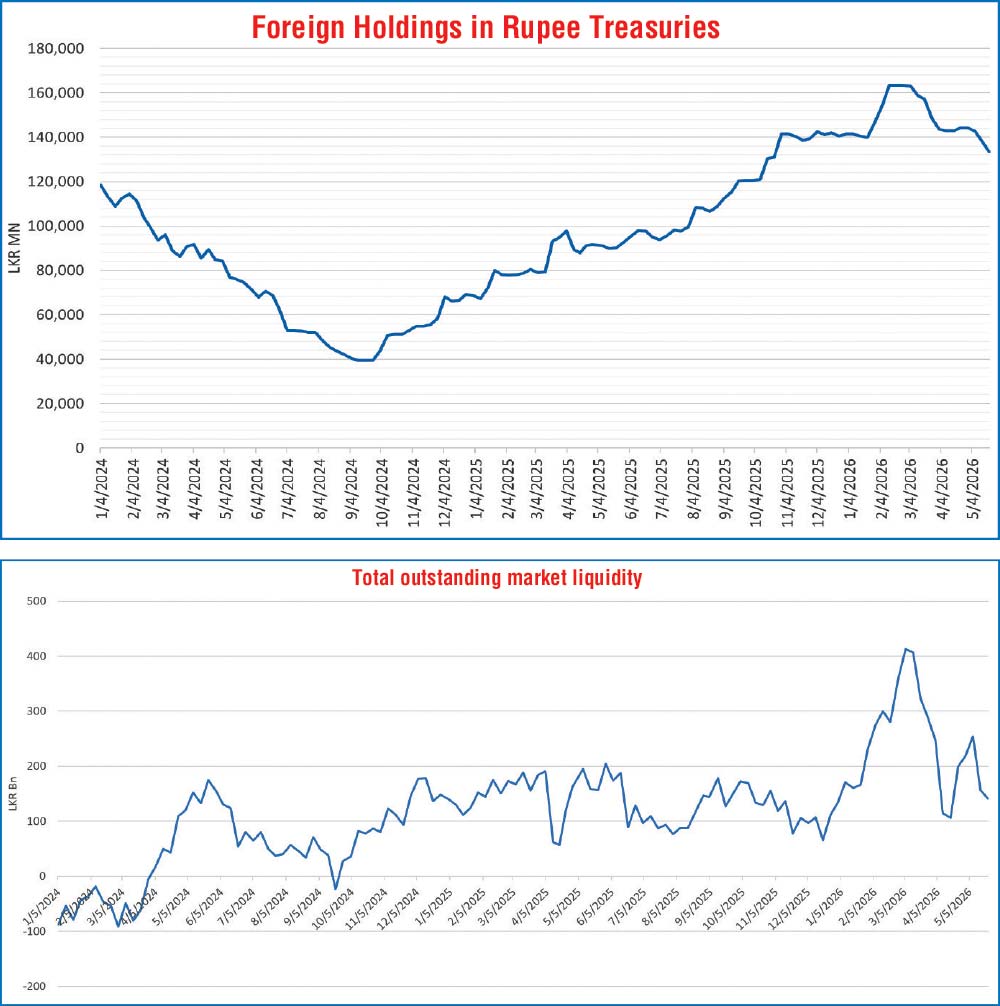

The foreign holdings of rupee-denominated Government securities dropped lower, recording a net outflow for the third consecutive week amounting to Rs. 4.58 billion. Accordingly, the total foreign holdings declined further to Rs. 133.43 billion during the week ended 21 May.

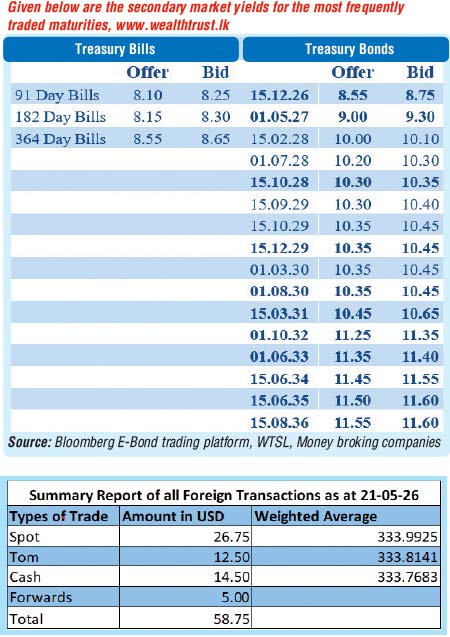

In money market, the total outstanding liquidity surplus in the money market was recorded at Rs. 141.27 billion against its previous weeks of Rs. 156.80 billion. The weighted average interest rates on Call Money and Repo stood at 7.92% and 7.97% respectively at the close of the week as compared to 7.79% and 7.85% respectively the previous week.

Forex market

In the Forex market, the USD/LKR rate on spot contracts was seen trading from an intraweek high of Rs.326.50 to a low of Rs.348.00, before recovering to trade at the rate of Rs.329.00.

The daily USD/LKR average traded volume for the first four trading days of the week stood at $ 50.13 million.

(References: Public Debt Management Office - Ministry of Finance, Central Bank of Sri Lanka, Bloomberg E-Bond Trading Platform, Money Broking Companies)