Saturday Jun 13, 2026

Saturday Jun 13, 2026

Thursday, 9 April 2026 00:08 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

The Secondary Bond Market saw yields initially decline sharply yesterday, as the announcement of the US-Iran Ceasefire sparked a relief rally. The news saw Brent crude futures plunge more than 15% toward $90 per barrel, as Iran agreed to conditionally reopen the Strait of Hormuz for two weeks, alleviating the current supply disruption pressures stemming from the key choke point.

The market factored in easing inflationary and foreign exchange pressures and rates began retracing downwards as the geopolitical outlook improved considerably.

Reinforcing this move was favourable developments on the domestic front, with a staff level approval imminently expected from the IMF EFF program and that Sri Lanka is on track to receive $ 700 million from combined fifth and sixth tranches by end-May.

This rally reflected the positive sentiment in the local stock market and global financial markets as well.

Activity and transaction volumes were seen at robust levels, but tapered off towards the end of the trading session following the release of the Treasury Bill auction results and as market participants adopted a wait and see approach ahead of the Treasury Bond auction due today. The emergence of profit taking pressure and the Bill auction outcome resulted in Bond yields surrendering some gains. As a result, secondary Bond market two-way quotes the day marginally lower.

Accordingly, during the rally earlier in the day the 15.02.28 maturity traded at the rate of 9.25%. The 01.07.28 maturity traded down the range of 9.55% to 9.50% and the 15.12.28 maturity at the rate of 9.65%. The 15.06.29 maturity traded down the range of 9.75%-9.70% and the 15.09.29 maturity down the range of 9.76%-9.71%. 15.10.29 maturity traded down range of 9.80% to 9.73% and the 15.12.29 maturity down the range of 9.90% to 9.80%. The 01.07.30 maturity traded down the range of 9.95%-9.87%.

However, on the back of profit taking pressure and following the release of the T Bill results the 01.03.30 maturity which had touched a low of 9.80% traded back up to 9.85%, the 01.10.32 maturity which touched a low of 9.58% traded back up to 9.67% and the 01.06.33 maturity which had traded at a low of 10.85% traded back up to a high of 10.98%.

The weekly Treasury Bill auction conducted yesterday extended its upward trajectory and saw weighted average yields increase across the board for the third consecutive week. Accordingly, the yield on the 91-day Bill rose by 15 basis points to 7.95%, the 182-day Bill increased by five basis points to 8.14%, while the 364-day Bill saw an uptick of four basis points to 8.45%.

The auction was fully subscribed and raised the entire offered amount of Rs. 30 billion at the first phase in competitive bidding. The bid-to-cover ratio stood at 1.99 times.

The Phase II subscription across all three tenors is now open until 3.00 pm of business day prior to settlement date (i.e., 09.04.2026) at the WAYRs determined for the said ISINs at the auction.

This comes ahead of the Treasury Bond auctions scheduled to be conducted today, 9 April. The round of auctions will have a total offered amount of Rs. 100.00 billion across three available maturities.

The auction will be comprised of: Rs. 30 billion from a 1 July 2030 maturity bearing a coupon rate of 9.75%; Rs. 40 billion from a 15 June 2034 maturity bearing a coupon rate of 10.75%; Rs. 30 billion from a 1 July 2037 maturity bearing a coupon rate of 10.75%. The settlement for which will be held on 15 April 2026.

For context, the previous round of Treasury Bond auctions conducted on the 12 March produced a positive outcome, registering weighted average rates below or in-line with prevailing secondary market levels at the time.

However, the auction was undersubscribed only raising Rs. 87.02 billion or 66.94% out of Rs. 130 billion on offer at the first and second phases — across three available maturities. The bids received to accepted amount ratio stood at 2.45 times.

Maturity-wise the results were as follows:

The shorter tenor 01.03.30 maturity was issued at a weighted average yield of 9.63%, however went undersubscribed at the 1st and 2nd phases.

The 15.06.34 maturity was issued at the weighted average yield of 10.70%. This tenor was also undersubscribed.

The longer tenor 15.08.36 maturity was fully subscribed at the 1st phase and issued at a weighted average yield of 10.80%.

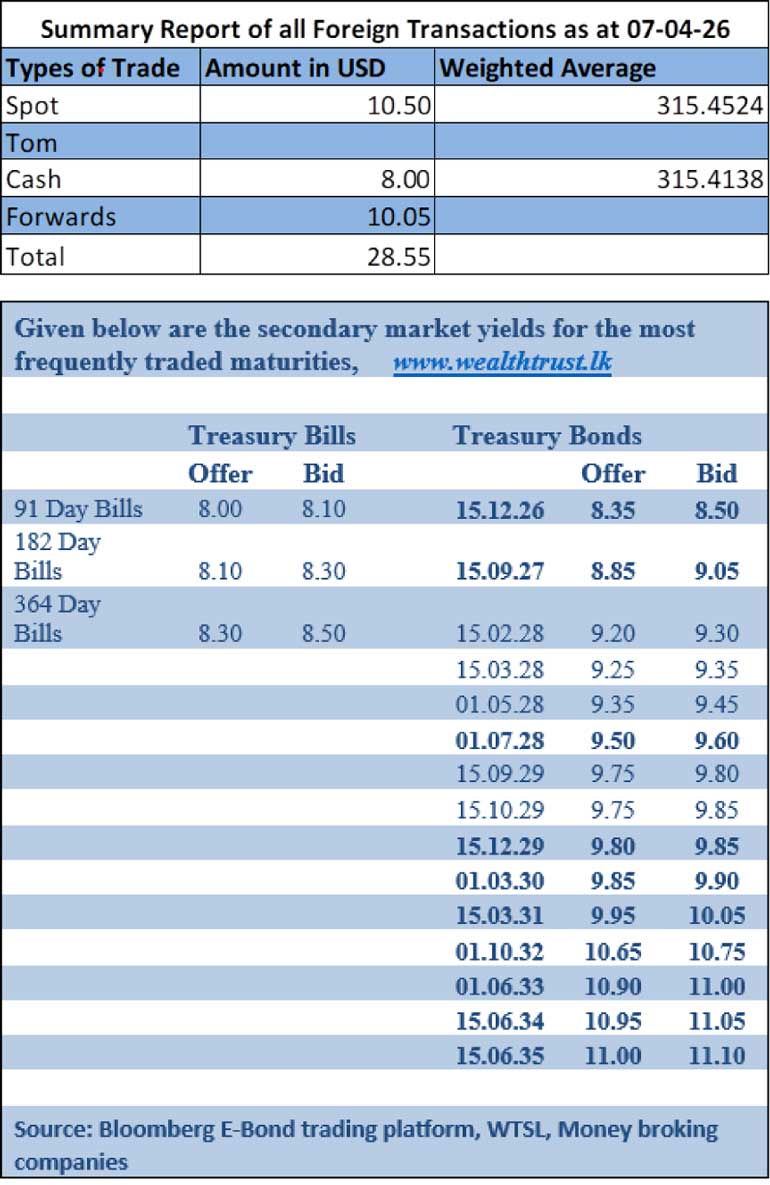

The total secondary market Treasury Bond/Bill transacted volume for 7 April was Rs. 8.17 billion.

In the money market, the net liquidity surplus in money market was recorded at Rs. 237.26 billion yesterday. The Domestic Operations Department (DOD) of the Central Bank of Sri Lanka was seen draining out an amount of Rs. 20 billion by way of overnight Repo auction at a weighted average rate of 7.48%.

Further an amount of Rs 231.76 billion was deposited at Central Bank’s SDFR (Standing Deposit Facility Rate) of 7.25% as against an amount of Rs 14.50 billion withdrawn from the Central Bank’s SLFR (Standing Facility Rate) of 8.25%.

The weighted average rates on overnight call money and Repo yesterday stood at 7.63% and 7.66% respectively.

Forex market

In the forex market, the Rupee strengthened with spot USD/LKR closing at Rs.315.30/315.40 against the previous day’s close of Rs.315.45/315.50.

The total USD/LKR traded volume for 7 April was $ 28.55 million.

(References: Public Debt Management Office - Ministry of Finance, Central Bank of Sri Lanka, Bloomberg E-Bond Trading Platform, Money Broking Companies)