Friday Jun 12, 2026

Friday Jun 12, 2026

Thursday, 11 June 2026 00:04 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

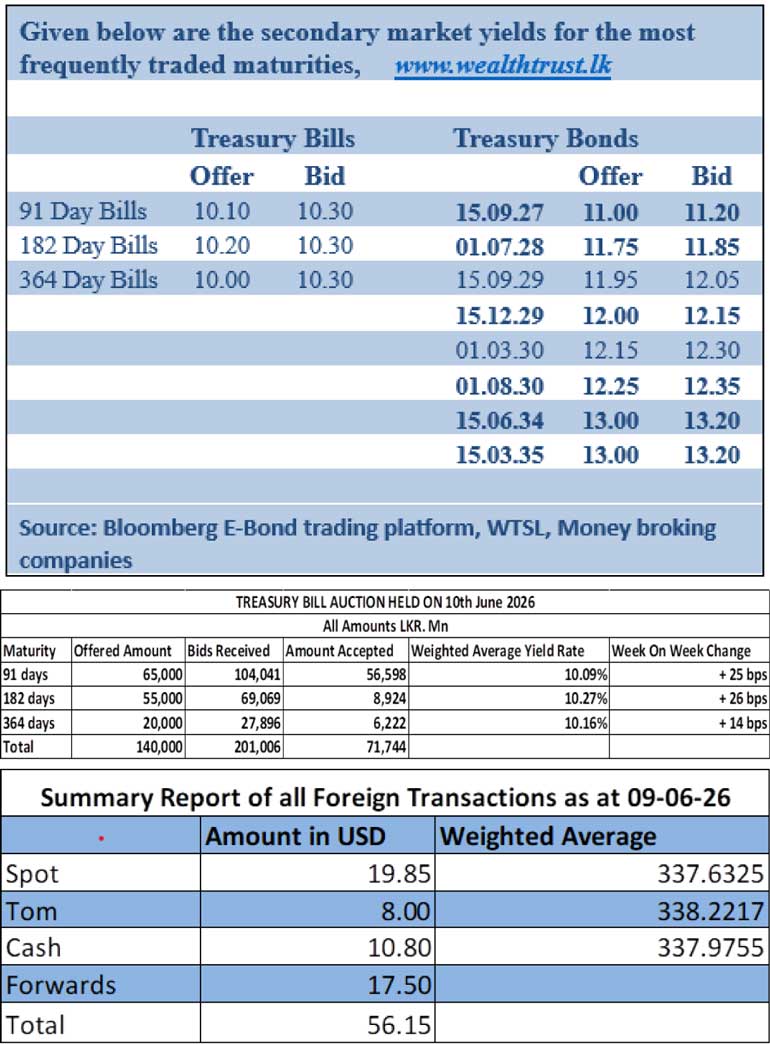

At the weekly Treasury Bill auction conducted yesterday, yields increased for the fourth consecutive week, reflecting the prevailing bearish sentiment. However, rates this week were seen increasing at a slower pace signalling a moderation in the upward movement.

Accordingly, the weighted average yield on the 91-day Treasury Bill rose by 25 basis points to 10.09%, while the 182-day and 364-day tenors increased by 26 basis points and 14 basis points to 10.27% and 10.16%, respectively. These yield levels represent the highest since late-September 2024. Interestingly, the rate on the six months increased above the 1-year rate.

Following the recent 100 basis point increase in the Monetary Policy Rate, cumulative increases in Treasury bill weighted average yields have now reached approximately 167–202 basis points across the three tenors, significantly exceeding the magnitude of the policy rate adjustment.

The auction raised only Rs. 71.744 billion in successful bids during the first phase of competitive bidding against an offered amount of Rs. 140 billion, representing a subscription rate of 51.25%. Total bids received amounted to 1.44 times the offered volume. Notably, the bulk of the accepted amount was raised from the shorter tenor 3 months while the other two tenors saw acceptance sharply below the respective offered amounts.

The Phase II subscription across all three maturities is now open until 3.00 pm of business day prior to settlement date (i.e., 11.06.2026) at the WAYRs determined for the said ISINs at the auction. Given below are the details of the auction.

The secondary Bond market yesterday saw rates hold broadly steady buoyed by the CBSL reducing the FX conversion time for exporters to 30 days to bolster the rupee and support the external sector balance as well as the constructive signal from the T-Bill auction. However, activity and transaction volumes remained at subdued levels amidst the prevailing uncertainty stemming from mixed-geopolitical signals from the Middle Eastern conflict, the volatile and still elevated crude oil prices. In addition, market participants were seen taking a wait-and-see approach ahead of the upcoming Treasury Bond auction.

The 01.08.26 maturity traded at the rate of 10%.The 15.09.29, 15.10.29 and 15.12.29 maturities traded at the rates of 12%,12.10% and 12.15% respectively. The 01.08.30 maturity traded at the rate of 12.25%.

This comes ahead of the Treasury Bond auctions due to be held Today the 11th of June. The round of auctions will have a total offered amount of Rs. 150 billion across three available maturities.

The auction will be comprised of:Rs. 70 billion

from a 15 May 2030 Maturity bearing a coupon rate of 11%; Rs. 60 billion from a 15 December 2032 Maturity bearing a coupon rate of 11.50%; Rs. 20 billion from a 1 July 2037 Maturity bearing a coupon rate of 10.75%; The settlement for which will be held on 15 June 2026.

For reference the previous round of Treasury Bond auctions saw the entire Rs. 240 billion on offer raised at the first phase in competitive bidding. The bids received to accepted amount ratio stood at 1.84 times; a strong response given the scale of the auction.

Maturity-wise the results were as follows: The shorter tenor 01.08.30 maturity was issued at a weighted average yield of 11.86%; the 15.01.33 maturity was issued at the weighted average yield of 12.32%; and the longer tenor 15.03.35 maturity was issued at the weighted average of 12.93%.

In the money market, the net liquidity surplus recorded at Rs. 57.38 billion yesterday. An amount of Rs. 82.97 billion was deposited at Central Bank’s SDFR (Standing Deposit Facility Rate) of 8.25% as against an amount of Rs. 25.59 billion withdrawn from the Central Bank’s SLFR (Standing Facility Rate) of 9.25%.

The weighted average rates on overnight call money and Repos were recorded at 9.19% and 9.23% respectively.

Forex market

The USD/LKR rate on spot contracts was seen closing at the rate of Rs. 332.25/333,appreciating from the previous day’s close of Rs. 337/337.75.

The total USD/LKR traded volume for 9 June was $ 56.15 million.

(References: Public Debt Management Office - Ministry of Finance, Central Bank of Sri Lanka, Bloomberg E-Bond Trading Platform, Money Broking Companies)