Sunday Aug 09, 2026

Sunday Aug 09, 2026

Thursday, 13 November 2025 00:10 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

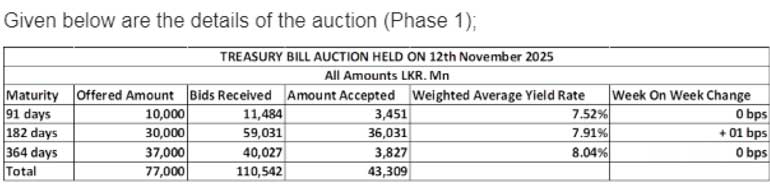

The weighted average rates at the weekly Treasury Bill auction conducted yesterday remained broadly steady, with the yields on the 91-day and the 364-day tenors remaining unchanged at 7.52% and 8.04% respectively. However, the 182-day tenor registered a marginal increase of 01 basis point to 7.91%. This marks the 17th week where T-Bill rates have stayed broadly anchored around prevailing levels.

However, the auction was undersubscribed, raising only 56.25% or Rs 43.31 billion out of the Rs 77.00 billion offered. This marks the second consecutive auction to undersubscribed. The bids received to offered amount ratio stood at 1.44 times.

The Phase II of subscription is now open across all three ISINs until 3.00 pm of business day prior to settlement date (i.e., 13.11.2025) at the WAYRs determined for the said ISINs at the auction. Given in the table are the details of the auction Phase 1.

Meanwhile, the secondary Bond market yesterday saw yields edge up marginally. Activity and transaction volumes were initially seen at healthy levels before tapering off to a virtual standstill as market participants adopted a wait-and-see stance ahead of the upcoming Treasury Bond Auction.

In terms of the Secondary Bond market trade summary, the 15.01.27 maturity was seen trading within the range of 8.15%-8.16%. The 15.02.28, 15.03.28 and 01.05.28 maturities were seen trading at the rates of 8.90%, 8.90%-8.95% and 8.93% respectively. The 15.06.29, 15.09.29, 15.10.29 and 15.12.29 maturities were seen trading at the rates of 9.35%, 9.45%, 9.45% and 9.45% respectively. The 15.05.30 and 01.07.30 maturities were seen 9.55% and 9.56% respectively. The 15.03.31 maturity was seen trading at the rates of 9.80%-9.82%.

The 15.12.32 maturity bucked the trend and rallied dropping from an intraday high of 10.25% to a low of 10.20%. The 01.11.33 maturity traded at 10.45% while the 15.09.34 maturity at 10.55%.

This comes ahead of the Treasury Bond auction, scheduled to be conducted today, 13 November. The round of auctions will have a total offered amount of Rs. 80 billion across three available maturities.

The auction will be comprised of: Rs. 35 billion from a 1 July 2030 maturity bearing a coupon rate of 09.75% and Rs. 45 billion from a 15 June 2035 Maturity bearing a coupon rate of 10.70%

The settlement for which will be held on 17 November 2025.

For context, the last Treasury Bond auctions conducted on the 13 October with a total offered amount of Rs. 181 billion across three available maturities, went undersubscribed. However, this was due to only the relatively shorter tenor maturity going undersubscribed.

The auctions raised Rs. 162.11 billion or 86.23% out of the total offered amount in successful bids across both phases. The total bids received exceeding the offered amount by 2.13 times.

Maturity-wise the results were as follows:

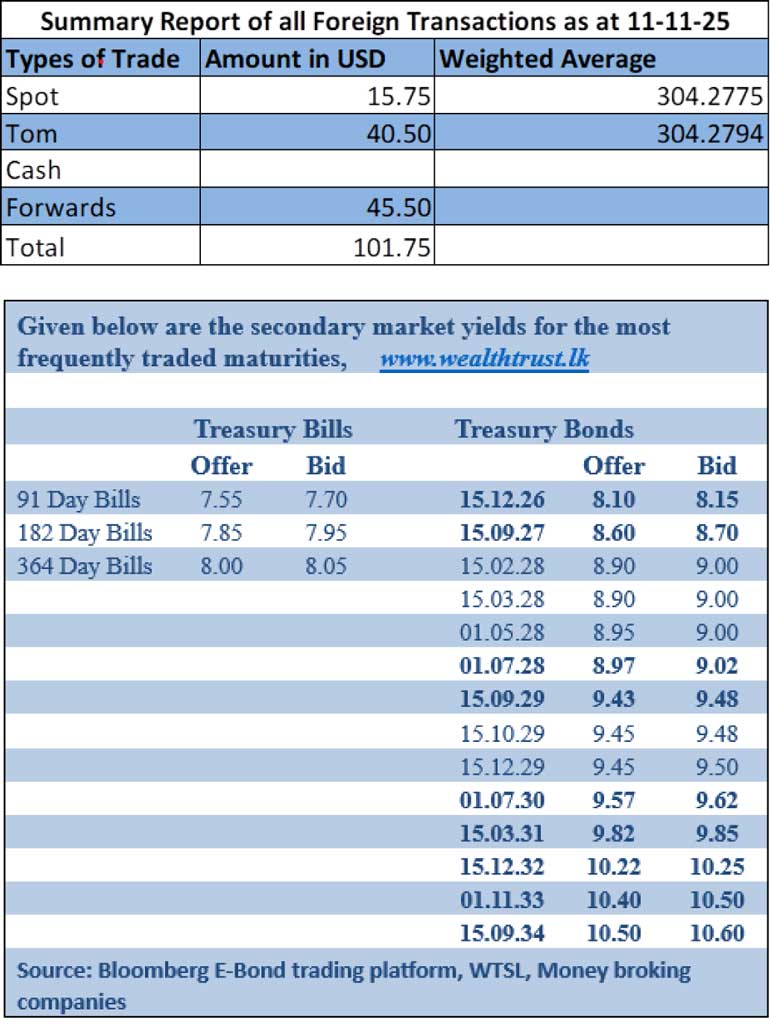

The total secondary market Treasury Bond/Bill transacted volume for 11 November was Rs. 8.03 billion.

In money markets, the weighted average rates on overnight call money and Repo stood at 7.93% and 7.96% respectively.

In money markets, the net liquidity surplus was recorded at Rs. 146.61 billion yesterday deposited at the Central Banks SDFR (Standing Deposit Facility Rate) of 7.25%.

Forex Market

In the Forex market, the USD/LKR rate on spot contracts to closed depreciating to 304.60/304.65 as against its previous day’s closing level of Rs. 304.20/304.35.

The total USD/LKR traded volume for 11 November 2025 was $ 101.75 million.

(References: Central Bank of Sri Lanka, Bloomberg E-Bond trading platform, Money broking companies)