Friday Aug 07, 2026

Friday Aug 07, 2026

Thursday, 18 June 2026 00:45 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

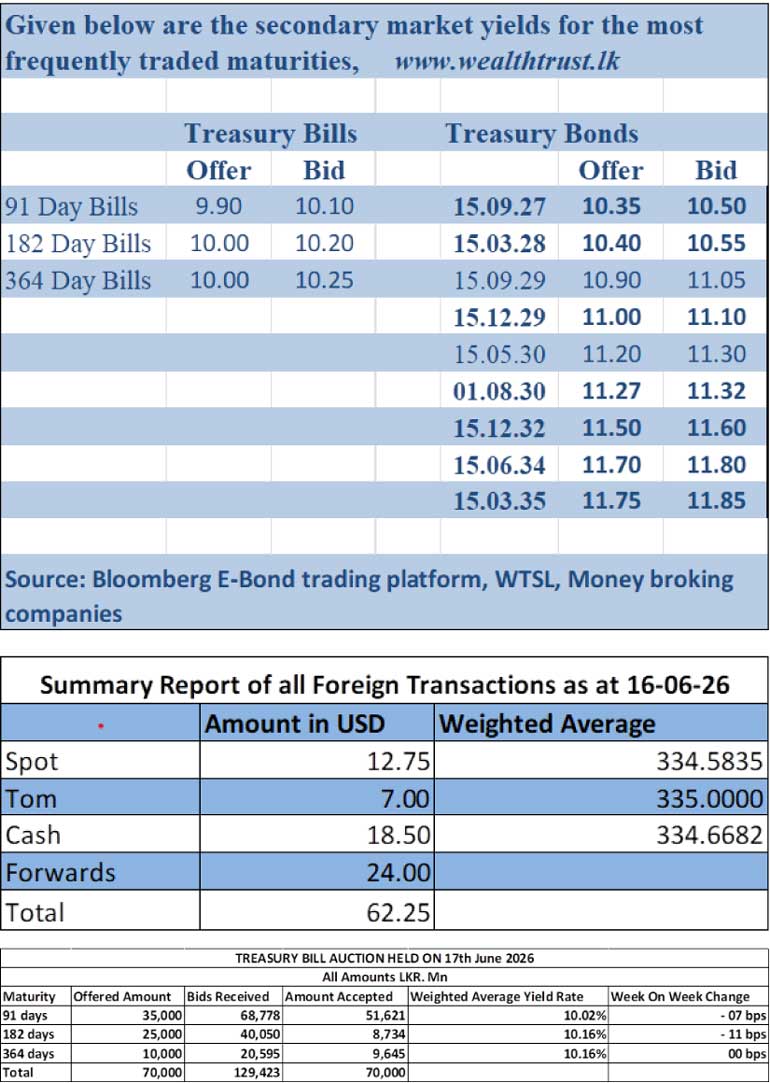

At the weekly Treasury Bill auction conducted yesterday, rates dropped for the first time in five weeks. This reflected the downward adjustment in secondary Bond market yields driven by enthusiasm around the US-Iran peace agreement and the corresponding drop in Brent Crude prices below $ 80/barrel- the lowest level in around 3 months.

The weighted average yield on the 91-day Treasury Bill decreased by 7 basis points to 10.02%, the 182-day Bill saw its rate drop by 11 basis points to 10.16%. However, the 364-day tenor remained unchanged at 10.16%. As such the inversion in the T-Bill yield curve was corrected.

The auction raised the entire Rs. 70 billion offered at the first phase in competitive bidding. Total bids received amounted to 1.85 times the offered volume. Notably, the bulk of the accepted amount was raised from the shorter tenor three months which raised more than its respective offered amount. The other two tenors saw acceptance sharply below their respective offered amounts.

The Phase II subscription only on the 182-day and 364-day tenors is now open until 3.00 pm of business day prior to settlement date (i.e., 18.06.2026) at the WAYRs determined for the said ISINs at the auction (see table for details of the auction).

The secondary Bond market yesterday saw rates decline as the market extended its rally. Aggressive buying interest was seen on the short-end and spilling over to the long-end driving yields lower on the back of elevated activity and transaction volumes. Despite some late-session profit-taking secondary market two-way quotes closed firmly lower.

The 01.05.28, 01.07.28 and 15.10.28 maturities traded lower at the rates of 10.74%-10.65%, 10.65% and 10.75%-10.70%. The 15.12.29 maturity saw its yield decline down the range of 11.12%-11.00%. The 01.03.30, 15.05.30 and 01.08.30 maturities traded at the rates of 11.30%-11.05%, 11.25% and 11.40%-11.20%. The 15.01.33 maturity traded down the range of 11.70%-11.50% and the 01.06.33 maturity traded 11.60%. The 15.06.34 maturity traded at the rate of 11.80%. The 15.03.35 maturity was taken down the range of 11.90% to 11.77% and the 15.08.36 saw a notable drop to trade at a low of 11.90%.

In the money market, the net liquidity surplus was recorded at Rs. 43.19 billion yesterday. An amount of Rs. 90.45 billion was deposited at Central Bank’s SDFR (Standing Deposit Facility Rate) of 8.25% as against an amount of Rs. 47.26 billion withdrawn from the Central Bank’s SLFR (Standing Facility Rate) of 9.25%.

The weighted average rates on overnight call money and Repos were recorded at 9.20% and 9.24% respectively.

Forex market

The USD/LKR rate on spot contracts was seen closing at the rate of Rs. 333.5/334.25, appreciating from the previous day’s close of LKR. 334.75/333.5.

The total USD/LKR traded volume for 16 June was $ 62.25 million.

(References: Public Debt Management Office - Ministry of Finance, Central Bank of Sri Lanka, Bloomberg E-Bond Trading Platform, Money Broking Companies)