Tuesday Aug 04, 2026

Tuesday Aug 04, 2026

Thursday, 4 June 2026 00:10 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

At the weekly Treasury Bill auction conducted yesterday, yields increased for the third consecutive week, reflecting the prevailing bearish sentiment in the market.

Accordingly, the weighted average yield on the 91-day Treasury Bill rose by 48 basis points to 9.84%, while the 182-day and 364-day tenors increased by 33 basis points and 19 basis points to 10.01% and 10.02%, respectively. These yield levels represent the highest seen in approximately 87 weeks, since early October 2024.

Following the recent 100 basis point increase in the Monetary Policy Rate, cumulative increases in Treasury bill weighted average yields have now reached approximately 153–176 basis points across the three tenors, significantly exceeding the magnitude of the policy rate adjustment.

The auction was undersubscribed, with only Rs. 111.16 billion raised during the first phase of competitive bidding against an offered amount of Rs. 140 billion, representing a subscription rate of 79.40%. Total bids received amounted to 1.52 times the offered volume, resulting in a bid-to-offer ratio of 1.52x.

The Phase II subscription across all three maturities is now open until 3.00 pm of business day prior to settlement date (i.e., 04.06.2026) at the WAYRs determined for the said ISINs at the auction. Given below are the details of the auction.

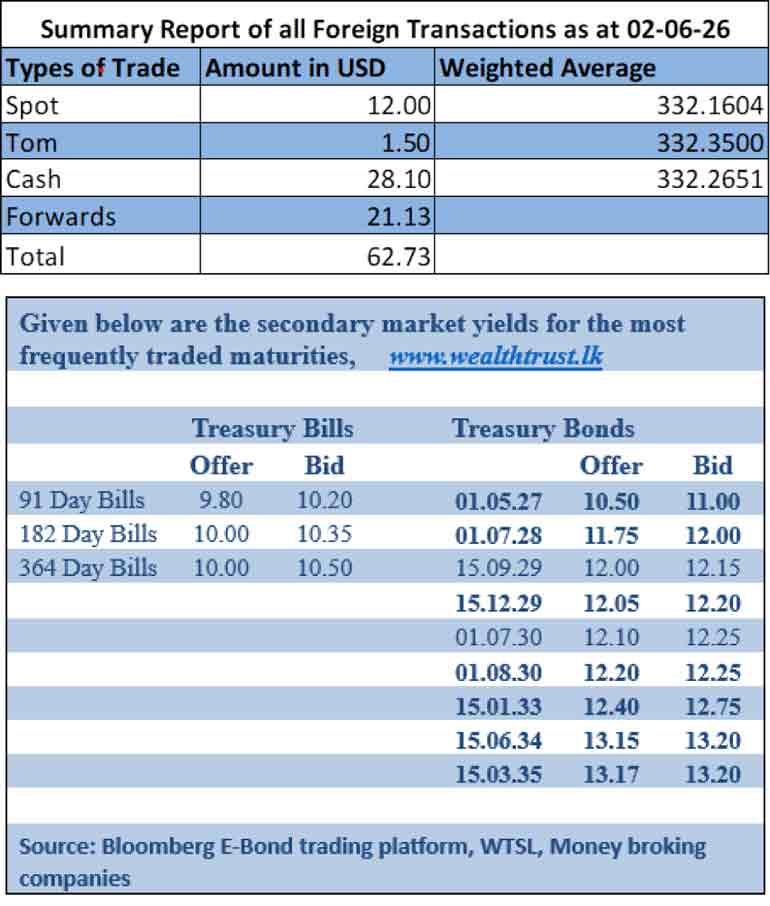

The secondary Bond market remained bearish yesterday, with yields edging higher across the curve amid continued selling pressure and cautious investor sentiment. Market participants also remained attentive to developments in global energy markets, where Brent crude oil extended gains above $ 97 per barrel.

Oil prices moved higher amid escalating geopolitical tensions in the Middle East. Fresh military exchanges involving the US, Iran, and other Gulf countries heightened concerns over regional stability and potential disruptions to energy supplies. Reports indicated renewed missile and drone attacks, alongside retaliatory US strikes. Meanwhile, uncertainty surrounding the status of ongoing US-Iran negotiations continued to support a geopolitical risk premium in oil markets. Against this backdrop, investor sentiment remained risk-off, contributing to the upward bias in domestic Bond yields. Market activity was seen at subdued levels; however, a few block transactions were observed.

The 01.05.28 maturity traded at the rate of 11.75%. The 15.10.29 maturity traded at the rate of 12.10%. The 01.07.30 and 01.08.30 maturities each traded at the rate of 12.15%. The 15.06.34 and 15.03.35 maturities traded at the rates of 13.15%-13.16% and 13.15%-13.185%.

In the money market, the net liquidity surplus was at Rs. 101.71 billion yesterday. An amount of Rs. 126.43 billion was deposited at Central Bank’s SDFR (Standing Deposit Facility Rate) of 8.25% as against an amount of Rs. 49.73 billion withdrawn from the Central Bank’s SLFR (Standing Facility Rate) of 9.25%. The Domestic Operations Department (DOD) of the Central Bank of Sri Lanka to continue to drain out an amount of Rs. 25 billion by way of overnight repo auction at a weighted average rate of 8.75%.

The weighted average rates on overnight call money and Repos were recorded at 9.15% and 9.20% respectively.

Forex market

The USD/LKR rate on spot contracts was seen closing at the rate of LKR. 335.00/337.00, up further from the previous day’s close of LKR. 332.50/333.50.

The total USD/LKR traded volume for 2 June was $ 62.73 million.

(References: Public Debt Management Office - Ministry of Finance, Central Bank of Sri Lanka, Bloomberg E-Bond Trading Platform, Money Broking Companies)