Sunday Jul 05, 2026

Sunday Jul 05, 2026

Thursday, 7 May 2026 05:51 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

The weekly Treasury Bill auction conducted yesterday, was fully subscribed, raising the entire Rs. 100 billion on offer at the first phase in competitive bidding. The bid to offer ratio stood at 2.15 times, reflecting the strong demand seen in the secondary market in the run up to the auction.

The weekly Treasury Bill auction conducted yesterday, was fully subscribed, raising the entire Rs. 100 billion on offer at the first phase in competitive bidding. The bid to offer ratio stood at 2.15 times, reflecting the strong demand seen in the secondary market in the run up to the auction.

Rates were seen stabilising. The weighted average yield rates on the 91-day tenor remained unchanged at 8.20% and the 364-day tenor also held steady at 8.52%. However, the 182-day registered a marginal decline of one basis point to 8.24% compared to the previous week. This followed an extended period where rates were seen on an uptrend with the yield on at least one tenor registering an increase over the past six weeks.

The Phase II subscription across all three tenors is now open until 3.00 pm of business day prior to settlement date (i.e., 07.05.2026) at the WAYRs determined for the said ISINs at the auction.

The secondary Bond market yesterday saw yields registering an increase for a third consecutive session. Uncertainty arising from mixed developments surrounding the ongoing Middle Eastern tensions and elevated crude oil prices continued to weigh on market sentiment.

However, market activity and transaction volumes were seen at healthy levels due to the execution of several block trades, as selling pressure was met with absorptive buying interest kicking in at the elevated levels.

Towards the latter part of the trading, it was reported that oil prices dropped on news that the U.S. and Iran were closing in on a deal to end the war, with Brent falling below $100. The market was seen going into a lull period as traders digested the latest development.

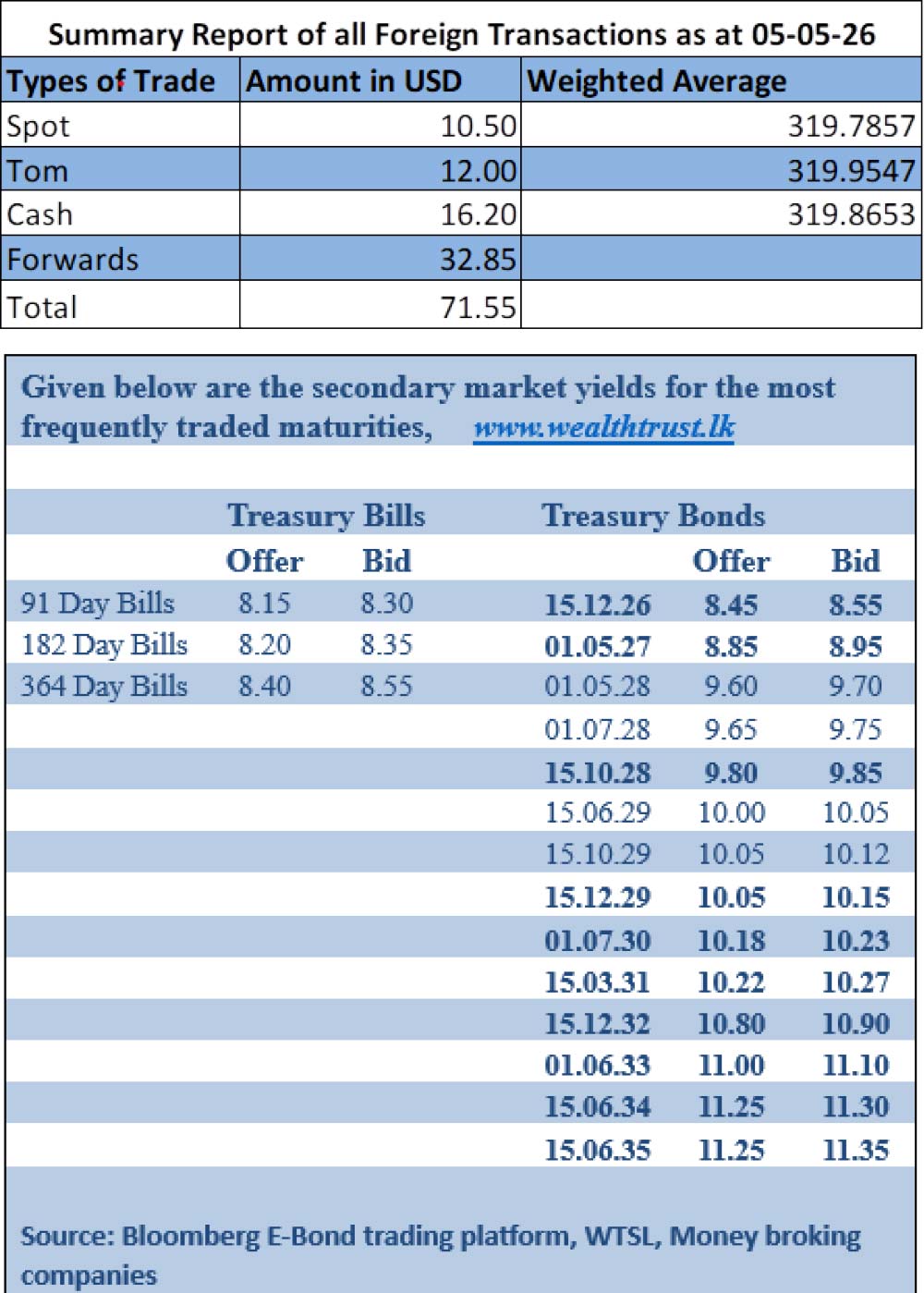

In the secondary Bond market, the 01.08.26 and 15.12.26 maturities were seen trading at the rates of 8.30%-8.20% and 8.55%. The 01.07.28 and 15.10.28 maturities were seen trading at the rates of 9.75%-9.70% and 9.85%-9.80% respectively. The 15.06.29 and 15.10.29 maturities were seen trading at the rates of 10.07%-10.05% and 10.08% respectively. The 15.05.30 maturity traded at the rate of 10.17%. The 01.10.32 maturity traded at the rate of 10.90%. The 15.03.31 maturity traded at the rate of 10.27%. The 15.06.34 maturity traded within the range of 11.31% -11.25%.

In secondary market Bill transactions, July Bills were seen trading at the rate of 8.20% on the back of large volumes ahead of the T-Bill auction.

In the money market, the net liquidity surplus recorded at Rs. 254.52 billion yesterday, continuing its uptrend. An amount of Rs. 184.52 billion was deposited at Central Bank’s SDFR (Standing Deposit Facility Rate) of 7.25%. The Domestic Operations Department (DOD) of the Central Bank of Sri Lanka to continue to drain out an amount of Rs. 70 billion by way of overnight repo auction at a weighted average rate of 7.70%

The weighted average rates on overnight call money and Repos were recorded at 7.75% and 7.80%.

Forex market

The USD/LKR rate on spot contracts was seen closing the day at Rs. 320.20/321.00 as against the previous day’s spot closing level of Rs. 319.90/320.40.

The total USD/LKR traded volume for 5 May was $ 71.55 million.

(References: Public Debt Management Office - Ministry of Finance, Central Bank of Sri Lanka, Bloomberg E-Bond Trading Platform, Money Broking Companies)