Tuesday Jul 07, 2026

Tuesday Jul 07, 2026

Monday, 18 May 2026 00:02 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

The secondary Bond market last week saw sentiment shaped by a tug-of-war between supportive domestic fundamentals and persistent geopolitical uncertainty.

The week commenced on a cautious note, with yields broadly holding steady across most of the curve as market participants consolidated positions. Investor sentiment remained restrained amid external uncertainty, particularly the ongoing Middle Eastern conflict and elevated crude oil prices, which continued to cloud the global macro backdrop. Mixed geopolitical signals reinforced the defensive tone.

However, domestic fundamentals offered meaningful support. Sri Lanka’s latest fiscal performance data for February 2026 painted an encouraging picture, with Government revenue and grants rising 35.5% YoY to Rs. 1.03 trillion in the first two months of the year. The primary surplus expanded 66.1% YoY to Rs. 545.42 billion and the overall Budget balance swung to a surplus of Rs. 169.71 billion compared to a deficit in the corresponding period last year, helping anchor investor confidence.

Market sentiment improved significantly on Tuesday following the Treasury Bond auction outcome, which was viewed as constructive despite the challenging external backdrop. Weighted average yields were accepted broadly in line with or below market expectations, prompting aggressive buying interest and a notable rally in yields.

However, profit-taking emerged in the latter half of the week, leading yields to edge moderately higher from Tuesday’s lows. Nevertheless, the upward adjustment remained measured, with rates holding below prior highs as buying interest continued to absorb selling pressure.

Overall market activity remained selectively subdued as investors largely maintained a cautious wait-and-see stance amid prevailing uncertainty, while transaction volumes remained healthy, supported by several sizeable block trades.

In terms of the secondary Bond market trade summary:

During the week, the 01.08.26 maturity traded at the rate of 8.15%, while the 15.12.26 maturity traded within intraweek highs and lows of 8.45% to 8.40% respectively.

Moving into the 2028 tenors, the 15.02.28 maturity traded within intraweek highs and lows of 9.65% to 9.60%, while the 01.07.28 maturity traded at the rate of 9.70%. The 15.10.28 and 15.12.28 maturities traded within intraweek highs and lows of 9.77% to 9.71% and 9.80% to 9.75% respectively.

Further along the curve, the 15.06.29 maturity traded within intraweek highs and lows of 9.85% to 9.80%, while the 15.09.29 and 15.10.29 maturities traded within intraweek highs and lows of 9.95% to 9.90% respectively. The 15.12.29 maturity traded at the rate of 9.95%.

On the medium end, the 01.03.30 and 01.07.30 maturities traded within intraweek highs and lows of 10.10% to 10.00% and 10.15% to 10.05% respectively, while the 15.05.30 maturity traded at the rate of 10.10%. The 01.08.30 maturity traded within intraweek highs and lows of 10.10% to 10.05%.

Further out the curve, the 01.10.32 and 15.12.32 maturities traded at the rates of 10.75% and 10.80% respectively.

At the long end, the 15.06.34 maturity traded within intraweek highs and lows of 11.22% to 11.08%, while the 15.06.35 maturity traded at the rate of 11.18%.

The weighted average yields at last Tuesday’s Treasury Bond auction came in line with or below market expectations, an impressive outcome given the external backdrop driven by the Middle East conflict and elevated crude oil prices. However, the auction was undersubscribed, with Rs. 176.62 billion raised against the Rs. 250 billion offered across the first and second phases. The bid-to-accepted ratio stood at 2.47x.

The maturity-wise results across the 4 offered securities:

The 01.08.30 maturity was issued at a weighted average rate of 10.16%, broadly in line with market expectations, with the full offered amount accepted in the 1st phase.

The 15.06.34 maturity was issued at 11.24%, also in line with pre-auction quotes, with the full offered amount raised in competitive bidding.

The 15.08.36 maturity was issued at 11.40%, which was below market expectations, but remained undersubscribed across both phases.

The 15.08.39 maturity was rejected.

Further to the Treasury Bond auction, an additional Rs. 13 billion was raised via the Direct Issuance Window, representing the maximum amount offered. This was raised against a total market subscription of Rs. 73.08 billion, an overwhelming response.

To recap, the weekly Treasury Bill auction conducted last Wednesday, was fully subscribed, raising the entire Rs. 80 billion on offer at the first phase in competitive bidding. The bid to offer ratio stood at 2.74 times.

Rates were seen declining across the board for the first time in 10 weeks. This reversed the upward trend observed in the recent past, with yields retreating from the highs touched during late April. Accordingly, the weighted average yield rates on the 91-day tenor declined by 07 basis points to 8.13%, the 182-day tenor registered a drop of 01 basis point to 8.23%, and the 364-day tenor decreased by 03 basis points to 8.49%.

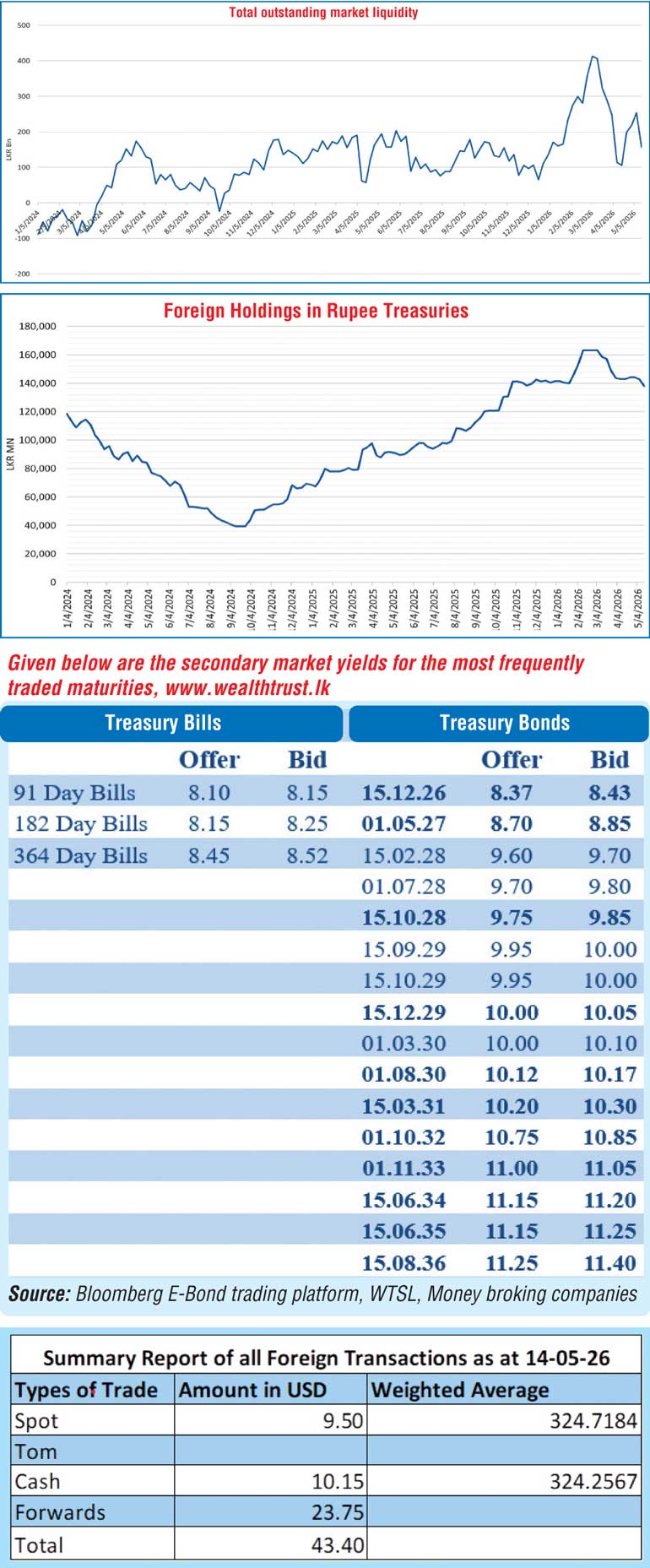

The foreign holdings of rupee-denominated Government securities dropped lower, recording a net outflow for the second consecutive week amounting to Rs. 4.73 billion. Accordingly, the total foreign holdings declined further to Rs. 138 billion during the week ended 14 May.

In the money market, the total outstanding liquidity surplus was recorded at Rs. 156.80 billion against the previous week’s Rs. 253.66 billion. The weighted average interest rates on Call Money and Repo stood at 7.79% and 7.85% respectively at the close of the week as compared to 7.76% and 7.80% respectively the previous week.

Forex market

In the forex market, the USD/LKR rate on spot contracts was seen trading within the range of a high of Rs. 321.90 and a low of Rs. 326.00.

The daily USD/LKR average traded volume for the first four trading days of the week stood at $ 66.15 million.

(References: Public Debt Management Office - Ministry of Finance, Central Bank of Sri Lanka, Bloomberg E-Bond Trading Platform, Money Broking Companies)