Wednesday Jul 08, 2026

Wednesday Jul 08, 2026

Wednesday, 20 May 2026 05:38 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

The secondary Bond market yesterday turned bearish and saw rates increase for the second consecutive day.

The secondary Bond market yesterday turned bearish and saw rates increase for the second consecutive day.

Selling pressure pushed yields higher, however, some renewed buying emerged at the elevated levels keeping a cap on rates. This mirrored the global Bond market rate increase. As a result, secondary Bond market two-way quotes closed the day notably higher.

Market activity remained defensive shaped by ongoing geopolitical uncertainty surrounding the Middle Eastern conflict and concerns over elevated crude oil prices, both of which continue to cloud the near-term macro-outlook. However, transaction volumes were seen at healthy levels due to the execution of several block transactions due to the intermittent emergence of buying support.

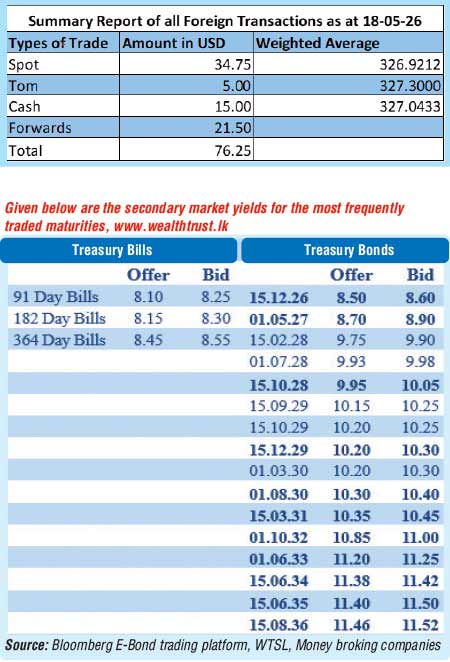

Accordingly, the 01.08.26 maturity traded at the rate of 8.25%. The 01.07.28 and 15.10.28 maturities traded at the rates of 9.95% and 10.00% respectively. The 15.09.29 and 15.10.29 maturities traded up the ranges of 10.05% to 10.20% and 10.15% to 10.30% respectively. The 01.07.30 maturity traded at the rate of 10.30%. The 15.06.34 maturity traded up the range of 11.32% to 11.42%. The 15.06.35 maturity traded within the range of 11.42%-11.45%. The 15.08.36 maturity traded within the range of 11.44%-11.48%.

Meanwhile, the Treasury Bill auction scheduled for today, will have a total amount of Rs. 140 billion on offer. This will comprise of Rs. 65 billion offered on the 91-day maturity, Rs 40.00 billion on the 182-day maturity and Rs. 35.00 billion on the 364-day maturity. This is below the maturity in line with the scheduled auction, which is estimated to be approximately Rs. 162.00 billion.

For reference, the previous Treasury Bill auction conducted last Wednesday was fully subscribed, raising the entire Rs. 80.00 billion on offer at the 1st phase in competitive bidding. The bid to offer ratio stood at 2.74 times.

Rates declined across the board for the first time in 10 weeks. This reversed the upward trend observed in the recent past, with yields retreating from the highs touched during late April. Accordingly, the weighted average yield rates on the 91-day tenor declined by 07 basis points to 8.13%, the 182-day tenor registered a drop of 01 basis point to 8.23%, and the 364-day tenor decreased by 03 basis points to 8.49%.

In the money market, the net liquidity surplus was recorded at Rs. 181.68 billion yesterday. An amount of Rs 150.38 billion was deposited at Central Bank’s SDFR (Standing Deposit Facility Rate) of 7.25% as against an amount of Rs. 43.71 billion withdrawn from the Central Bank’s SLFR (Standing Lending Facility Rate) of 8.25%. In addition, the Domestic Operations Department (DOD) of the Central Bank of Sri Lanka drained out an amount of Rs. 75 billion by way of overnight repo auction at a weighted average rate of 7.74%.

The weighted average rates on overnight call money and Repo were recorded at 7.84% and 7.89% respectively.

Forex market

In the forex market, the USD/LKR rate on spot contracts traded within the range of a low of Rs. 328.90 and a high of Rs. 327.85.

The total USD/LKR traded volume for 18 May 2026 was $ 76.25 million.

(References: Public Debt Management Office- Ministry of Finance, Central Bank of Sri Lanka, Bloomberg E-Bond trading platform, Money broking companies)