Wednesday Jun 03, 2026

Wednesday Jun 03, 2026

Wednesday, 4 March 2026 00:04 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

The secondary Bond market yesterday opened the week with yields initially increasing sharply as a knee-jerk reaction to the news of the ongoing Middle East tensions.

However, renewed buying interest was seen kicking in at the elevated levels which drove a strong recovery. Despite this recovery, secondary market two-way quotes were seen closing higher day-on-day. Trading activity and transaction volumes were seen at healthy levels as the market adjusted and settled to the ongoing developments.

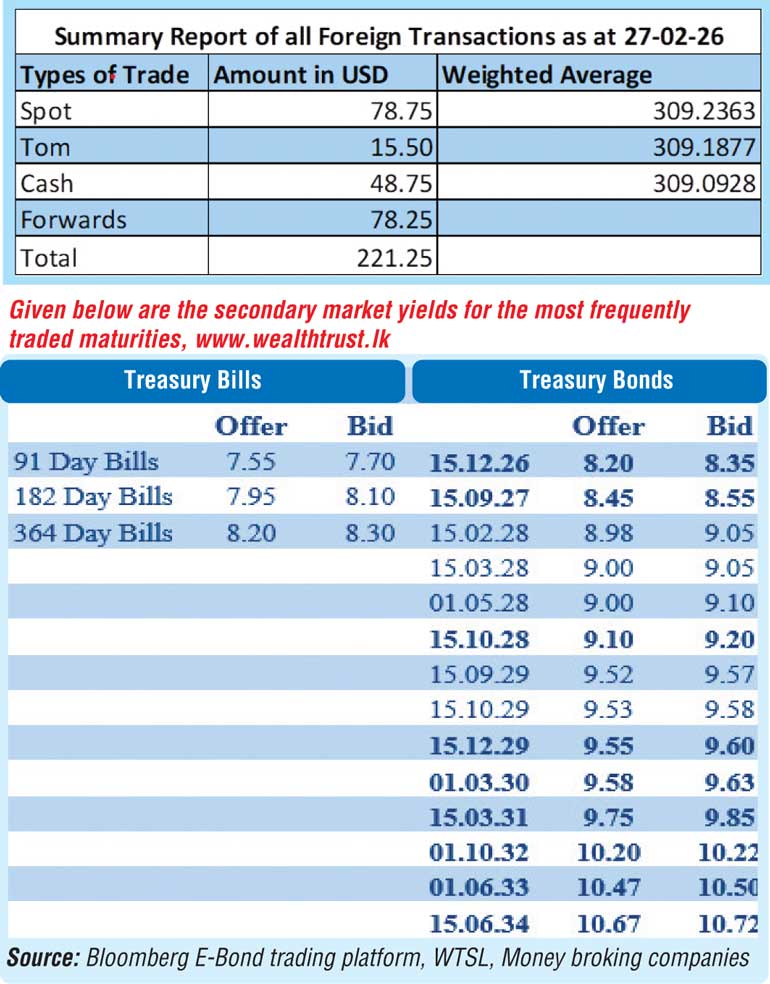

The 15.12.26 maturity traded at the rate of 8.30%. The 15.02.28 maturity traded at the rate of 9.00%. The 15.06.29, 15.09.29 and 15.12.29 maturities traded down from intraday highs to lows of 9.50%-9.45%, 9.60%-9.55%, 9.63%-9.60% respectively. The 01.03.30 maturity traded up from an intraday low of 9.56% to a high of 9.63% before easing back down to trade at 9.60% at the close. The 15.03.31 maturity traded down the range of 9.85%-9.80%. The 01.10.32 maturity traded at the rate of 10.20%. The 01.06.33 traded down from a high of 10.55% to a low of 10.50%. The 15.06.34 maturity traded at the rate of 10.65% and the 15.06.35 maturity at the rate of 10.74%.

Meanwhile, the weekly Treasury Bill auction scheduled for today will have on offer a total amount of Rs. 120 billion. The auction will comprise of Rs. 15 billion in 91-day Bills, Rs. 70 billion in 182-day Bills, and Rs. 35 billion in 364-day Bills. The offered amount is below the maturing volume, which is estimated at around Rs. 125.95 billion.

For context, the weekly Treasury Bill auction held last Wednesday (25 February), saw yields continue their downward trajectory, with weighted average rates declining across all maturities for the sixth consecutive week. Accordingly, the rate on the 91-day Bill declined by 3 basis points to 7.63%, the rate on the 182-day Bill dropping by 7 basis points to 7.92% and the 364-day Bill saw its yield ease by 3 basis points to 8.24%.

The auction was undersubscribed at the first phase in competitive bidding, raising only Rs. 67.88 billion, or 75.42% of the total offered amount of Rs. 90 billion. Nevertheless, demand extended to the second phase where Rs. 31.12 billion was raised, out of the total market subscription of Rs. 48.27 billion. Accordingly, the aggregate accepted amount of the issuance was Rs. 99 billion – not only bridging the shortfall at the first phase but also raising an additional 10% on top.

In money markets, the net liquidity surplus was recorded at Rs. 332.49 billion yesterday. The Domestic Operations Department (DOD) of the Central Bank of Sri Lanka was seen draining out an amount of Rs. 75 billion by way of overnight repo auction at a weighted average rate of 7.60% while an amount of Rs. 258.12 billion was deposited at Central Bank’s SDFR (Standing Deposit Facility Rate) of 7.25%. An amount of Rs. 0.63 billion was withdrawn from the Central Bank’s SLFR (Standing Lending Facility Rate) of 8.25%.

The weighted average rates on overnight call money and Repo stood at 7.68% and 7.71% respectively.

The total secondary market Treasury Bond/Bill transacted volume for 27 February was Rs. 13.87 billion.

Forex market

The forex market also experienced considerable volatility following the news of the Middle East conflict. Accordingly, the USD/LKR rate on spot contracts was seen depreciating, to close the day at Rs. 310.10/310.30 as against the previous day’s closing level of Rs. 309.29/309.32 and subsequent to trading at a high of Rs. 309.70 and a low of Rs. 310.40.

The total USD/LKR traded volume for 27 February was $ 221.25 million.

(References: Central Bank of Sri Lanka, Bloomberg E-Bond trading platform, Money broking companies)