Friday Jul 17, 2026

Friday Jul 17, 2026

Monday, 16 March 2026 04:40 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

Sri Lanka’s secondary Government Bond market last week experienced a volatile start before stabilising toward the latter half, as global developments surrounding oil prices and geopolitical tensions drove sentiment.

Sri Lanka’s secondary Government Bond market last week experienced a volatile start before stabilising toward the latter half, as global developments surrounding oil prices and geopolitical tensions drove sentiment.

Yields initially rose sharply last Monday following a surge in global energy prices, with Brent crude briefly climbing close to $ 120 per barrel amid supply disruption concerns in the Middle East. This triggered a knee-jerk rise in yields and cautious positioning by market participants.

However, the move reversed on Tuesday as global oil prices corrected sharply, easing inflation and external sector concerns for oil-importing economies such as Sri Lanka. The decline in crude prices compressed risk premiums and triggered renewed buying interest from banks and institutional investors, driving yields lower across the curve.

For the remainder of the week, the market largely consolidated, with activity remaining subdued around the Treasury Bond auction as participants adopted a cautious stance amid ongoing geopolitical uncertainty.

Despite the week’s volatility and the supply from the Treasury Bond auction, yields closed broadly unchanged week-on-week following the recovery, with ample system liquidity, compressed money market rates, and positive results at the auctions helping keep rates anchored around prevailing levels.

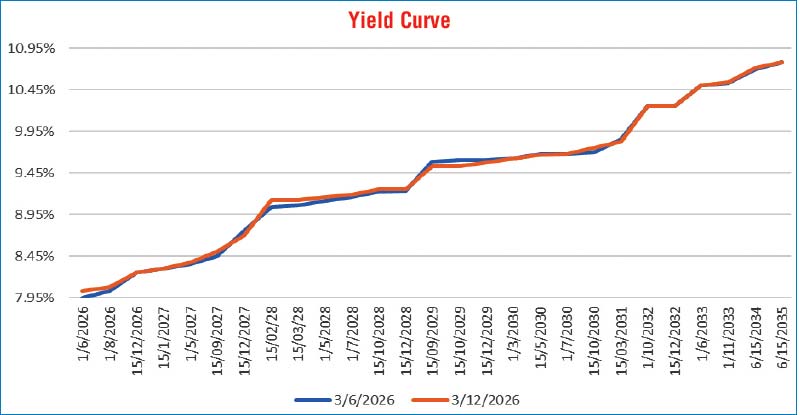

During the week, the 01.08.26 maturity traded at 8.30%, while the 01.05.27 maturity traded at 8.40%. The 15.09.27 maturity initially spiked to an intraweek high of 8.80% before easing back to trade at a low of 8.55%.

Moving into the 2028 tenors, the 15.02.28 maturity eased down from an intraweek high of 9.30% to a low of 9.10%, while the 15.03.28 maturity traded within the range of 9.15%–9.12%. The 15.12.28 maturity also retraced from an intraweek high of 9.65% to a low of 9.30%.

Further along the curve, the 15.06.29 maturity traded at 9.50%. The 15.09.29 maturity traded down from an intraweek high of 9.65% to a low of 9.50%.

On the medium end, the 01.03.30 maturity traded down from an intraweek high of 9.85% to a low of 9.65%.

Further out the curve, the 01.10.32 maturity traded within 10.25%–10.23%. The 01.06.33 maturity retraced from an intraweek high of 10.72% to a low of 10.50%, while the 01.11.33 maturity traded within 10.55%-10.50%.

At the long end, the 15.06.34 maturity traded within the range of 10.90%–10.72%, while the 15.06.35 maturity traded down from an intraweek high of 11.00% to a low of 10.80%.

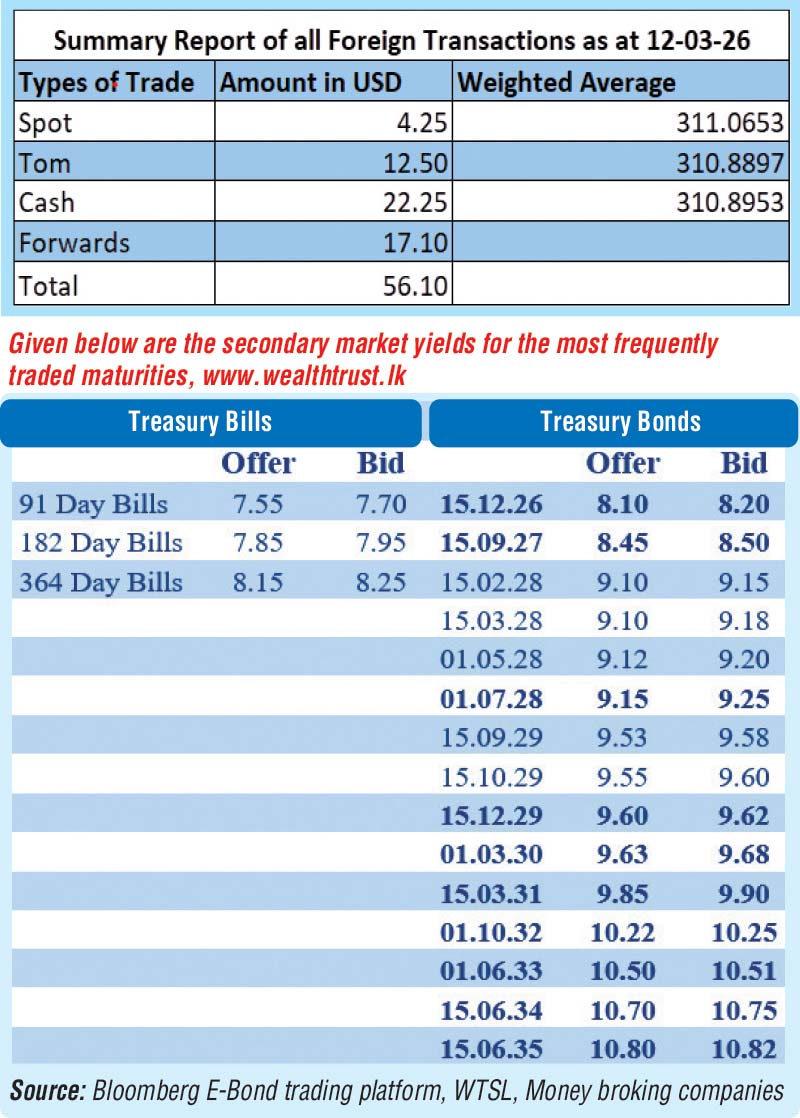

The weekly Treasury Bill auction conducted last Wednesday (11) saw weighted average yields decline marginally. Accordingly, the rate on the 91-day Bill dipped by two basis points to 7.61% and the rate on the 182-day Bill edged lower by one basis point to 7.91%. However, the 364-day Bill saw its yield hold static at 8.23%. The auction was undersubscribed at the first phase in competitive bidding. The bid-to-cover ratio stood at 2.33 times.

This was followed by a Treasury Bond auction conducted on 12 March which produced a positive outcome, registering weighted average rates below or in-line with prevailing secondary market level. However, the auction went undersubscribed only raising Rs. 87.02 billion or 66.94% out of Rs. 130 billion on offer at the first and second phases — across three available maturities. The bids received-to-accepted amount ratio stood at 2.45 times.

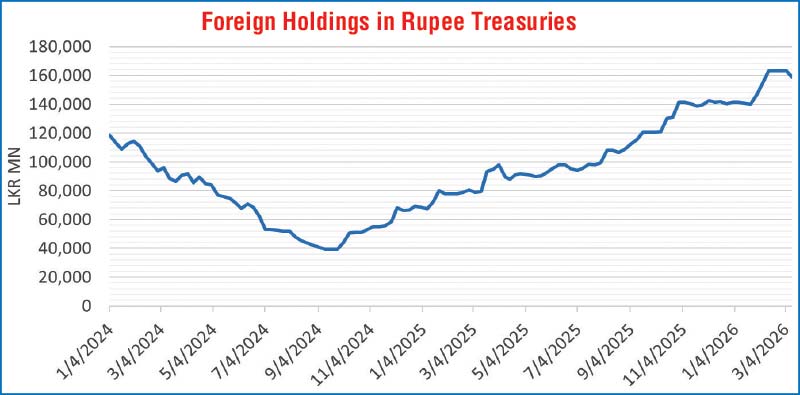

The foreign holdings of rupee-denominated Government securities recorded a net outflow for the second consecutive week amounting to Rs. 4.50 billion and as a result, total foreign holdings dipped to Rs. 158.67 billion during the week ended 12 March.

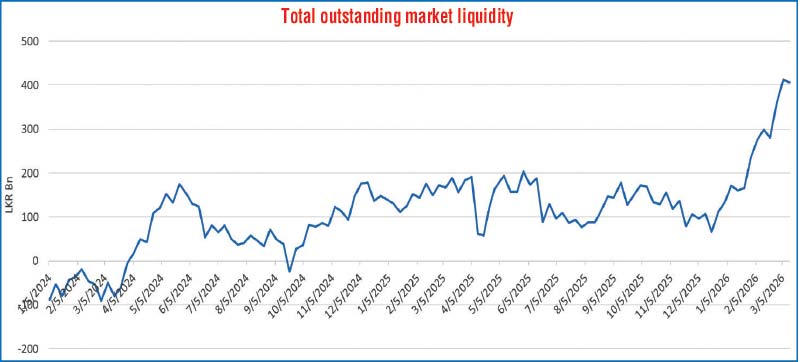

In the money market, the total outstanding liquidity surplus in the inter-bank market remained elevated and stood at Rs. 406.78 billion as at the week ending 13 March 2026, dipping slightly from Rs. 412.92 billion recorded the previous week. The Domestic Operations Department (DOD) of the Central Bank continued to drain out liquidity during the week by way of overnight Repo auctions at weighted average yields ranging from 7.48% to 7.40%, as well as one week term repo at the rate of 7.61%.

The weighted average interest rates on Call Money and Repo to stood at 7.60% and 7.61%, respectively, at the close of the week, against its previous weeks closings of 7.66% and 7.69%.

Forex market

In the forex market, the USD/LKR rate on spot contracts was seen closing the week depreciating to Rs. 311.15/311.25 as against the previous week’s closing level of Rs. 310.80/311.20. This was subsequent to trading at a high of Rs. 310.90 and a low of Rs. 311.60.

The daily USD/LKR average traded volume for the first four trading days of the week stood at $ 105.57 million.

(References: Public Debt Management Office - Ministry of Finance, Central Bank of Sri Lanka, Bloomberg E-Bond Trading Platform, Money Broking Companies)