Wednesday Jun 03, 2026

Wednesday Jun 03, 2026

Monday, 30 March 2026 04:50 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

Secondary Bond market last week was characterised by choppy trading conditions and a largely externally driven narrative.

Secondary Bond market last week was characterised by choppy trading conditions and a largely externally driven narrative.

The dominant drivers remained the ongoing Middle Eastern conflict and the accompanying movements in Brent crude oil prices. Episodes of softening oil prices, often linked to temporary de-escalation signals from the US and diplomatic developments, triggered downward adjustments in yields, supporting brief bullish phases. Conversely, rebounds in oil prices, driven by renewed geopolitical uncertainty and conflicting reports, led to upward pressure on yields.

Despite intermittent bullish phases, the market lacked a sustained directional bias. External shocks, including rebounds in oil prices and conflicting US–Iran developments, kept sentiment cautious.

In addition, the weekly T-Bill auction, which saw rates increase for the first time in 10 weeks, contributed to the upward bias in yields. Furthermore, the Central Bank of Sri Lanka was seen holding policy rates steady at its announcement during the week.

Overall, secondary market two-way quotes closed the week broadly unchanged compared to the previous week across the belly to long end of the yield curve, while the very short end recorded a modest upward adjustment despite underlying fluctuations.

In terms of the Secondary Bond market trade summary:

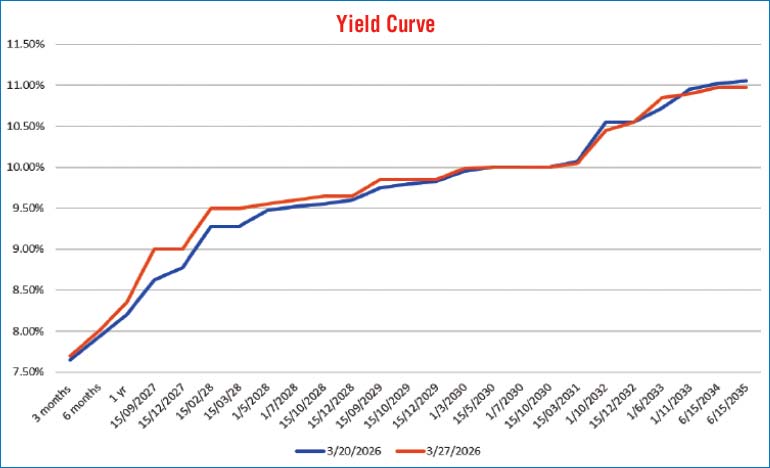

During the week, the 01.05.27 maturity traded within intraweek highs and lows of 8.72%–8.57%.

Moving into the 2028 tenors, the 15.02.28 maturity traded within intraweek highs and lows of 9.70%–9.30%, while the 15.03.28 maturity traded at 9.60%. The 01.05.28 maturity traded within intraweek highs and lows of 9.70%–9.60%, while the 15.10.28 maturity traded within intraweek highs and lows of 9.53%–9.40%.

Further along the curve, the 15.06.29 maturity traded within intraweek highs and lows of 10.05%–9.65%. The 15.09.29 maturity traded within intraweek highs and lows of 10.12%–9.75%, while the 15.10.29 maturity traded within intraweek highs and lows of 10.08%–9.70%. The 15.12.29 maturity traded within intraweek highs and lows of 10.12%–9.70%.

On the medium end, the 01.03.30 maturity traded within intraweek highs and lows of 10.10%–9.70%, while the 15.05.30 maturity traded within intraweek highs and lows of 10.22%–10.18%. The 15.03.31 maturity traded within intraweek highs and lows of 10.30%–9.85%, while the 01.12.31 maturity traded within intraweek highs and lows of 10.37%–10.33%.

Further out the curve, the 01.10.32 maturity traded at 10.68%, while the 15.12.32 maturity traded within intraweek highs and lows of 10.85%–10.45%. The 01.06.33 maturity traded within intraweek highs and lows of 11.05%–10.72%.

At the long end, the 15.09.34 maturity traded within intraweek highs and lows of 11.23%–11.12%, while the 15.06.35 maturity traded within intraweek highs and lows of 11.05%–10.97%.

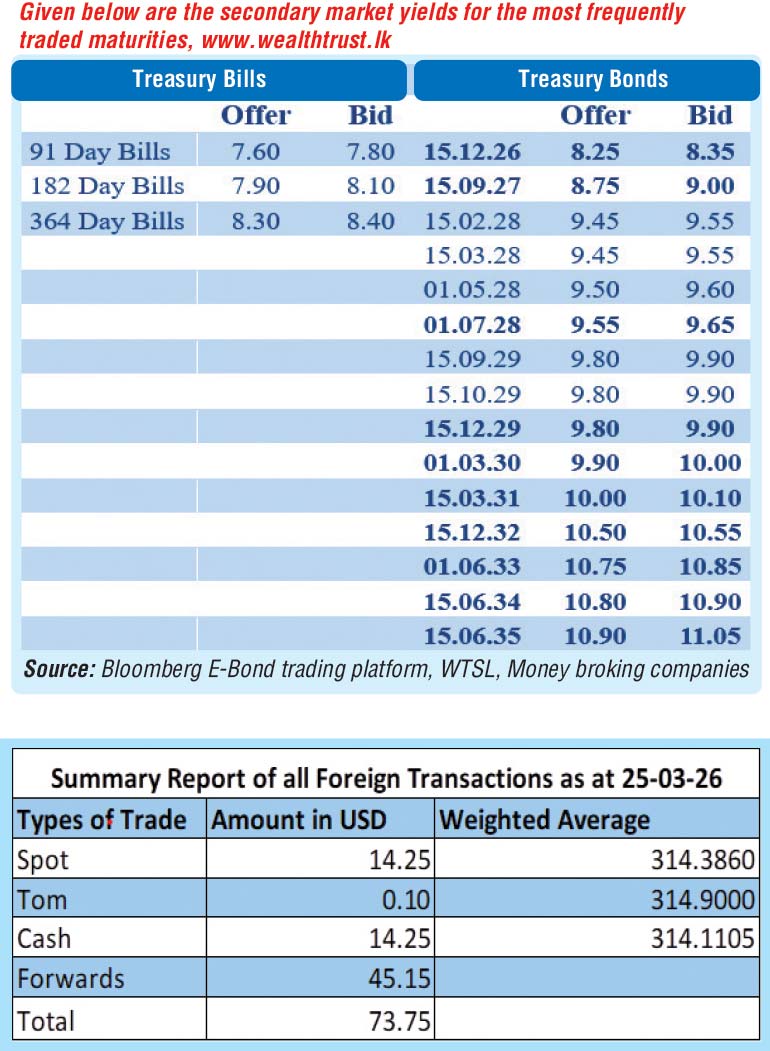

The weekly Treasury Bill auction conducted last Wednesday (25) saw weighted average yields increase across the board for the first time in 10 weeks. Accordingly, the yield on the 91-day Bill rose by 3 basis points to 7.64%, the 182-day Bill increased by 4 basis points to 7.95%, while the 364-day Bill saw an uptick of 9 basis points to 8.32%. The auction was undersubscribed at the first phase in competitive bidding, raising only Rs. 34.94 billion, or 43.68% of the total offered amount of Rs. 80 billion. The bid-to-cover ratio stood at 1.24 times.

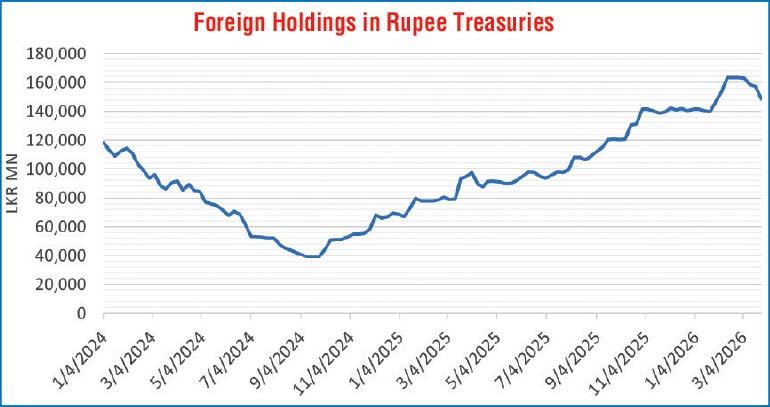

The foreign holdings of rupee-denominated Government securities recorded a net outflow for the fourth consecutive week, amounting to a sizeable Rs. 8.68 billion and as a result, total foreign holdings dropped sharply to Rs. 148.60 billion during the week ended 26 March.

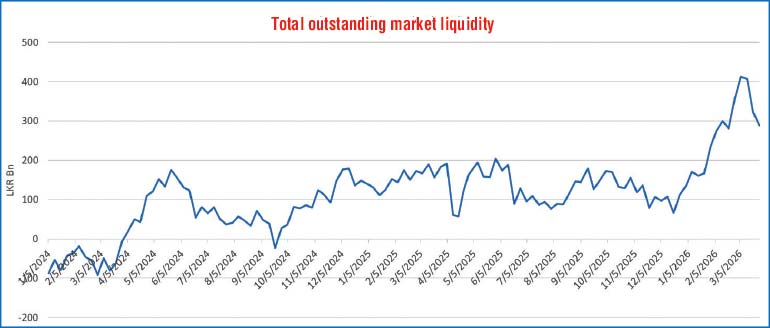

In the money market, the total outstanding liquidity surplus in the inter-bank market remained elevated but dropped to Rs. 288.31 billion as at the week ending 27 March 2026, from Rs. 323.04 billion recorded the previous week. The Domestic Operations Department (DOD) of Central Bank continued to drain out liquidity during the week by way of overnight Repo auctions at weighted average yields ranging from 7.59% to 7.61%, as well as one week term repo at the W.A rate of 7.66%.

The weighted average interest rates on Call Money and Repo stood at 7.60% and 7.65%, respectively, at the close of the week ending 20 March against its previous weeks closings of 7.59% and 7.61%.

Forex market

In the forex market, the USD/LKR rate on spot contracts was seen closing the week depreciating to Rs. 314.70/315.00 as against the previous week’s closing level of Rs. 311.85/312.00. This was subsequent to trading at a high of Rs. 311.90 and a low of Rs. 315.10.

The daily USD/LKR average traded volume for the first four trading days of the week stood at $ 55.78 million.

(References: Public Debt Management Office - Ministry of Finance, Central Bank of Sri Lanka, Bloomberg E-Bond Trading Platform, Money Broking Companies)