Wednesday Aug 05, 2026

Wednesday Aug 05, 2026

Monday, 23 February 2026 00:00 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

The yields in the secondary Bond market edged higher last week, as market participants moved to realise gains following the sustained rally observed in the weeks prior. Rates remained broadly stable at the start of the week amid a consolidation phase, before gradually trending higher towards the latter half, with the upward adjustment more pronounced across the belly to the long end of the curve.

Profit-taking activity was the primary driver behind the rise in yields, particularly across medium- to longer-dated maturities, while movements at the short end remained relatively contained. Additionally, external developments — including escalating US-Iran tensions and the uptick in global oil prices — weighed on overall market sentiment.

Despite the upward adjustment in yields, trading activity and transaction volumes remained healthy throughout the week, supported by several sizeable block trades. Overall, secondary market two-way quotes closed higher on a week-on-week basis, resulting in a modest upward parallel shift in the yield curve.

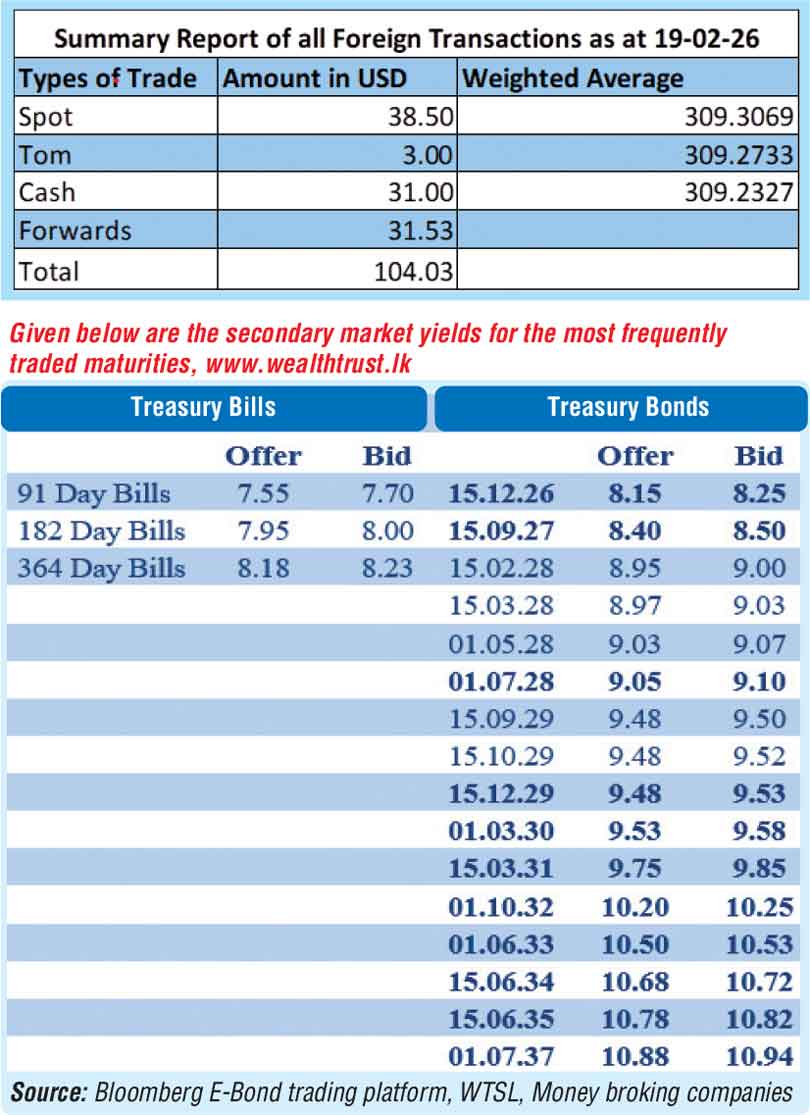

In terms of the secondary Bond market, the trade summary is as follows:

The 01.08.26 maturity traded within the range of 8.05%–8.10%. The 15.01.27 maturity traded at 8.30%, while the 01.05.27 maturity traded up to 8.40%. The 15.09.27 maturity traded at 8.45%.

Moving into the 2028 tenors, the 01.05.28 maturity traded up from an intraweek low of 9.02% to a high of 9.05%, while the 01.07.28 maturity traded up within the range of 9.03%–9.05%. The 01.09.28 maturity traded at 9.10%.

Further along the curve, the 15.06.29 maturity traded up from an intraweek low of 9.34% to a high of 9.40%. The 15.09.29 maturity traded up from 9.43% to 9.51%, while the 15.12.29 maturity traded up from an intraweek low of 9.45% to a high of 9.50%.

On the medium end, the 01.03.30 maturity traded up from an intraweek low of 9.49% to a high of 9.55%, while the 01.07.30 maturity traded up from 9.50% to 9.55%. The 15.03.31 maturity traded up from an intraweek low of 9.70% to a high of 9.78%.

Further out the curve, the 01.10.32 maturity traded up notably from an intraweek low of 10.10% to a high of 10.25%. The 01.06.33 maturity traded up from 10.37% to 10.50%, while the 01.11.33 maturity traded up from an intraweek low of 10.38% to a high of 10.54%.

At the long end, the 15.06.34 maturity traded up from 10.65% to 10.70%, while the 15.06.35 maturity traded up from an intraweek low of 10.74% to a high of 10.80%. The 01.07.37 maturity traded up from 10.85% to 10.92%, and the 15.08.39 maturity traded at 10.92%.

Meanwhile, the weekly Treasury Bill auction held last Wednesday (18) registered a positive outcome, with yields continuing to trend downward. The weighted average rates declined across all maturities for the fifth consecutive week. The shorter-tenor maturities saw a more pronounced downward adjustment, with the rate on the 91-day Bill declining by six basis points to 7.66% and the rate on the 182-day Bill dropping by eight basis points to 7.99%. The 364-day Bill saw its yield ease more modestly, by four basis points to 8.27%. The auction was fully subscribed, raising the entire Rs. 60 billion offered.

In addition, demand extended to the second phase, where an additional Rs. 6—the maximum offered—was raised out of a total market subscription of a staggering Rs. 34.52 billion. Accordingly, the aggregate amount accepted at the issuance amounted to Rs. 66.00 billion.

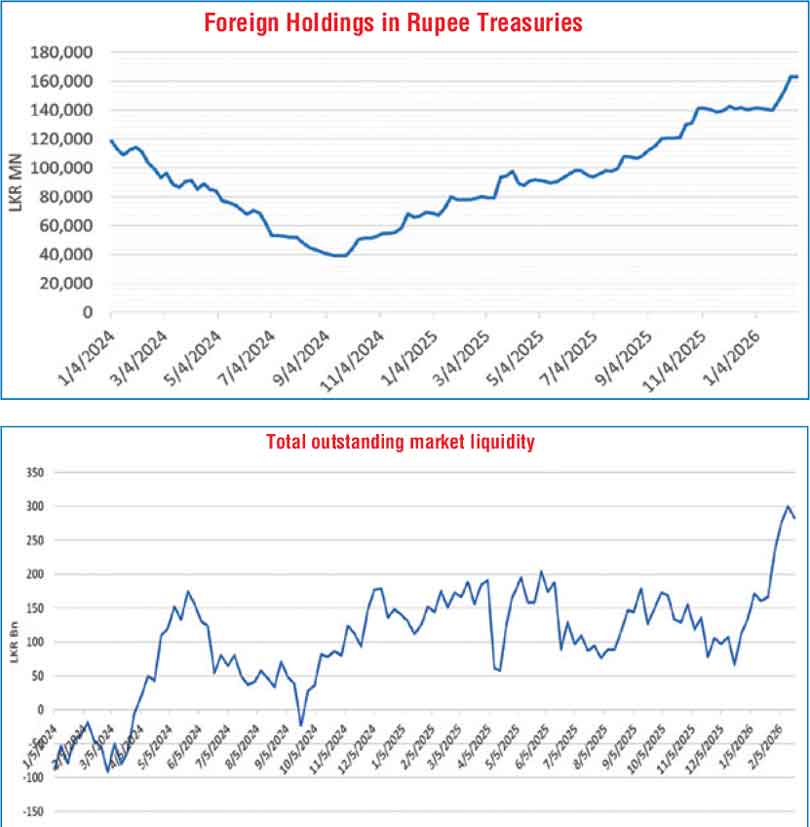

The foreign holdings of rupee-denominated Government securities rose for a fourth consecutive week, albeit recording a marginal net inflow of Rs. 12 million. As a result, total foreign holdings increased to Rs. 163.41 billion during the week ended 19 February.

In the money market, the total outstanding liquidity surplus in the inter-bank market stood at Rs. 283.22 billion as at the week ending 20 February 2026, down from Rs. 299.68 billion recorded in the previous week. The Domestic Operations Department (DOD) of the Central Bank continued to drain out liquidity during the week by way of overnight repo auctions at weighted average yields ranging from 7.63% to 7.65%.

The weighted average interest rates on Call Money and Repo stood at 7.67% and 7.69%, respectively, at the close of the week against the previous week’s closings of 7.67% and 7.70%.

Forex market

In the forex market, the USD/LKR rate on spot contracts was seen closing the week depreciating to Rs. 309.35/309.40 as against the previous week’s closing level of Rs. 309.20/309.25. This was subsequent to trading at a high of Rs. 309.20 and a low of Rs. 309.40.

The daily USD/LKR average traded volume for the first four trading days of the week stood at $ 83.46 million.

(References: Public Debt Management Office - Ministry of Finance, Central Bank of Sri Lanka, Bloomberg E-Bond Trading Platform, Money Broking Companies)