Sunday Jul 05, 2026

Sunday Jul 05, 2026

Monday, 11 May 2026 00:02 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

The secondary Bond market began last week on a cautious footing, with yields initially picking up from Monday through Wednesday as escalating Middle Eastern tensions and elevated crude oil prices weighed on sentiment. However, the selling pressure was met with absorptive buying interest, signalling the emergence of value-based demand at the elevated levels.

The turning point came late Wednesday after reports suggested that the US and Iran were nearing a deal to end hostilities, causing Brent crude to fall below $ 100 per barrel and materially improving risk sentiment.

This set the stage for a strong relief rally last Thursday, with yields declining sharply across the curve as easing geopolitical concerns reduced fears over inflation pressures and external stability. Robust market activity accompanied the move, with two-way quotes re-priced firmly lower. Friday saw the market continue the trend and edge further lower, locking in these gains and consolidating, allowing it to close the week on a distinctly positive note. As a result, secondary Bond market two-way quotes closed lower week on week.

Activity and transaction volumes for the week were observed at relatively higher levels compared to the subdued levels seen in previous weeks, as strong directional cues emerged amid mixed geopolitical developments.

In terms of the secondary Bond market trade summary:

During the week, the 01.08.26 maturity traded down from an intraweek high of 8.32% to a low of 8.20%, while the 15.12.26 maturity traded within the range of 8.65%–8.52%.

Moving into the 2028 tenors, the 01.07.28 maturity traded down from an intraweek high of 9.80% to a low of 9.65%. The 15.10.28 maturity similarly traded down from 9.85% to 9.75%, while the 15.12.28 maturity traded at 9.78%.

Further along the curve, the 15.06.29 maturity traded down from an intraweek high of 10.07% to a low of 9.90%, while the 15.09.29 maturity traded at 9.90%. The 15.12.29 maturity traded down from 10.10% to 9.95%.

On the medium end, the 01.03.30 maturity traded down from an intraweek high of 10.10% to a low of 10.05%, while the 15.05.30 maturity traded between 10.23% and 10.17%. The 01.07.30 maturity traded down from 10.25% to 10.15%, while the 15.03.31 maturity traded within the range of 10.26%–10.27%.

Further out the curve, the 01.10.32 maturity traded down to a low of 10.70% after touching an intraweek high of 10.90%, while the 15.12.32 maturity traded at 10.80%. The 01.06.33 traded between 11.08% and 11.00%, while the 01.11.33 maturity traded at 11.00%.

At the long end, the 15.06.34 maturity traded down to a low of 11.15% after touching an intraweek high of 11.31%, while the 15.06.35 maturity traded at 11.26%.

To recap the weekly Treasury Bill auction conducted last Wednesday, it was fully subscribed, raising the entire Rs. 100 billion on offer at the first phase in competitive bidding. The bid to offer ratio stood at 2.15 times.

Rates were seen stabilising. The weighted average yield rates on the 91-day tenor remained unchanged at 8.20% and the 364-day tenor also held steady at 8.52%. However, the 182-day registered a marginal decline of one basis point to 8.24% compared to the previous week. This followed an extended period where rates were seen on an uptrend with the yield on at least one tenor registering an increase over the past six weeks. Further to the T-Bill auction, Rs. 8.44 billion was raised at phase II and accordingly, the aggregate accepted amount of the issuance was Rs. 108,440 billion across both phases.

This comes ahead of the announcement of the details of the next upcoming Treasury Bond auctions, scheduled to be conducted tomorrow (12. The round of auctions will have a total offered amount of Rs. 250 billion across four available maturities.

The auction will be comprised of: Rs. 80 billion from a 1 August 2030 maturity bearing a coupon rate of 10%; Rs. 50 billion from a 15 June 2034 maturity bearing a coupon rate of 10.75%; Rs. 70 billion from a 15 August 2036 maturity bearing a coupon rate of 10.85%; and Rs. 50 billion from a 15 August 2039 maturity bearing a coupon rate of 10.50%. The settlement will be held on 15 May.

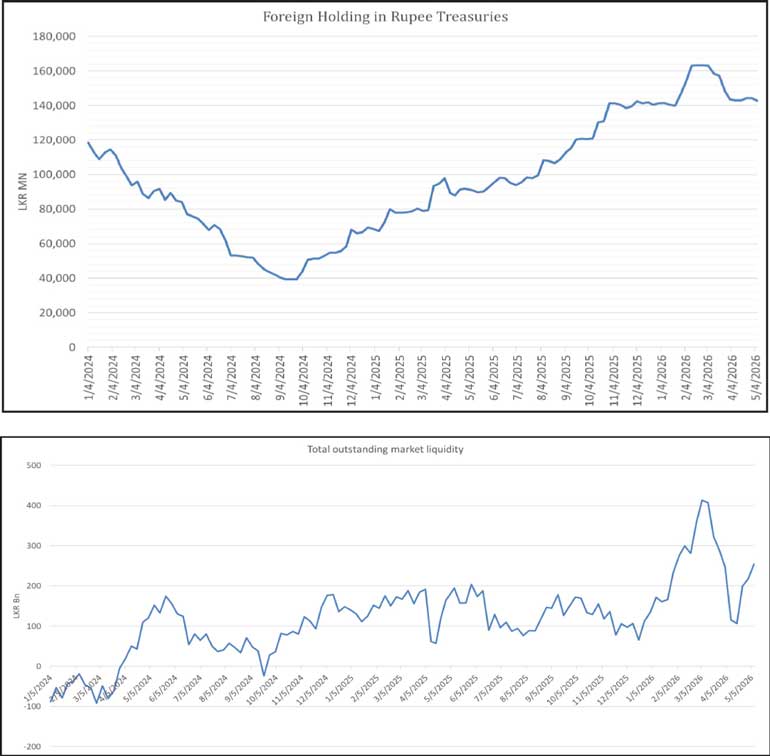

Foreign holdings of rupee-denominated Government securities dropped lower, recording a net outflow of Rs. 1.47 billion last week. Accordingly, total foreign holdings held declined to Rs. 142.73 billion during the week ended 8 May.

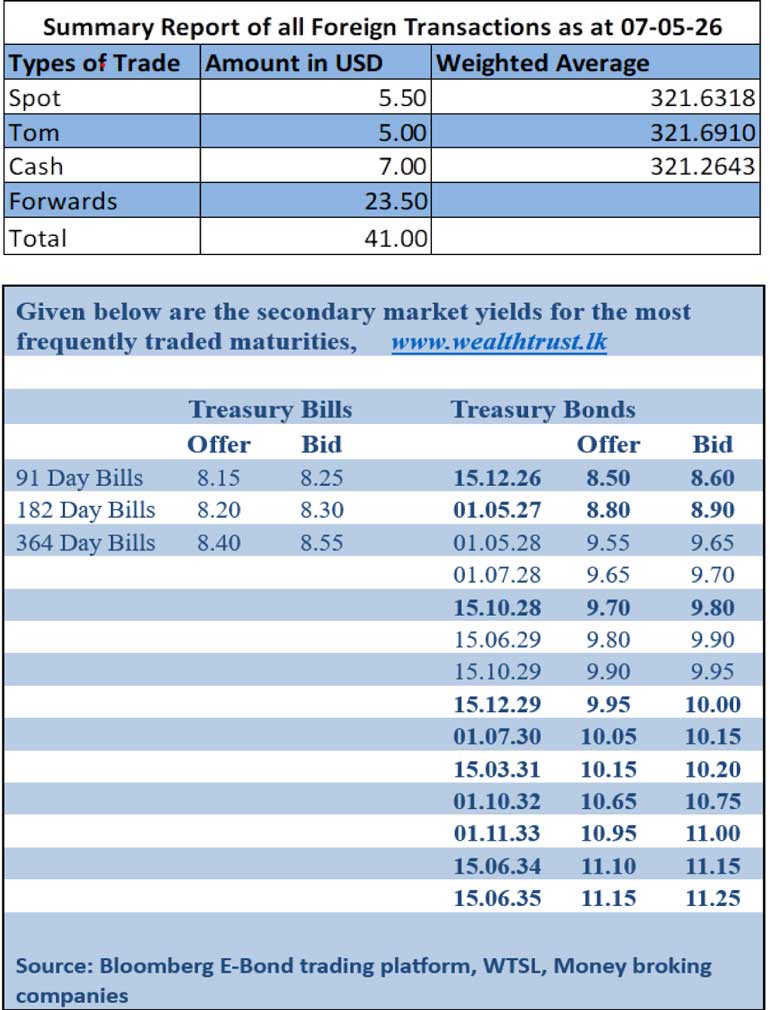

In the money market, the total outstanding liquidity surplus was seen continuing the uptrend and increasing during the week as it was recorded at Rs. 253.66 billion against the previous week’s of Rs. 218.70 billion. The weighted average interest rates on call money and repo stood at 7.76% and 7.80%, respectively, at the close of the week as compared to 7.73% and 7.79%, respectively, the previous week.

Forex market

In the forex market, the USD/LKR rate on spot next contracts was seen closing the week depreciating to Rs. 321.75/321.85 as against the previous week’s spot closing level of Rs. 319.75/320.00. This was subsequent to trading at a high of Rs. 320.00 and a low of Rs. 321.95.

The daily USD/LKR average traded volume for the first four trading days of the week stood at $ 48.28 million.

(References: Public Debt Management Office - Ministry of Finance, Central Bank of Sri Lanka, Bloomberg E-Bond Trading Platform, Money Broking Companies)