Thursday Jul 16, 2026

Thursday Jul 16, 2026

Monday, 9 March 2026 05:39 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

The secondary Bond market last week saw yields initially move sharply higher in response to escalating geopolitical tensions in the Middle East.

The secondary Bond market last week saw yields initially move sharply higher in response to escalating geopolitical tensions in the Middle East.

The early spike reflected a knee-jerk risk reaction, however renewed buying interest at the elevated levels swiftly emerged, supporting a partial recovery. Overall activity and transaction volumes were seen at healthy but subdued levels as participants adopted a more cautious stance amid the ongoing geopolitical uncertainty. In conclusion, secondary Bond market two-way quotes were seen closing the week higher, despite renewed buying interest which kept a cap on rates and drove a partial recovery.

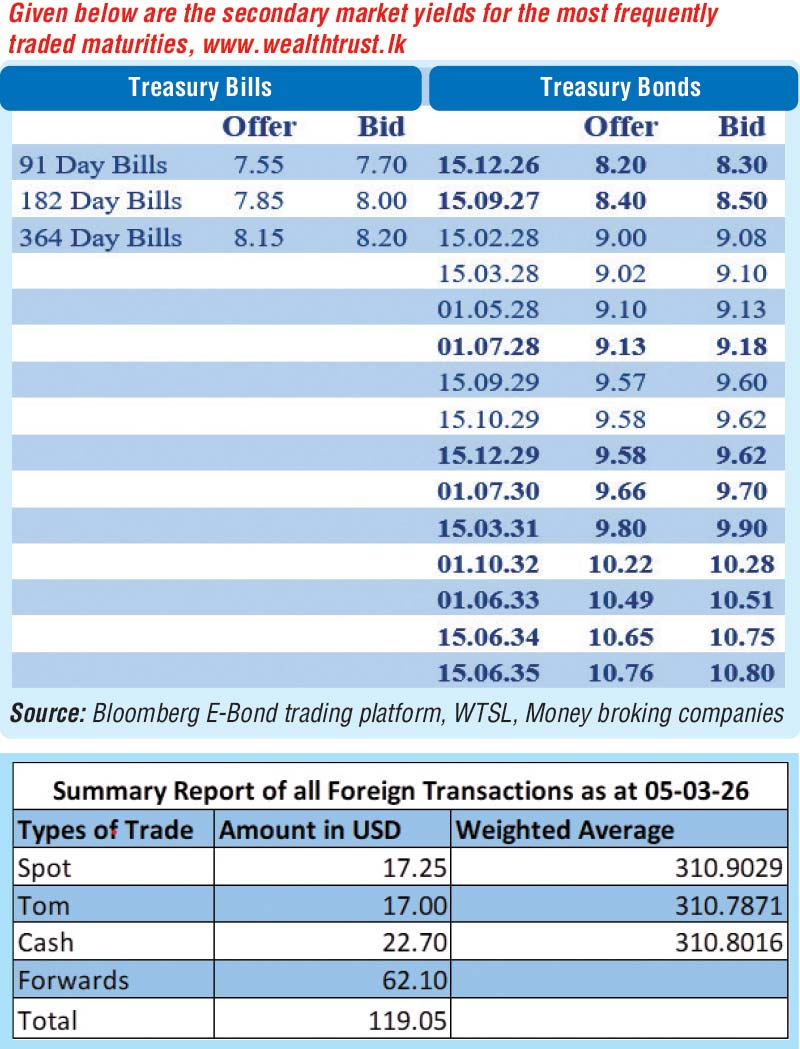

In terms of the Secondary Bond market trade summary: During the week, the 15.12.26 maturity traded at 8.30%, while the 15.01.27 maturity traded at 8.27%.

Moving into the 2028 tenors, the 15.01.28 maturity traded at 8.95%, while the 15.02.28 maturity traded at 9.00%. The 01.05.28 maturity traded at 9.12%, while the 01.07.28 maturity traded within the range of 9.13% to 9.15%. The 15.10.28 maturity traded at 9.20%.

Further along the curve, the 15.06.29 maturity traded down after touching an intraweek high of 9.50% to a low of 9.45%, while the 15.09.29 maturity traded within the range of 9.60% to 9.55%. The 15.10.29 maturity traded at within the range of 9.60%-9.58%, while the 15.12.29 maturity traded within the range of 9.63%-9.59%

On the medium end, the 01.03.30 maturity traded up from an intraweek low of 9.56% to a high of 9.63%, before easing to 9.60%. The 01.07.30 maturity traded at 9.70%. The 15.03.31 maturity traded within the range of 9.80%–9.85%.

Further out the curve, the 15.12.32 maturity traded within the range of 10.28%–10.22%. The 01.06.33 maturity traded down from 10.55% to 10.50%.

At the long end, the 15.06.34 maturity traded within 10.65%–10.72%, while the 15.06.35 maturity traded within 10.74%–10.795%.

The weekly Treasury Bill auction conducted last Wednesday (4) saw yields hold broadly steady, breaking a six-week consecutive streak of decreases prior. Accordingly, the rate on the 91-day Bill remained at 7.63% and the rate on the 182-day Bill stayed static at 7.92%. However, the 364-day Bill saw its yield ease very marginally by one basis points to 8.23%. The auction was heavily undersubscribed at the first phase in competitive bidding. The auction raised only Rs. 47.83 billion, or 39.86% of the total offered amount of Rs. 120 billion. An additional amount of Rs. 7.50 billion was raised from the second phase. Accordingly, the aggregate accepted amount of the issuance was Rs. 55.33 billion.

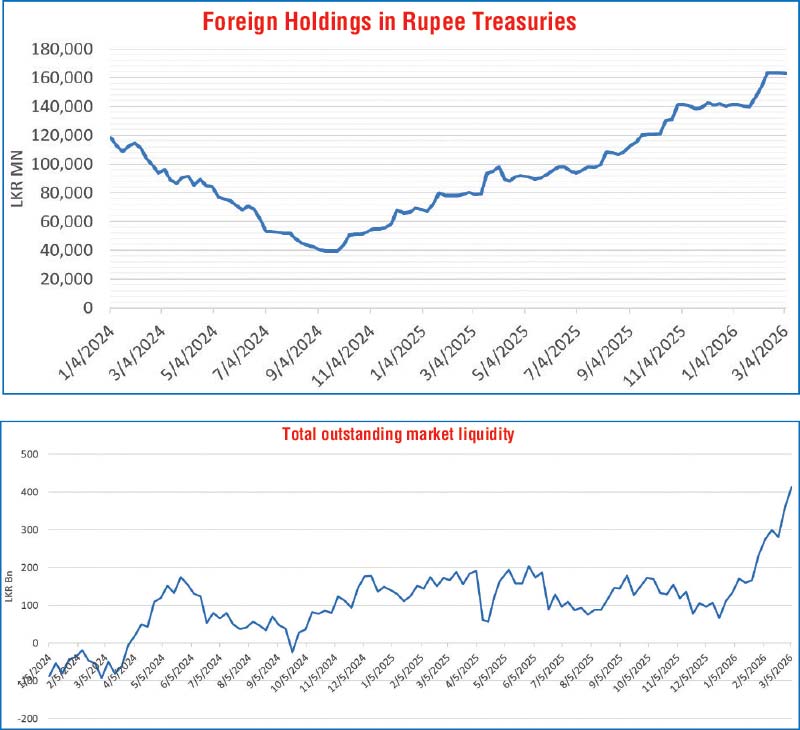

The foreign holdings of rupee-denominated Government securities recorded a marginal net outflow amounting to Rs. 90 million and as a result, total foreign holdings dipped to Rs. 163.15 billion during the week ended 5 March.

In the money market, the total outstanding liquidity surplus in the inter-bank market remained elevated and stood at Rs. 412.92 billion as at the week ending 6 March 2026, up from Rs. 358.76 billion recorded in the previous week. The Domestic Operations Department (DOD) of Central Bank continued to drain out liquidity during the week by way of overnight repo auctions at weighted average yields ranging from 7.60% to 7.51%, as well as 1 week term repo at the rate of 7.72%.

The weighted average interest rates on Call Money and Repo to stood at 7.66% and 7.69%, respectively, at the close of the week ending 3 March against its previous week’s closings of 7.69% and 7.71%.

Forex market

In the Forex market, the USD/LKR rate on spot contracts was seen closing the week depreciating to Rs. 310.80/311.20 as against the previous week’s closing level of Rs. 309.29/309.32. This was subsequent to trading at a high of Rs. 309.70 and a low of Rs. 311.67.

The daily USD/LKR average traded volume for the first four trading days of the week stood at $ 105.57 million.

(References: Public Debt Management Office - Ministry of Finance, Central Bank of Sri Lanka, Bloomberg E-Bond Trading Platform, Money Broking Companies)