Sunday Jun 28, 2026

Sunday Jun 28, 2026

Monday, 23 March 2026 03:11 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

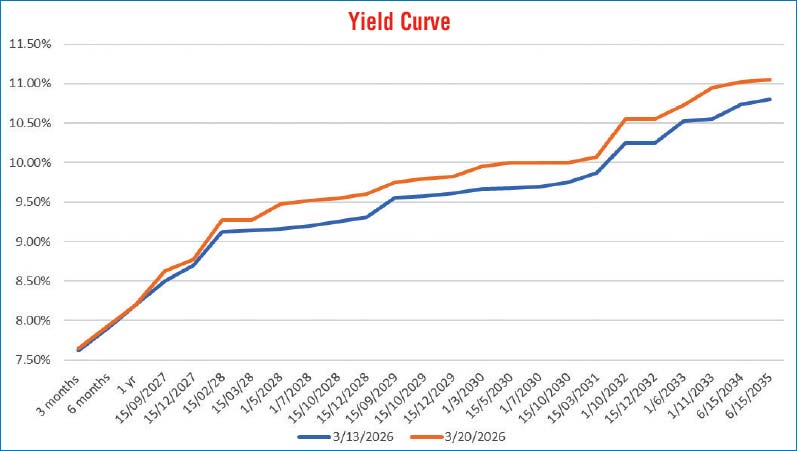

The secondary Bond market last week turned bearish, with yields trending higher across the curve, driven by intensifying external shocks.

The secondary Bond market last week turned bearish, with yields trending higher across the curve, driven by intensifying external shocks.

From a macro perspective, the market was primarily led by geopolitical risk re-pricing, as escalating tensions in the Middle East pushed Brent crude into elevated levels, reinforcing concerns of a renewed global inflation impulse. This was further compounded by hawkish undertones from major global Central Banks, with policymakers signalling that prolonged geopolitical stress could re-anchor inflation expectations higher. In parallel, rising global yields across USTs, Gilts and Bonds, alongside a stronger dollar, tightened global financial conditions—effectively increasing the required risk premium for frontier debt and exerting upward pressure on the local yield curve.

On the domestic front, fuel shortages, power disruption risks, and softer activity expectations amplified the external shock, reinforcing a negative feedback loop between growth concerns and fiscal risk perception. This translated into sustained selling pressure, with market positioning turning defensive, particularly in the belly and long end.

The sharpest re-pricing was observed on Thursday, with yields adjusting upward by 20–30bps on selected tenors. While tactical demand emerged at elevated yield levels, it largely functioned as absorption rather than a shift in sentiment. Although Friday saw a brief relief rally on easing oil-related headlines, renewed escalation risks quickly reversed gains, keeping yields elevated.

Overall, the week was characterised by a pronounced upward shift in the yield curve, with markets structurally re-pricing higher global rates, elevated inflation risks and increased FX drain pressure.

During the week, the 15.05.26 maturity traded within the range of 8.00%–8.10%. The 01.05.27 maturity traded at 8.35% to 8.54%, while the 15.09.27 maturity traded up from an intraweek low of 8.50% to a high of 8.60%.

Moving into the 2028 tenors, the 01.05.28 maturity traded up from an intraweek low of 9.50% to a high of 9.61% whiles the 15.10.28 and 15.12.28 maturities traded up from 9.30% to 9.50%.

Further along the curve, the 15.06.29 maturity traded up from an intraweek low of 9.70% to a high of 9.90%, while the 15.09.29 maturity traded up from 9.70% to 9.90%. The 15.10.29 maturity traded up from 9.90% to 10.05%, while the 15.12.29 maturity traded up from 9.65% to an intraweek high of 10.10%.

On the medium end, the 01.03.30 maturity traded up from an intraweek low of 9.70% to a high of 10.00%, while the 15.03.31 maturity traded up from 9.90% to 10.10%.

Further out the curve, the 01.10.32 maturity traded at 10.30%, while the 15.12.32 maturity traded at 10.45%. The 01.06.33 maturity traded up from 10.70% to 11.00%, while the 01.11.33 maturity traded up from an intraweek low of 10.65% to a high of 11.00%.

At the long end, the 15.06.34 maturity traded up from 10.82% to 11.05%, while the 15.09.34 maturity traded up from 10.82% to 11.12%. The 15.06.35 maturity traded up from an intraweek low of 10.98% to a high of 11.20%.

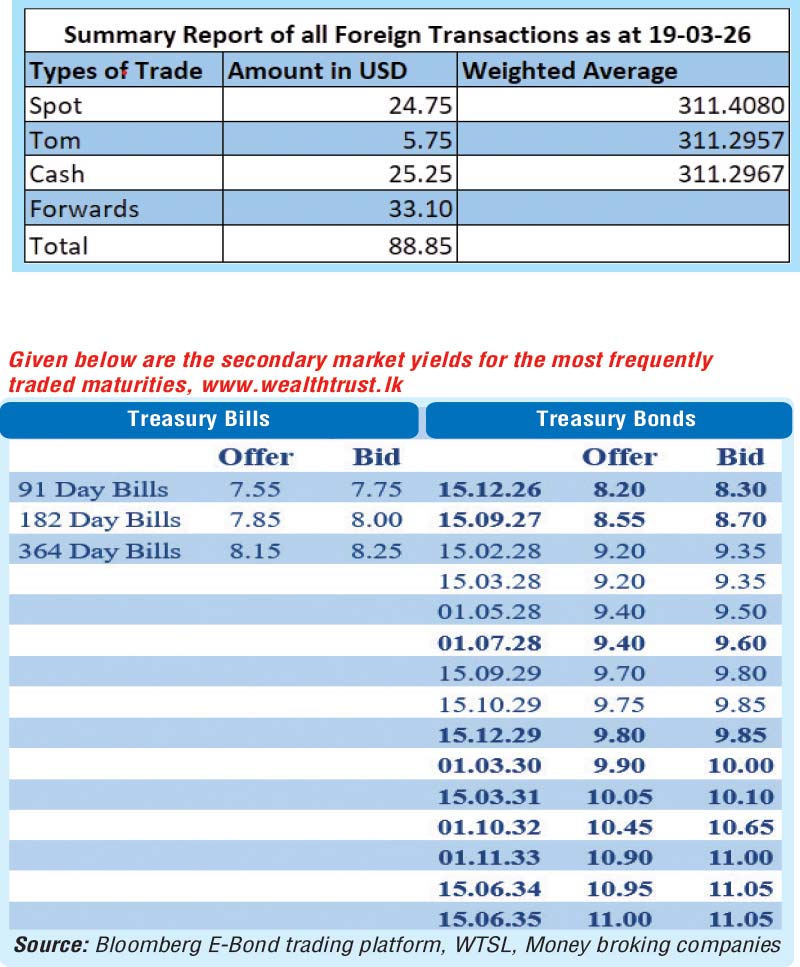

The weekly Treasury Bill auction conducted last Wednesday (18) saw weighted average yields remain unchanged across the board. Accordingly, the rate on the 91-day Bill was recorded at 7.61%, 182-day Bill at 7.91% and the 364-day Bill at 8.23%. This was in stark contrast to the secondary Bond market which has witnessed an uptrend in rates coinciding with the ongoing Middle East conflict. The auction was undersubscribed at the first phase in competitive bidding. Raising only Rs 60.79 billion, or 50.66% of the total offered amount of Rs 120.00 billion. The bid-to-cover ratio stood at 1.73 times.

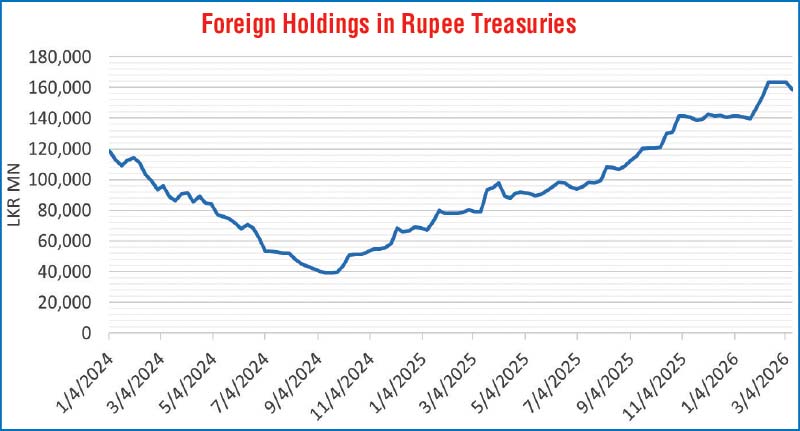

The foreign holdings of rupee-denominated Government securities recorded a net outflow for the third consecutive week amounting to Rs 1.38 billion and as a result, total foreign holdings dipped to Rs. 157.28 billion during the week ended 19 March.

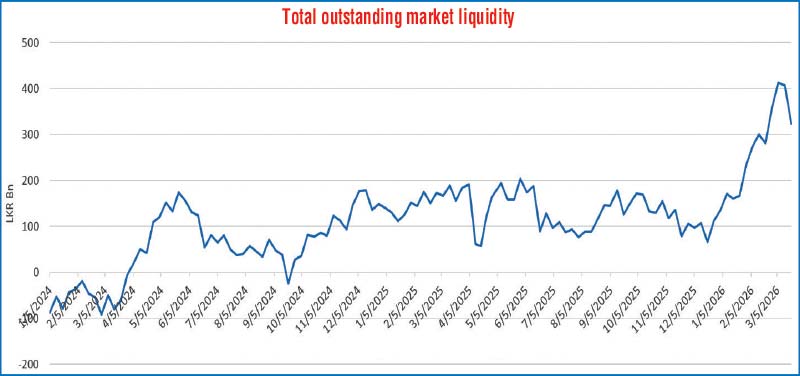

In the money market, the total outstanding liquidity surplus in the inter-bank market remained elevated however dropped to Rs. 323.04 billion as at the week ending 20 March 2026, dipping slightly from Rs. 406.78 billion recorded the previous week. The Domestic Operations Department (DOD) of Central Bank continued to drain out liquidity during the week by way of overnight repo auctions at weighted average yields ranging from 7.46% to 7.59%, as well as one week term repo at the rate of 7.61%.

The weighted average interest rates on Call Money and Repo stood at 7.59% and 7.61%, respectively, at the close of the week ending 20 March against its previous week’s closings of 7.60% and 7.61%.

Forex market

In the Forex market, the USD/LKR rate on spot contracts was seen closing the week depreciating to Rs. 311.85/312.00 as against the previous week’s closing level of Rs. 311.15/311.25. This was subsequent to trading at a high of Rs. 311.20 and a low of Rs. 311.85.

The daily USD/LKR average traded volume for the first four trading days of the week stood at $ 52.29 million.

(References: Public Debt Management Office - Ministry of Finance, Central Bank of Sri Lanka, Bloomberg E-Bond Trading Platform, Money Broking Companies)