Sunday Aug 09, 2026

Sunday Aug 09, 2026

Monday, 1 June 2026 00:05 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

The secondary Bond market last week experienced a volatile yet ultimately bullish week, driven largely by developments in the Middle East, movements in global energy prices, and domestic macroeconomic news.

The week commenced with a strong rally as aggressive buying interest pushed yields sharply lower. Investor sentiment improved on optimism surrounding a potential US-Iran agreement involving a ceasefire and the reopening of the Strait of Hormuz, which contributed to a decline in Brent crude oil prices. Additional support stemmed from the continued appreciation of the Rupee and easing global bond yields.

However, sentiment reversed on Tuesday following monetary policy tightening by a steep 100 basis points, resulting in a bearish bias. This coincided with a Treasury Bill auction which saw rates pick up by well over a 100 basis points as well. Mixed geopolitical developments and crude oil price volatility exerted upward pressure on yields, resulting in higher and wider market two-way quotes amidst subdued activity.

On Wednesday post Rs. 240 billion T-Bond Auction, where rates picked up in line with the monetary tightening, robust buying interest was observed as traders looked to dollar cost average into the new issuances at higher yields. Fresh book building interest was also observed, boosting market activity and volumes.

The week concluded with a strong rally on Friday after reports that the US and Iran have reached a preliminary agreement to extend a ceasefire and ease restrictions on shipping through the Strait of Hormuz subject to finalisation and approval. Further support came from Sri Lanka securing IMF approval for a ‘Super Tranche’ payment under its EFF program in combined reviews and the Treasury reporting a fiscal surplus of Rs. 116.3 billion for 1Q 2026. Consequently, yields declined by approximately 20–35 basis points across selected tenors during Friday.

Further on Friday an additional amount of Rs. 24 billion was raised being the maximum amount offered, out of the total market subscription of Rs. 51.90 billion via the Treasury bonds Direct Issuance Window.

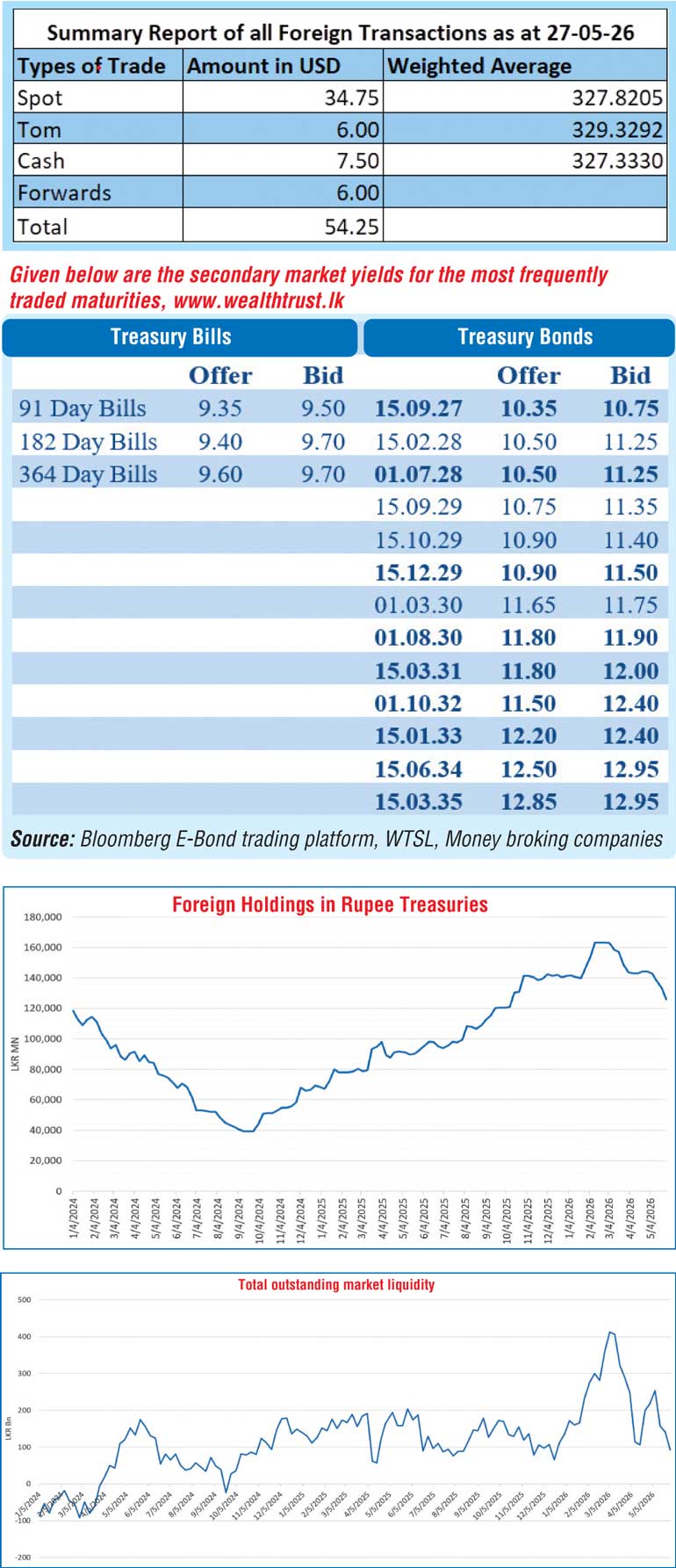

In terms of the secondary Bond market trade summary:

In the secondary Bond market, trading activity at the start of the week was observed prior to the monetary policy rate hike, with yields generally moving lower across the curve. Accordingly, the 15.09.27 maturity traded at the rate of 9.60%. In the 2028 space, the 01.07.28 maturity saw its yield decline from an intraday high of 10.18% to a low of 10.00%, while the 15.02.28 and 15.03.28 maturities traded at the rates of 9.95% and 10.25% respectively. The 15.12.28 maturity traded at the rate of 10.08%. The 15.06.29 and 15.12.29 maturities changed hands at the rates of 10.25%–10.10% and 10.22% respectively. In the 2030 space, the 01.08.30 maturity traded at the rate of 10.30%. The 01.10.32 maturity saw its yield decline sharply from 11.25% to 11.00%. The 01.06.33 maturity traded down the range of 11.30% to 11.20%, while the 15.06.34 and 15.08.36 maturities traded at the rates of 11.35% and 11.45% respectively.

However, following the monetary policy rate hike, the secondary market remained largely subdued on Tuesday with virtually no trades being recorded. However, in line with the policy rate adjustment, two-way quotes shifted higher and were quoted wider across the curve.

Subsequent to the Treasury Bond auction conducted on Wednesday, renewed buying interest emerged. Accordingly, the auctioned bonds namely the 01.08.30 maturities traded down the range of 12.10%–11.82%. The 15.03.35 maturity traded down the ranges of 13.10%-12.75%.

Meanwhile, the foreign holdings of rupee-denominated government securities dropped lower, recording a net outflow for the 4th consecutive week amounting to Rs. 7.33 billion. Accordingly, the total foreign holdings declined further to Rs. 126.10 billion during the week ended 27 May.

In money market, the total outstanding liquidity surplus in the money market was recorded at Rs. 92.15 billion against its previous weeks of Rs. 141.27 billion. The weighted average interest rates on Call Money and Repo stood at 9.10% and 9.13% respectively at the close of the week as compared to 7.92% and 7.97% respectively the previous week.

Forex Market

In the Forex market, the USD/LKR rate on spot contracts was seen closing at Rs. 330/332 as against its previous weeks closing of Rs 329/335 trading from an intraweek high of Rs. 322 to a low of Rs.330.

The daily USD/LKR average traded volume for the first four trading days of the week stood at $ 69.90 million.

(References: Public Debt Management Office – Finance Ministry, Central Bank of Sri Lanka, Bloomberg E-Bond Trading Platform, Money Broking Companies)