Tuesday Aug 04, 2026

Tuesday Aug 04, 2026

Monday, 4 May 2026 06:57 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

The secondary Bond market spent the last week in a clear consolidation phase, with yields holding broadly steady as investors balanced external risks against improving domestic fundamentals.

Sentiment continued to be shaped by persistent geopolitical tensions in the Middle East and elevated crude oil prices. Despite this, robust fiscal performance for January 2026—highlighting a sharp expansion in the primary surplus and near-elimination of the overall budget deficit—provided a strong domestic offset. Concurrently, sustained surplus liquidity, culminating in a CBSL liquidity drain via overnight repo, reinforced stability in short-end rates.

Market activity remained subdued throughout the week, as participants broadly adopted a wait-and-see approach in the absence of clear directional triggers.

By midweek, selective absorptive buying at elevated yield levels, particularly following the positive T-Bill auction outcome, helped cap any upward pressure on rates. Block trades supported volumes.

The prevailing trading pattern was defensive, range-bound positioning, with elevated yields attracting demand but the curve remaining largely unchanged.

In terms of the secondary Bond market trade summary:

During the week, the 01.06.26 and 01.08.26 maturities traded within intra-week highs and lows of 8.30%–8.15% and 8.40%–8.35% respectively.

Moving into the 2028 tenors, the 01.07.28 maturity traded within intraweek highs and lows of 9.75%–9.71%, while the 15.12.28 maturity traded within intraweek highs and lows of 9.85%–9.80%.

Further along the curve, the 15.10.29 maturity traded at 10.00%.

On the medium end, the 01.07.30 and 15.03.31 maturities traded at 10.18%-10.19% and 10.25% respectively.

Further out the curve, the 15.12.32 maturity traded within 10.85%-10.90%, while the 01.06.33 and 01.11.33 maturities traded at 11.00%.

At the long end, the 15.06.34 maturity traded within intraweek highs and lows of 11.21-11.15%, while the 01.07.37 maturity traded at 11.25%.

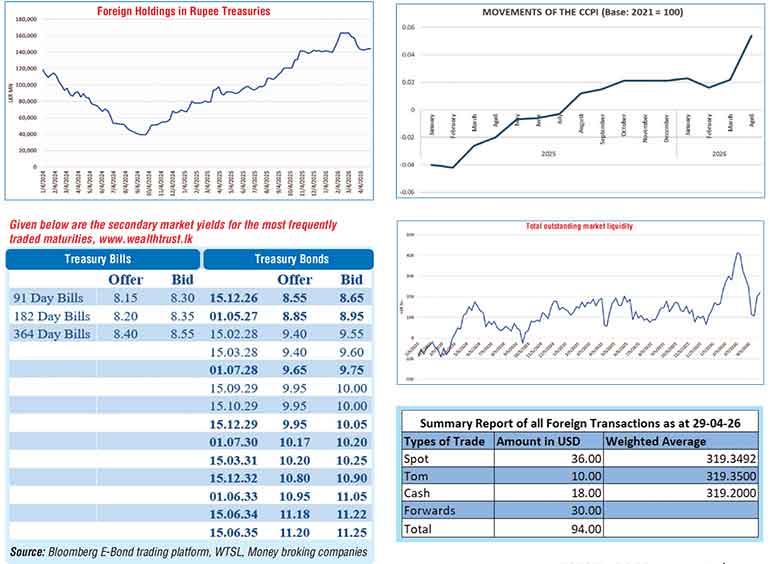

At the weekly Treasury Bill auction conducted last Wednesday, the shorter tenor 91-day Bill attracted strong demand and was issued at a weighted average yield of 8.20%, reflecting a decline of seven basis points compared to the previous week. This marked the first instance in seven weeks where the rate on at least one tenor recorded a decrease. This came despite the 91-day tenor raising above its respective offered amount.

Importantly, the decline in the 91-day yield led to a correction in the T-Bill yield curve, with the shorter tenor moving below the 182-day tenor, reversing the inversion observed in the previous week.

The 182-day Bill increased marginally by two basis points to 8.25%, while the 364-day Bill remained unchanged at 8.52%, with both tenors raising below their respective offered amounts. The auction was undersubscribed, raising Rs. 126.90 billion or 90.64% out of the Rs. 140 billion offered at the first phase. The bid-to-cover ratio of 2.18 times. Further to the T-bill auction held on 29 April 2026, Rs. 10.04 billion was raised at phase II and as a result the aggregate accepted amount of the issuance was Rs. 136.94 billion.

The foreign holdings of rupee-denominated Government securities remained unchanged last week following two consecutive weeks of net inflows preceding that. Accordingly, the total foreign holdings held static at Rs. 144.20 billion during the week ending 29 April.

In terms of inflation data: April CCPI inflation (Base 2021=100) was recorded at +5.40% year-on-year, accelerating from +2.20% in March. The 12-month moving average was recorded at 1.60%. With this print CCPI inflation is now in line with the Central Bank’s targeted inflation level of 5.00% +/- 2.00%.

In the money market, the total outstanding liquidity surplus was seen continuing the uptrend and increasing during the week as it was recorded at Rs. 218.70 billion against its previous weeks of Rs. 199.17 billion. The weighted average interest rates on Call Money and Repo stood at 7.73% and 7.79% respectively at the close of the week as compared to 7.72% and 7.74% respectively the previous week.

Forex market

In the forex market, the USD/LKR rate on spot next contracts was seen closing the week depreciating to Rs. 319.75/320.00 as against the previous week’s spot closing level of Rs. 318.40/318.70. This was subsequent to trading at a high of Rs. 317.75 and a low of Rs. 320.00.

The daily USD/LKR average traded volume for the first four trading days of the week stood at $ 59.20 million.

(References: Public Debt Management Office - Ministry of Finance, Central Bank of Sri Lanka, Bloomberg E-Bond Trading Platform, Money Broking Companies)