Thursday Aug 06, 2026

Thursday Aug 06, 2026

Monday, 20 April 2026 04:08 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

The secondary Bond market witnessed mixed yet broadly positive trend during the holiday-shortened week, influenced by evolving geopolitical developments and shifting investor sentiment.

The secondary Bond market witnessed mixed yet broadly positive trend during the holiday-shortened week, influenced by evolving geopolitical developments and shifting investor sentiment.

At the start of the week, yields remained broadly steady with muted activity, reflecting a cautious stance among market participants. However, sentiment improved significantly on Thursday, leading to a decline in yields across the curve. This was driven by optimism surrounding a potential diplomatic resolution to US–Iran tensions and anticipated de-escalation in the Middle East. The most notable yield compression was observed in the liquid 2029–2034 tenors. Early session volumes were strong, although profit-taking later led to a partial reversal of gains.

By Friday, yields stabilised across most maturities, with some tenors edging slightly higher as investors adopted a defensive stance ahead of further geopolitical clarity. While activity levels were subdued, transaction volumes remained healthy, supported by several block trades.

On a week-on-week basis, yields closed steady to marginally lower across the curve, underpinned by improved sentiment and moderating oil prices.

In terms of the secondary Bond market trade summary:

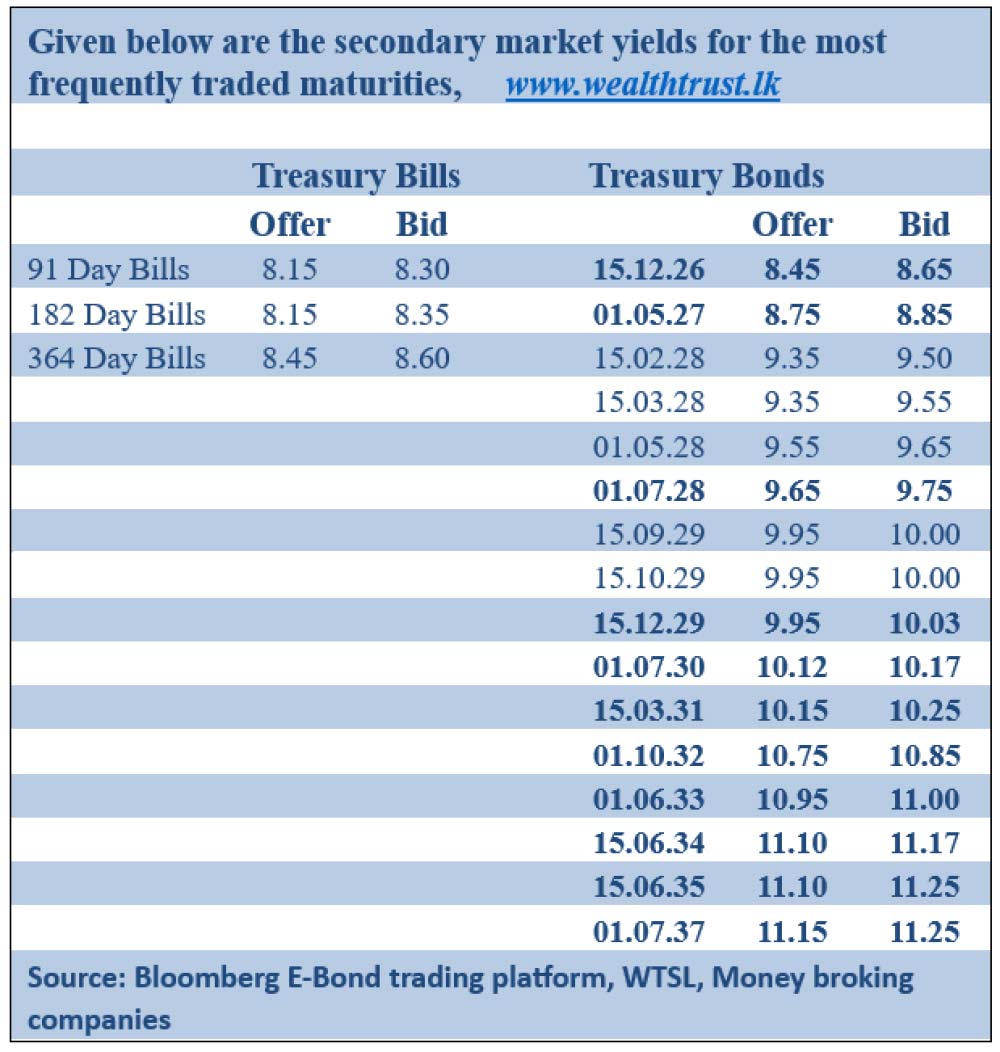

During the week, the 01.05.27 maturity traded within intraweek highs and lows of 8.83%–8.75%.

Moving into the 2028 tenors, the 01.05.28 maturity traded at 9.60%, while the 01.07.28 maturity traded at 9.70%. The 15.10.28 maturity traded at 9.75%.

Further along the curve, the 15.06.29 maturity traded at 9.90%, while the 15.09.29 maturity traded within intraweek highs and lows of 9.98%–9.93%. The 15.12.29 maturity traded within intraweek highs and lows of 10.05%–10.00%.

On the medium end, the 01.03.30 maturity traded within intraweek highs and lows of 10.05%–9.95%, while the 01.07.30 maturity traded within intraweek highs and lows of 10.15%–10.10%.

Further out the curve, the 01.06.33 maturity traded within intraweek highs and lows of 11.00%–10.95%, while the 01.11.33 maturity traded at 11.00%. At the long end, the 15.06.34 maturity traded within intraweek highs and lows of 11.15%–11.09%.

The weekly Treasury bill auction conducted last Wednesday extended the upward trajectory and saw weighted average yields increase across the board for the fourth consecutive week.

Accordingly, the yield on the 91-day Bill rose by 20 basis points to 8.15%, the 182-day bill increased by 08 basis points to 8.22%, while the 364-day Bill saw an uptick of 07 basis points to 8.52%. The auction was undersubscribed at the first phase in competitive bidding, raising only Rs. 58.52 billion or 65.02% out of the Rs. 90 billion total offered amount. The bid-to-cover ratio stood at 1.51 times. Notably, further to the T-bill auction, Rs. 25.52 billion was raised at the phase II of the auction boosting the aggregate accepted amount of the issuance was Rs. 84.04 billion.

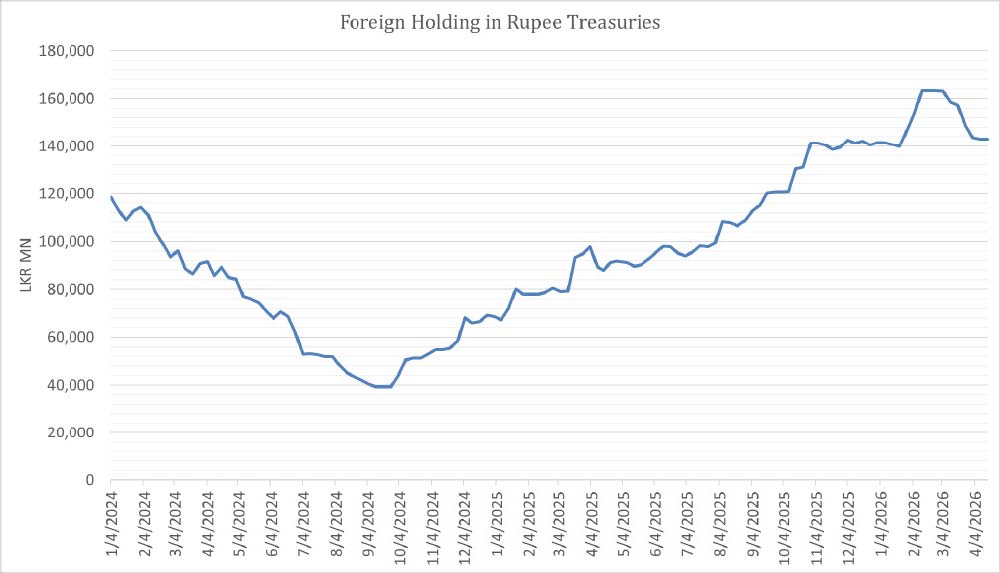

Meanwhile, the foreign holdings of rupee-denominated Government securities recorded a net inflow for the first time in seven weeks, amounting to a marginal Rs. 2 million and as a result, total foreign holdings held broadly steady at Rs. 142.92 billion during the week ended 17 April.

In the money market, the total outstanding liquidity surplus in the inter-bank market remained mostly unchanged at Rs. 106.32 billion as at the week ending 17 April 2026, from Rs. 114.60 billion recorded the previous week.

The weighted average interest rates on Call Money and Repo stood at 7.67% and 7.70%, respectively, at the close of the week ending 10th April as against its previous weeks closings of 7.63% and 7.66%.

Forex market

In the forex market, the USD/LKR rate on spot contracts was seen closing the week depreciating to Rs. 316.55/316.70 as against the previous week’s closing level of Rs. 315.50/315.60. This was subsequent to trading at a high of Rs. 315.55 and a low of Rs. 316.60.

The daily USD/LKR average traded volume for the first four trading days of the week stood at $ 88.38 million.

(References: Public Debt Management Office - Ministry of Finance, Central Bank of Sri Lanka, Bloomberg E-Bond Trading Platform, Money Broking Companies)