Saturday Jun 13, 2026

Saturday Jun 13, 2026

Monday, 8 June 2026 05:15 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

THE secondary Bond market started off and remained bearish throughout last week, with yields trending higher across the curve amid persistent selling pressure and cautious investor sentiment. Market activity was generally subdued, although transaction volumes were supported by selective block trades.

THE secondary Bond market started off and remained bearish throughout last week, with yields trending higher across the curve amid persistent selling pressure and cautious investor sentiment. Market activity was generally subdued, although transaction volumes were supported by selective block trades.

Sentiment was weighed down by both domestic and external factors. Domestically, investors continued to assess the impact of the recent 100 basis point policy rate hike, while tighter liquidity conditions and rising money market rates contributed to higher funding costs. In addition, Treasury Bill yields continued to rise, with market participants re-pricing interest rate expectations after the latest auction recorded a third consecutive weekly increase in yields. The increase in T-Bill yields since the policy rate hike has significantly exceeded the magnitude of the policy adjustment. Domestic inflation statistics which have already shown a notable rise were further pressured by a fuel price revision delivered on the 30 May ranging between Rs. 15-25.

Externally, escalating geopolitical tensions in the Middle East and uncertainty surrounding US-Iran negotiations kept Brent crude oil prices elevated and volatile, raising concerns over further inflation and external sector risks. Rising global bond yields and a broader risk-off environment further pressured the market. As a result, yields trended higher and secondary bond market two-way quotes closed the week up.

In terms of the Secondary Bond market trade summary:

The 15.02.28 and 15.03.28 maturities changed hands at the rate of 11.95% each. The 01.05.28 maturity traded up from an intraweek low of 11.75% to a high of 12%, while the 01.07.28 maturity traded up the range of 11.50%–12.00%.

Moving into the 2029 segment, the 15.10.29 and 15.12.29 maturities changed hands at the rates of 12.10% and 12.00% respectively.

In the 2030 space, the 01.03.30 maturity traded at the rate of 12.10%, while the 01.07.30 maturity changed hands at the rate of 12.15%. The 01.08.30 maturity traded up from an intraweek low of 11.95% to a high of 12.30%.

The 15.01.33 maturity traded up the range of 12.30% to 12.45%, while the 01.06.33 maturity changed hands at the rate of 12.75%.

The 15.06.34 maturity traded up from an intraweek low of 13.12% to a high of 13.15%.

Further along the curve, the 15.03.35 maturity traded up from an intraweek low of 12.95% to a high of 13.25%, while the 15.06.35 maturity changed hands at the rate of 13.30%. At the longer end, the 15.08.36 maturity traded within the range of 13.28%–13.29%.

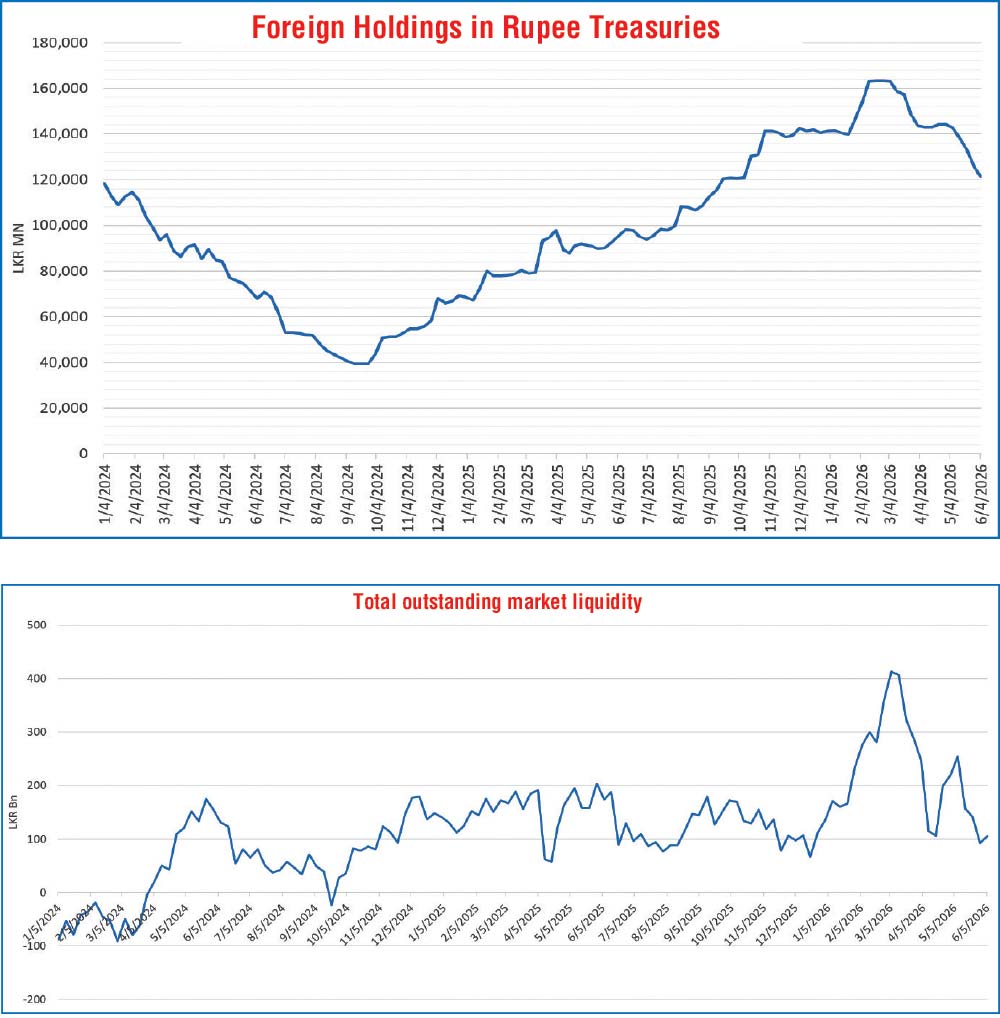

The foreign holdings of rupee-denominated Government securities dropped lower, recording a net outflow for the 5th consecutive week amounting to Rs. 4.77 billion. Accordingly, the total foreign holdings declined further to Rs. 121.33 billion during the week ended 4 June, the lowest level in 37 weeks-since mid-October 2025.

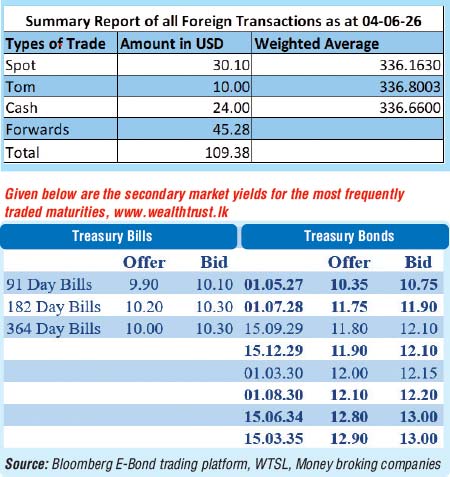

In money Market, the total outstanding liquidity surplus in the money market was recorded at Rs. 105.04 billion against the previous week’s Rs. 92.15 billion. The weighted average interest rates on Call Money and Repo stood at 9.16% and 9.20% respectively at the close of the week as compared to 9.10% and 9.13% respectively the previous week.

Forex market

In the forex market, the USD/LKR rate on spot contracts was seen closing at Rs 335.75/336.25 as against its previous weeks closing of Rs. 330/322

trading from an intraweek high of Rs. 330.75 to a low of

Rs. 337.10.

The daily USD/LKR average traded volume for the first four trading days of the week stood at $ 85.26 million.

(References: Public Debt Management Office - Ministry of Finance, Central Bank of Sri Lanka, Bloomberg E-Bond Trading Platform, Money Broking Companies)