Wednesday Aug 05, 2026

Wednesday Aug 05, 2026

Monday, 15 June 2026 05:42 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

The secondary Bond market began last week on a cautious note, with subdued activity as investors navigated heightened geopolitical tensions in the Middle East and a busy primary issuance calendar featuring back-to-back Treasury Bill and Bond auctions. Yields drifted higher early in the week amid risk-off sentiment, driven by elevated and volatile crude oil prices.

The secondary Bond market began last week on a cautious note, with subdued activity as investors navigated heightened geopolitical tensions in the Middle East and a busy primary issuance calendar featuring back-to-back Treasury Bill and Bond auctions. Yields drifted higher early in the week amid risk-off sentiment, driven by elevated and volatile crude oil prices.

Market sentiment improved mid-week following a constructive outcome at the Treasury Bill auction and the CBSL’s decision to shorten exporters’ FX conversion timelines, which helped stabilise the currency and in turn yields.

While renewed concerns over escalating US-Iran tensions briefly pressured the market on Thursday ahead of the Bond auction and rates spiked, post auction saw renewed buying interest push rates back lower sparking a recovery.

Friday proved to be the defining session of the week.

Reports of a potential US-Iran peace agreement triggered a sharp decline in Brent crude prices toward $ 86/bbl, significantly improving global risk sentiment. The prospect of easing external pressures prompted a strong broad-based rally across the curve, with yields declining sharply amid aggressive buying interest. Activity and transaction volumes also rose markedly. In conclusion, despite a week characterised by volatility, at the close secondary Bond market two-way quotes closed firmly lower on the back of risk-on enthusiasm.

In terms of the secondary Bond market trade summary, the 15.09.27 maturity traded down from an intraweek high of 11.00% to a low of 10.75%.

In the 2028 space, the 15.02.28 maturity traded down from an intraweek high of 11.75% to a low of 11.40%, while the 15.03.28 maturity changed hands at the rate of 11.45%. The 01.05.28 maturity traded down from an intraweek high of 11.92% to a low of 11.70%.

Moving into the 2029 segment, the 15.09.29 maturity traded down from an intraweek high of 12.50% to a low of 11.80%.

In the 2030 space, the 01.03.30 maturity hit an intraweek high of 12.50% to before recovering to trade at a low of 12.00%. Similarly, the 15.05.30 maturity traded down from 12.50% to 11.92% and the 01.08.30 maturity traded down from 12.25% to 11.93%.

The 15.12.32 maturity traded down from an intraweek high of 12.60% to a low of 12.30%. The 01.06.33 and 01.11.33 maturities changed hands at the rate of 13.00% each during the bearish phase of the market.

At the longer end, the 15.03.35 maturity traded down from an intraweek high of 13.25% to a low of 12.88%.

At the weekly Treasury Bill auction, yields increased for the fourth consecutive week, albeit at a slower pace, indicating moderation in the upward trend. The weighted average yield rate on the 91-day Bill yield rose by 25 bps to 10.09%, the 182-day Bill yield increased by 26 bps to 10.27%. Interestingly the 364-day Bill yield gained 14 bps to 10.16%, with the 6-month yield moving above the 1-year rate. Hitting the highest yield levels since September 2024. The auction raised only 51.25% or Rs. 71.7 billion against an offer of Rs. 140.0 billion, with most accepted bids concentrated in the 3-month tenor.

Subsequently Thursday’s Treasury bond auction delivered mixed results, with the auction failing to raise the Rs. 150 billion total offered amount across both phases, and seeing all bids for the longest tenor rejected. The auction raised only 61.70% or Rs. 92.55 billion across both phases. However, despite the prevailing bearish sentiment driven by Middle Eastern tensions and elevated crude oil prices at the time, yields came in below market expectations - well below pre-auction traded levels and quotes. The bid-to-offer ratio stood at 1.97x.

Maturity-wise results: 15.05.30 issue at 11.65%, below prevailing market levels as the same maturity was observed trading at 12.50% pre auction, but failed to raise the maturity wise offered amount; 15.12.32 issued at 12.69%, also came in below market expectations, However, the maturity also failed to raise the maturity-wise offered amount; 01.07.37 issue saw all bids rejected.

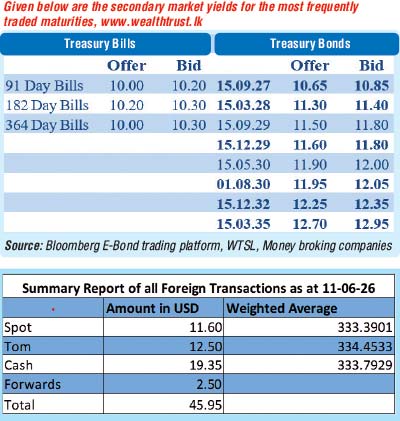

The foreign holdings of rupee-denominated Government securities increased marginally, recording a net inflow breaking a streak of 5th consecutive weeks of outflows. Accordingly, the total foreign holdings increased by Rs. 13 million to Rs. 121.34 billion during the week ended 11 June.

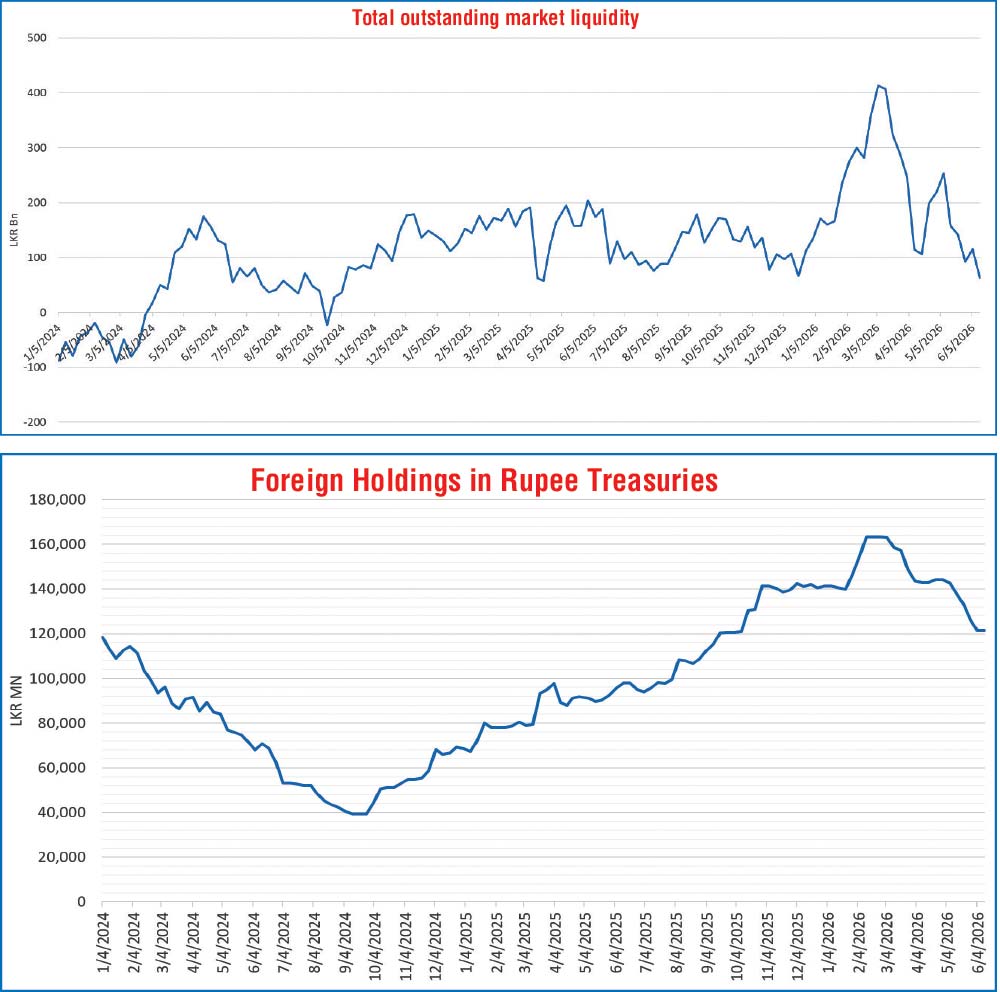

In the money market, the total outstanding liquidity surplus was recorded at Rs. 62.57 billion against the previous week’s Rs. 115.04 billion. The weighted average interest rates on Call Money and Repo stood at 9.19% and 9.23% respectively at the close of the week as compared to 9.16% and 9.20% respectively the previous week.

Forex market

In the forex market, the USD/LKR rate on spot contracts was seen closing at Rs 335.50/336.00 as against its previous weeks closing of Rs 335.75/336.25 trading from an intraweek high of Rs. 328.00 to a low of Rs.338.50.

The daily USD/LKR average traded volume for the first four trading days of the week stood at $ 58.88 million.

(References: Public Debt Management Office - Ministry of Finance, Central Bank of Sri Lanka, Bloomberg E-Bond Trading Platform, Money Broking Companies)