Friday Aug 07, 2026

Friday Aug 07, 2026

Wednesday, 28 January 2026 00:16 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

The secondary Bond market today remained largely at a standstill, as market participants continued to adopt a defensive stance ahead of an action-packed week. Key events include the first Monetary Policy Announcement of 2026 and the weekly Treasury Bill auction, both scheduled for today.

The announcement for the inaugural Monetary Policy Review for 2026 is due to be announced today at 7.30 am.

To recap: At the 06th and Final Monetary Policy Review for 2025 announced last November, the Central Bank of Sri Lanka (CBSL) decided to hold the Overnight Policy Rate at 7.75%. This marked the third consecutive monetary policy decision to keep rates on hold.

The Standing Deposit Facility Rate (SDFR) and Standing Lending Facility Rate (SLFR), which are linked to OPR with pre-determined margins of ± 50 basis points, also remained unchanged at 7.25% and 8.25%, respectively. The statutory reserve rate was left unchanged at 2.00%.

It is widely anticipated that there will be a no change outcome at the Monetary Policy Review No. 01 for 2026. In an article titled “Sri Lanka central bank likely to hold rates ahead of IMF review”, Reuters reported that Sri Lanka’s Central Bank is expected to keep its key policy rate unchanged at 7.75% at its 28 January announcement, as an IMF delegation reviews progress under the country’s $ 2.9 billion assistance program.

Today’s scheduled weekly Treasury Bill auction will have on offer a total amount of Rs. 125 billion. The auction will be comprising of Rs. 35 billion in 91-day Bills, Rs. 70 billion in 182-day Bills, and Rs. 20 billion in 364-day Bills. The offered amount is below the maturing volume, which is estimated at around Rs. 132.82 billion.

At the weekly Treasury Bill auction held last Wednesday (21), weighted average yields declined across all maturities, reversing the upward trend seen over the previous four consecutive weeks. The weighted average yield on the 91-day Bill eased by 2 basis points to 7.93%, the 182-day Bill recorded a sharper decline of 8 basis points to 8.36% and the 364-day Bill edged down marginally by 1 basis point to 8.47%.

Despite the auction being marginally undersubscribed at the first phase, strong investor appetite was witnessed, with total bids reaching 2.81 times the offered volume. The Public Debt Management Office raised Rs. 112.48 billion, representing 89.99% of the Rs. 125 billion on offer during competitive bidding. Subsequently, strong demand was also observed at Phase 2, where Rs. 25.02 billion was raised across all three tenors out of a total market subscription of Rs. 116.41 billion, reflecting a heavily oversubscribed Phase 2 issuance. As a result, the total accepted amount across both phases reached Rs. 137.50 billion.

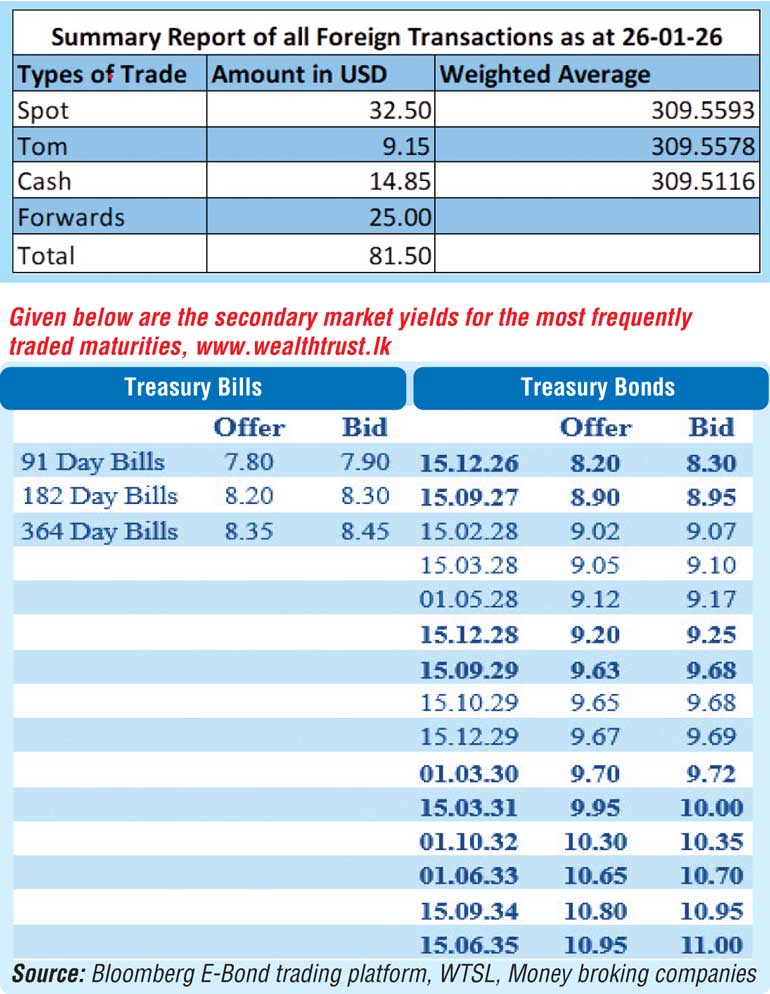

In secondary Bonds market, limited trades were observed: the 15.05.26 maturity traded within the range of 8.27%-8.20%. The 01.08.26 maturity traded at the rate of 8.25%. The 01.05.27 maturity traded at the rate of 8.86%. The 15.03.28 maturity traded at the rate of 9.08%. The 01.05.28 and 01.07.28 maturities were seen trading at the rates of 9.15% and 9.17%. The 15.12.29 maturity traded up the range of 9.68%-9.69%. The 01.03.30 maturity traded at the rate of 9.71%.

The total secondary market Treasury Bond/Bill transacted volume for 26 January was Rs. 10.34 billion.

In money markets, the weighted average rates on overnight call money and Repo stood at 7.71% and 7.73% respectively whiles the net liquidity surplus was recorded at Rs. 163.50 billion.

Forex market

In the forex market, the USD/LKR rate on spot contracts were seen closing the day depreciating to Rs. 309.65/309.75 as against its previous day’s closing level of Rs. 309.50/309.60.

The total USD/LKR traded volume for 26th January 2026 was $ 81.50 million.

(References: Central Bank of Sri Lanka, Bloomberg E-Bond trading platform, Money broking companies)