Thursday Jul 16, 2026

Thursday Jul 16, 2026

Wednesday, 15 July 2026 00:04 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

The secondary Bond market yesterday saw activity pick up from the previous session, which was at a virtual standstill due to the Treasury Bond auctions.

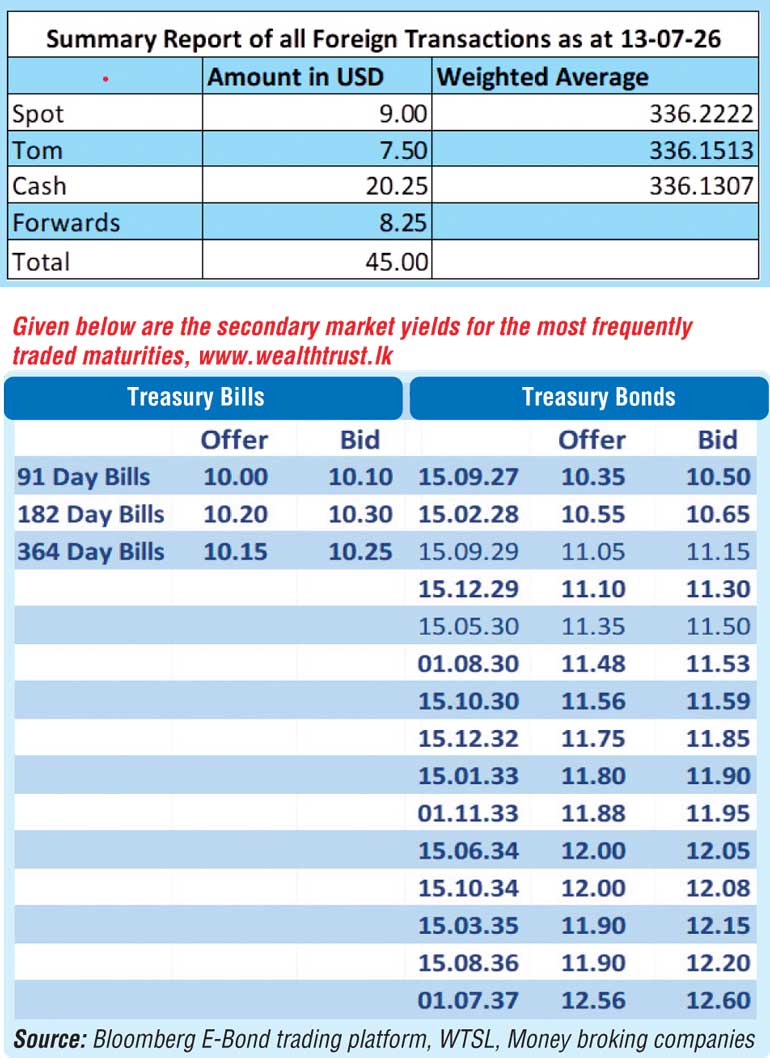

Secondary market yields were seen adjusting to the Treasury Bond auction outcome from the previous day. Yields were seen compressing from the morning’s opening quotes on the back of steady institutional buying interest as renewed demand kicked in at the elevated levels.

The 01.08.30 and 15.10.30 maturities traded at the rates of 11.50% and down the range of 11.60%-11.57% respectively. The 01.11.33, 15.06.34 and 15.10.34 auction maturities traded at the rate and down the range of 11.90%, 12.00% and 12.05%-12.00% respectively. The longer tenor 01.07.37 maturity traded down the range of 12.62%-12.58%.

The Treasury Bill auction scheduled for today, will have a total amount of Rs. 120 billion on offer. This will comprise of Rs. 55 billion offered on the 91-day maturity, Rs. 35 billion on the 182-day maturity and Rs. 30 billion on the 364-day maturity. This is below the maturity corresponding to the scheduled auction, which is estimated to be approximately Rs. 147.72 billion.

To recap: At the weekly Treasury Bill auction last week, the weighted average yields held broadly steady, breaking a two-week streak of across-the-board increases prior. Accordingly, the rate on the 91-day tenor reduced by 2 basis points to 10.21%, the 182-day tenor remained unchanged at 10.30% and the 364-day tenor edged up marginally by 1 basis point to 10.21%.

The auction successfully raised the full Rs. 100 billion offered at the first phase of competitive bidding. However, the bulk of the quantity raised was from the 91-day tenor, which raised more than its offered amount, while the other two tenors raised the same or less than their respective offered amounts. Total bids received amounted to 2.30 times of the offered amount up from 1.66 times the week before.

In the money market, the net liquidity surplus stood at Rs. 151.99 billion yesterday. Of this, Rs. 101.99 billion was absorbed via the Central Bank’s Standing Deposit Facility (SDF) at 8.25%, while a further Rs. 50 billion was mopped up through an overnight Repo auction conducted by the Domestic Operations Department (DOD) at a weighted average rate of 8.69%. Notably, bids received amounted to Rs. 71 billion against the Rs. 50 billion offered.

The weighted average rates on overnight call money and Repos were recorded at 8.96% and 9.00% respectively.

Forex market

The USD/LKR rate on spot contracts was seen closing at the day at Rs. 336.30/336.40, slipping against its previous day’s close of Rs. 336/336.25.

The total USD/LKR traded volume for 13 July was $ 45 million.

(References: Public Debt Management Office - Ministry of Finance, Central Bank of Sri Lanka, Bloomberg E-Bond Trading Platform, Money Broking Companies)