The secondary Bond market began last week with yields initially edging up further, as residual profit-taking pressure from the prior week lingered. Market activity remained subdued during the early part of the week, with participants adopting a cautious, wait-and-see stance ahead of the back-to-back Treasury Bill and Bond auctions, despite liquidity conditions remaining elevated.

However, market momentum quickly shifted. Mid-week sentiment turned more constructive following the positive outcome at the weekly Treasury Bill auction, alongside a further increase in money market liquidity from already elevated levels, supporting a recovery. Market direction changed decisively on Thursday, as the Treasury Bond auction delivered a bullish outcome, triggering a sharp rally in the secondary market. Aggressive buying interest, underpinned by liquidity levels reaching 22-year highs, drove yields lower across the curve. By week’s end, yields consolidated at lower levels, with secondary market quotes closing lower on a week-on-week basis.

In terms of the Secondary Bond market trade summary:

During the week, the 01.08.26 maturity traded within the range of 8.10%–8.00%, while the 15.01.27 maturity traded down from an intra-week high of 8.25% to a low of 8.20%.

Moving into the 2028 tenors, the 15.02.28 maturity traded down from 9.00% to 8.98%, while the 01.05.28 maturity traded at 9.05% to 9.02%. The 15.10.28 maturity initially traded up to an intraweek high of 9.19% before easing back to 9.15%. The 15.12.28 maturity traded at 9.19%.

Further along the curve, the 15.06.29 maturity traded down from 9.40% to 9.35%. The 15.09.29 maturity traded down from 9.45% to 9.40%, while the 15.10.29 maturity traded down from an intraweek high of 9.54% to a low of 9.40%. The 15.12.29 maturity traded down from 9.50% to 9.42%.

On the medium end, the 01.03.30 maturity traded down from 9.55% to a low of 9.48%. The 15.03.31 maturity traded down from 9.75% to 9.70%.

Further out the curve, the 01.10.32 maturity traded down from an intraweek high of 10.22% to a low of 10.10%, while the 15.12.32 maturity traded down from 10.15% to 10.10%. The 01.06.33 maturity traded down from an intraweek high of 10.47% to a low of 10.35%, while the 01.11.33 maturity traded at 10.40%.

At the long end, the 15.06.34 maturity traded down from 10.80% to 10.62%, while the 15.06.35 maturity traded down from an intraweek high of 10.85% to a low of 10.70%.

The weekly Treasury Bill auction held last Wednesday (25), saw yields continue their downward trajectory, with weighted average rates declining across all maturities for the sixth consecutive week. Accordingly, the rate on the 91-day Bill declined by 3 basis points to 7.63%, the rate on the 182-day Bill dropping by 7 basis points to 7.92% and the 364-day Bill saw its yield ease more by 3 basis points to 8.24%.

This was followed by a Treasury Bond auction on Thursday (26), with the PDMO raising the full Rs. 140 billion on offer across three available maturities. Demand was strong, reflected by a bid-to-cover ratio of 2.79x, supported by high system liquidity, compressed money market rates, and the prior day’s decline in T-Bill yields. All maturities were fully subscribed at the first phase- in competitive bidding, with weighted average yields coming in below or in line with market expectations.

Maturity-wise breakdown:

1)

01.03.30: Issued at a weighted average yield of 9.50%, came in below pre-auction market quotes of 9.52% / 9.55%

2)

15.06.34: Issued at WAYR of 10.70%, marginally below the pre-auction quote of 10.70% / 10.75%.

3)

01.07.37: Issued at a weighted average yield of 10.88%, representing only a narrow term premium over the actively traded 15.06.35 maturity which was quoted at 10.77% / 10.80% pre-auction.

In terms of inflation data: February CCPI inflation (Base 2021=100) was recorded at +1.60% year-on-year, decelerating from +2.3% in January. Inflation continues to remain moderate and below the Central Bank’s medium-term target of 5% and even below the lower bound of the target range of 3%. This print was also well below expectations of both Bloomberg’s forecast of 2.10% and a consensus estimate of 2.50%.

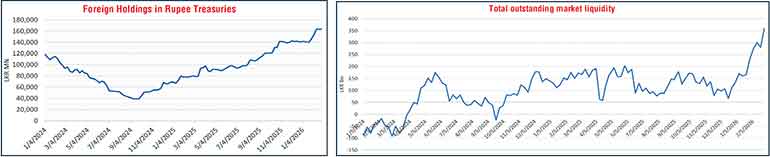

The foreign holdings of rupee-denominated Government securities remained static following four consecutive weeks of net inflows prior. As a result, total foreign holdings remained at Rs. 163.41 billion during the week ended 26 February.

In the money market, the total outstanding liquidity surplus in the inter-bank market stood at Rs. 358.76 billion as at the week ending 27 February 2026, up from Rs. 280.75 billion recorded in the previous week. The Domestic Operations Department (DOD) of the Central Bank continued to drain out liquidity during the week by way of overnight repo auctions at weighted average yields ranging from 7.62% to 7.64%, as well as 1 week term repo at the rate of 7.74%.

The weighted average interest rates on Call Money and Repo to stood at 7.69% and 7.71%, respectively, at the close of the week ending 27 February against its previous weeks closings of 7.67% and 7.69%.

Forex market

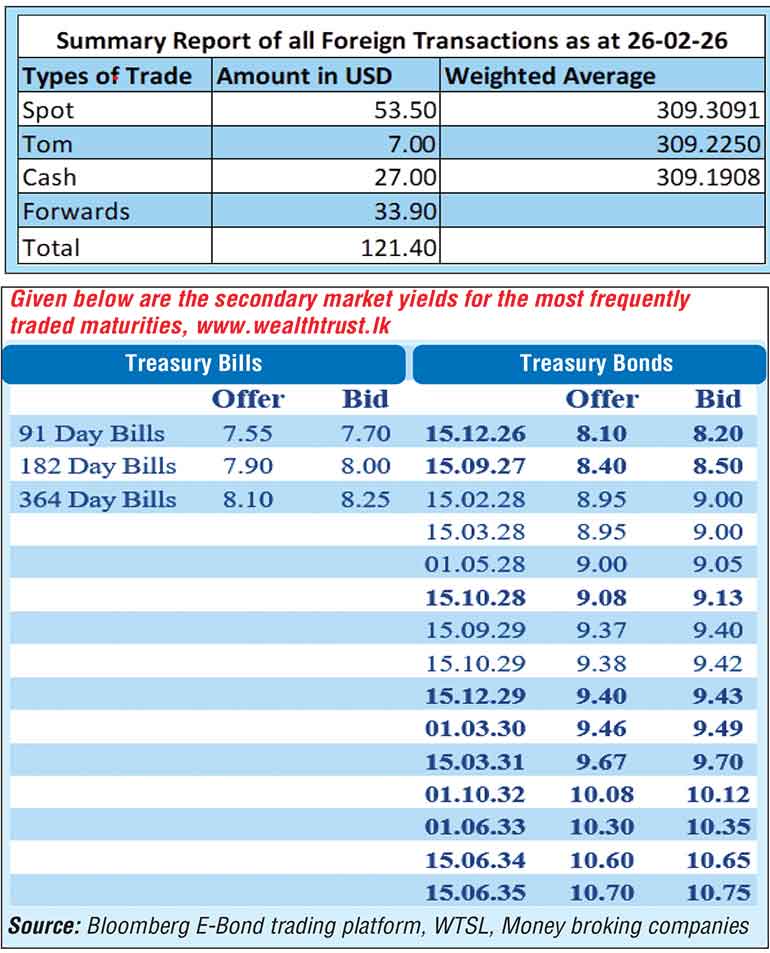

In the forex market, the USD/LKR rate on spot contracts was seen closing the week appreciating slightly to Rs. 309.29/309.32 as against the previous week’s closing level of Rs. 309.35/309.40. This was subsequent to trading at a high of Rs. 309.30 and a low of Rs. 309.38.

The daily USD/LKR average traded volume for the first four trading days of the week stood at

$ 109.56 million.

(References: Public Debt Management Office - Ministry of Finance, Central Bank of Sri Lanka, Bloomberg E-Bond Trading Platform, Money Broking Companies)