Friday Jul 31, 2026

Friday Jul 31, 2026

Wednesday, 26 February 2020 00:01 - - {{hitsCtrl.values.hits}}

SC Securities Ltd. recently held a symposium where it made a compelling case for investing in the Big Three Banks.

The SC Investor Symposium was attended by top institutional and high networth clients.

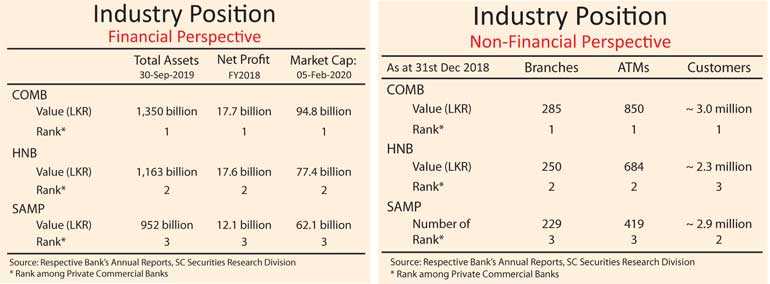

The SC Securities research team provided an overview of the three big commercial banks – Commercial, HNB and Sampath highlighting their respective financial position as well recent achievements including financial performance up to September 2019.

It was pointed out that the Reduction in Statutory Reserve Ratio (SRR) by the Central Bank by 250bps (100bps and 150bps in Nov 2018 and Mar 2019) has enabled the banks to generate additional funds to enhance interest income.

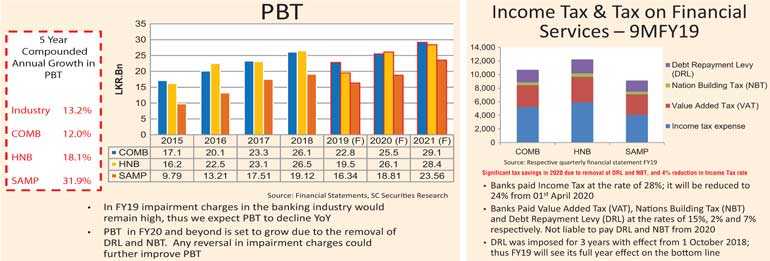

Another facet is that lower income tax from 2020 from 28% to 24% from 1 April will increase the distributable profits for the banks.

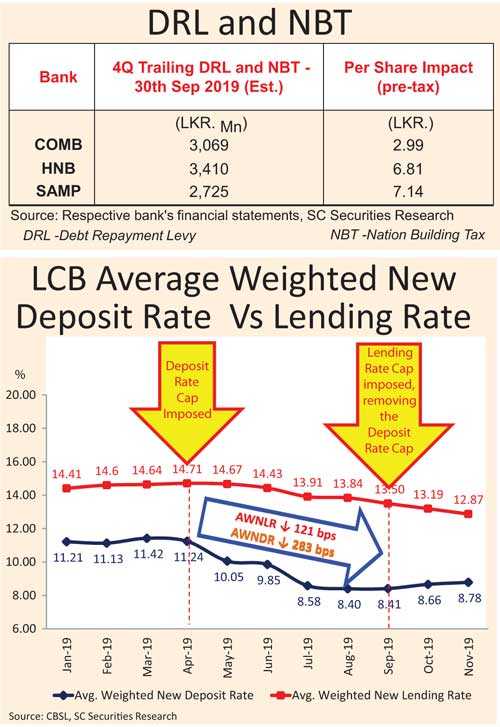

The removal of Debt Repayment Levy (7%) and NBT (2%) according to SC Securities will enable significant savings from 2020.

The broking firm also believes the CASA ratio (current and savings account) to improve in the medium term since reduction in market interest rates generally cause a shift from term deposits to CASA.

In terms of the Government announced credit support scheme to SMEs, SC Securities said certain Non-Performing Loans (NPLs) will get rescheduled. “This could improve recovery of existing NPLs and reduce new NPLs,” it added.

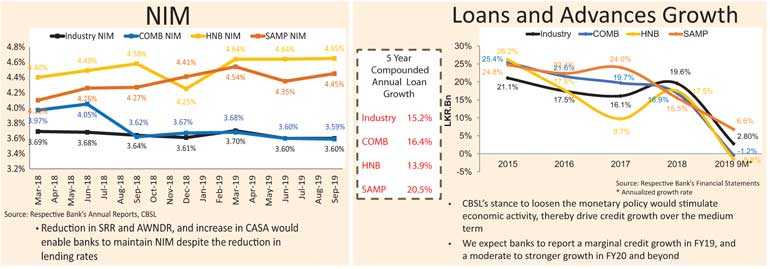

It was pointed out that timely re-pricing of loans and deposits has enabled all three banks to maintain NIM above the banking industry average. (Industry NIM 3.6% | Sep 2019)

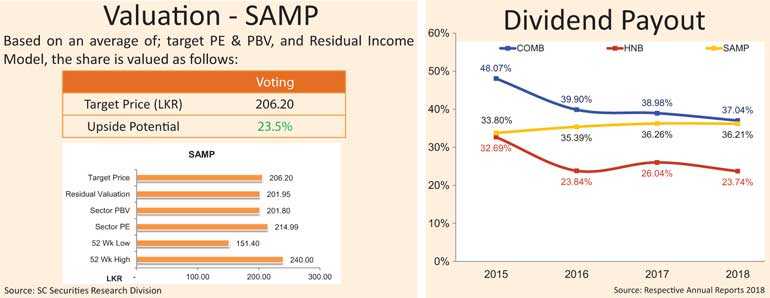

‘The Big Three’ also have offered relatively high dividend yield whilst recent decline in share price has improved the dividend yield.

The banks are also pursuing process efficiencies to improve profitability with IT enabling the efficient use of the cost base; thereby the Cost to Income Ratio (CIR) tipped to decline for all banks. Investors also have the additional comfort of all three banks being well capitalised in line with Basel III capital requirements.

SC Securities said higher economic growth in 2020 aided by the new Government’s fiscal stimulus would boost private consumption and investment activities, thereby improve credit growth.

The banks also stand to benefit by the measures to reduce cost of funds by the Government and the Central Bank.

Among them are reduction of Statuary Reserver Ratio (SRR) by 250 basis points which injected Rs. 150 billion in liquidity and lowering money market rates.

The policy interest rate reduction of 150 basis points enabled the decline of call rates and repo rates.

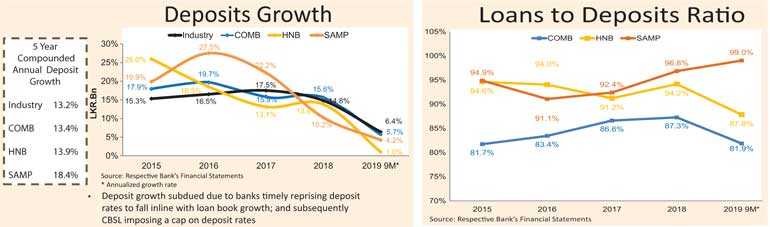

The cap on deposit rates until September 2019 saw AWNDR decline by 283 basis points to 8.41% within four months since April 2019.

With regard to the question of ‘Is the lending rate cap credit positive?’ SC Securities said it was temporary, and subject to review.

“Lending rate cap was imposed after allowing for a substantial decline in cost of funds; hence there shouldn’t be a material impact on interest margins,” the broking firm said.

“Lending rate cap was imposed after allowing for a substantial decline in cost of funds; hence there shouldn’t be a material impact on interest margins,” the broking firm said.

It also expects lower lending rates will stimulate economic activity, thereby improve credit growth.

“Lower lending rates could improve the repayment capacity of borrowers that could reduce non-performing loans,” SC Securities said.

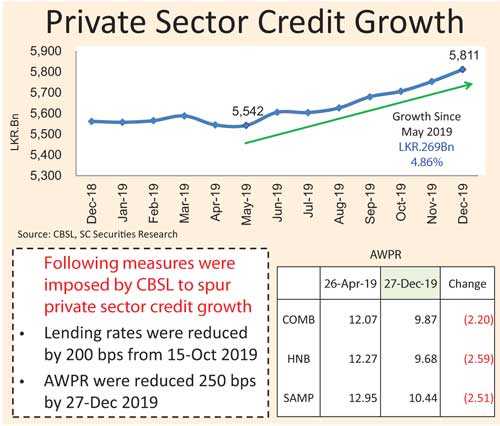

Focusing on credit growth, SC Securities said it is on the up both due to regulatory measures and uptick in business sentiments post the Easter Sunday tragedy.

The Central Bank implemented the following measures to spur private sector credit growth: Lending rates were reduced by 200 bps from 15-Oct 2019; AWPR were reduced 250 bps by 27-Dec 2019. This saw AWPR of COMB decline by 2.2% between April and December 2019 and by 2.59% and 2.51% for HNB and Sampath respectively.

“Private sector credit growth steadily growing since May 2019,” SC Securities said, adding that the fiscal stimulus implemented under the new Government would boost private consumption and investment activities, thereby improve credit growth and Non-Interest Income.

“The reduction in SRR and AWNDR, and increase in CASA would enable banks to maintain NIM despite the reduction in lending rates,” the broking firm said.

Overall SC Securities said the Central Bank’s stance to loosen the monetary policy would stimulate economic activity, thereby drive credit growth over the medium term

“We expect banks to report a marginal credit growth in FY19, and a moderate to stronger growth in FY20 and beyond,” it forecast.

With regard to deposit growth, it said deposit growth subdued due to banks timely reprising deposit rates to fall in line with loan book growth; and subsequently CBSL imposing a cap on deposit rates.

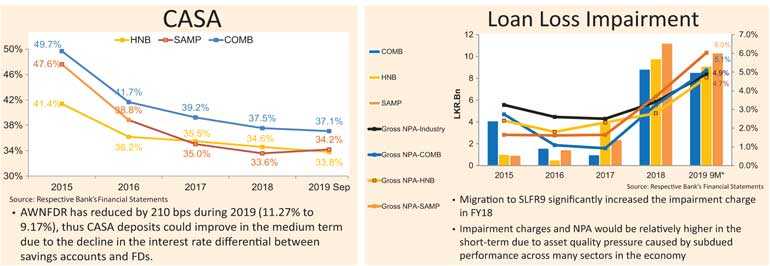

CASA of all banks have declined. SC Securities said AWNFDR has reduced by 210 bps during 2019 (11.27% to 9.17%), thus CASA deposits could improve in the medium term due to the decline in the interest rate differential between savings accounts and FDs.

Addressing the loan loss impairment which was a major issue in recent years, SC Securities said the migration to SLFR9 significantly increased the impairment charge in FY18. “Impairment charges and NPA  would be relatively higher in the short-term due to asset quality pressure caused by subdued performance across many sectors in the economy,” it added.

would be relatively higher in the short-term due to asset quality pressure caused by subdued performance across many sectors in the economy,” it added.

Scope to boost Non-Interest Based Income (NIBI) was also highlighted. The average contribution to Operating Income by NIBI was 27%~29% and high penetration in credit and debit card services is driving growth. It was recalled that the depreciation of LKR in FY18 resulted in a massive foreign exchange gain.

Commenting on the profitability of the three banks, SC Securities said in FY19 impairment charges in the banking industry would remain high, thus it expects PBT to decline YoY. However PBT in FY20 and beyond is set to grow due to the removal of DRL and NBT. Any reversal in impairment charges could further improve PBT.

In FY19 up to first nine months, banks paid Income Tax at the rate of 28%; it will be reduced to 24% from 01st April 2020. Additional the banks Paid Value Added Tax (VAT), Nations Building Tax (NBT) and Debt Repayment Levy (DRL) at the rates of 15%, 2% and 7% respectively. Not liable to pay DRL and NBT from 2020. DRL was imposed for 3 years with effect from 1 October 2018; thus FY19 will see its full year effect on the bottom line.

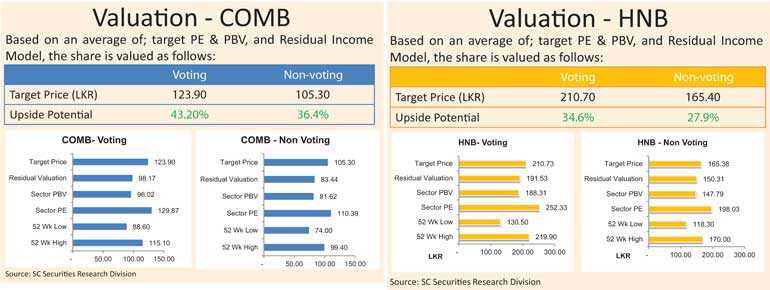

According to SC Securities, based on an average of target PE and PBV, and Residual Income Model, with a target price of Rs. 123.90 (voting) and Rs. 105.30 (non-voting), COMB’s upside potential of its share is 43.2% (voting) and 36.4% (non-voting). For HNB with a target price of 210.70 (voting) and Rs. 165.40 (non-voting), it is 34.6% (Voting) and 27.9% (non-voting) and for Sampath at a target price of Rs. 206.20, the upside potential is 23.5%.