Monday Jul 13, 2026

Monday Jul 13, 2026

Wednesday, 13 May 2026 12:16 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

The weighted average rates at yesterday’s Treasury Bond auctions were seen coming in line with or below market levels, an impressive outcome given the current external backdrop stemming from the Middle East conflict. However, the auction went undersubscribed raising Rs. 176.62 billion out of Rs. 250 billion on offer at the first and second phases — across four available maturities. The bids received to accepted amount ratio stood at 2.47 times; a strong response given the scale of the auction.

The weighted average rates at yesterday’s Treasury Bond auctions were seen coming in line with or below market levels, an impressive outcome given the current external backdrop stemming from the Middle East conflict. However, the auction went undersubscribed raising Rs. 176.62 billion out of Rs. 250 billion on offer at the first and second phases — across four available maturities. The bids received to accepted amount ratio stood at 2.47 times; a strong response given the scale of the auction.

Maturity-wise the results were as follows:

The shorter tenor 01.08.30 maturity was issued at a weighted average yield of 10.16%. This was at very narrow term premium to the 01.07.30 nearest actively quoted maturity. As a result, rates were seen coming in line with market expectations. The entire maturity wise offered amount was fully accepted at the 1st phase.

The 15.06.34 maturity was issued at the weighted average yield of 11.24%. This again was in line with a pre-auction quote of 11.18%/11.22%. The entire maturity wise offered amount was raised at the first phase in competitive bidding.

The longer tenor 15.08.36 maturity was issued at the weighted average of 11.40%. This was below market expectations. However, maturity wise it went undersubscribed across the first and second phases.

The 15.08.39 maturity was rejected.

An issuance window is now open on the 2030 and 2034 tenors until 3.00 pm of 14.05.2026 at the Weighted Average Yield Rates (WAYR) determined for the said ISIN at the auction, up to 10% of the respective amount offered (see table for details of the auction).

Meanwhile, the secondary Bond market yesterday mainly rallied post auction with rates dropping on the back of aggressive buying. Market activity and transaction volumes were seen at heightened levels during the day.

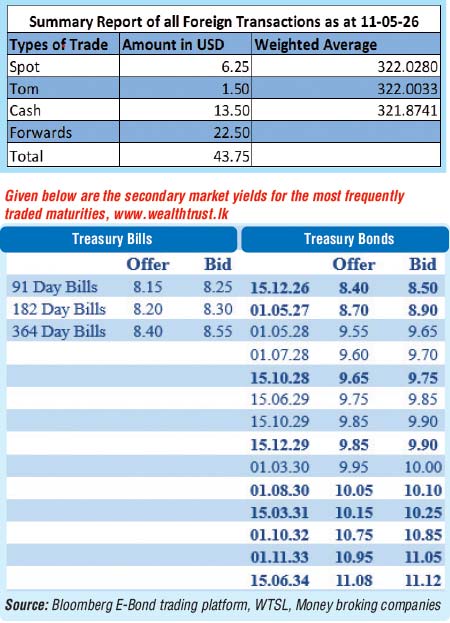

Accordingly, the 01.07.30 maturity traded down the range of 10.15% to a low of 10.05% and the 01.08.30 Bond traded down to a low of 10.10% post auction well below the issued weighted average rate. The 15.10.28 and 15.12.28 maturities traded at the rates of 9.75%-9.71% and 9.78%-9.75% respectively. The 15.06.29 maturity traded at the rate of 9.80%, the 15.10.29 maturity traded at the rate of 9.90%. The 15.12.32 maturity traded at the rate of 10.80%. The 15.06.34 auction maturity traded down to a low of 11.08% post auction well below its auction weighted average.

In the money market, the net liquidity surplus was recorded at Rs. 247.19 billion yesterday. An amount of Rs. 178.06 billion was deposited at Central Bank’s SDFR (Standing Deposit Facility Rate) of 7.25% as against an amount of Rs. 5.87 billion withdrawn from the Central Bank’s SLFR (Standing Lending Facility Rate) of 8.25%. In addition, the Domestic Operations Department (DOD) of the Central Bank of Sri Lanka drained out an amount of Rs. 75 billion by way of overnight repo auction at a weighted average rate of 7.70%.

The weighted average rates on overnight call money and Repo were recorded at 7.77% and 7.82% respectively.

Forex market

In the forex market, the USD/LKR rate on spot contracts were seen closing the day at Rs.322.50/323.00 as against its previous day’s closing level of Rs. 322.00/322.40.

The total USD/LKR traded volume for 11th May 2026 was $ 43.75 million.

(References: Public Debt Management Office- Ministry of Finance, Central Bank of Sri Lanka, Bloomberg E-Bond trading platform, Money broking companies)