Friday Jun 05, 2026

Friday Jun 05, 2026

Friday, 29 May 2026 06:21 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

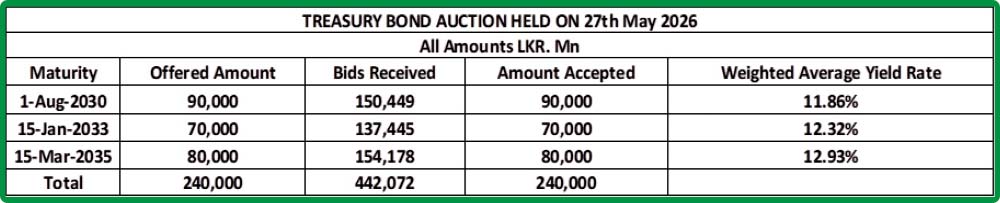

The weighted average yield rates at Wednesday’s Treasury Bond auction increased in line with the Monetary Policy rate hike of 100 bps and the corresponding increase in yields observed at the Treasury Bill auction delivered and conducted the day prior.

The weighted average yield rates at Wednesday’s Treasury Bond auction increased in line with the Monetary Policy rate hike of 100 bps and the corresponding increase in yields observed at the Treasury Bill auction delivered and conducted the day prior.

The prevailing Middle Eastern tensions as well as volatile and elevated crude oil prices continued to weigh on sentiment and result in a bearish bias. However, the auction was fully subscribed, with the entire Rs. 240 billion on offer raised at the first phase in competitive bidding.

This was a remarkable outcome given the prevailing backdrop. The bids received to accepted amount ratio stood at 1.84 times; a strong response given the scale of the auction.

Maturity-wise the results were as follows:

The shorter tenor 01.08.30 maturity was issued at a weighted average yield of 11.86%.

The 15.01.33 maturity was issued at the weighted average yield of 12.32%.

The longer tenor 15.03.35 maturity was issued at the weighted average of 12.93%.

An issuance window is now open on all 3 tenors until 3 p.m. of 29.05.2026 at the Weighted Average Yield Rates (WAYR) determined for the said ISIN at the auction, up to 10% of the respective amount offered.

Meanwhile, the secondary Bond market yesterday remained mostly quiet earlier during the day as the auction was ongoing as market participants mostly stuck to the sidelines. However, post auction renewed buying was observed as traders looked to dollar cost average into the new issuance as well as fresh book building interest was observed. Accordingly, market activity and transaction volumes were seen at robust levels post auction.

Accordingly, the 01.08.30 maturity traded within the range of 12.10% to 12%, the 15.01.33 maturity traded at the rate of 12.52% and the 15.03.35 maturity at the rate of 13.10% post auction. Additionally, trades were observed on the 15.03.28 maturity traded at the rate of 10.25% and the 01.07.30 maturity traded at the rate of 12.05%.

In the money market, the net liquidity surplus was recorded at Rs. 126.70 billion yesterday. An amount of Rs. 140.98 billion was deposited at Central Banks SDFR (Standing Deposit Facility Rate) of 8.25% as against an amount of Rs. 89.27 billion withdrawn from the Central Banks SLFR (Standing Lending Facility Rate) of 9.25%. In addition, the Domestic Operations Department (DOD) of the Central Bank of Sri Lanka drained out an amount of Rs. 75 billion by way of overnight repo auction at a weighted average rate of 8.75%.

The weighted average rates on overnight call money and Repo were recorded at 9.05% and 9.07% respectively.

Forex market

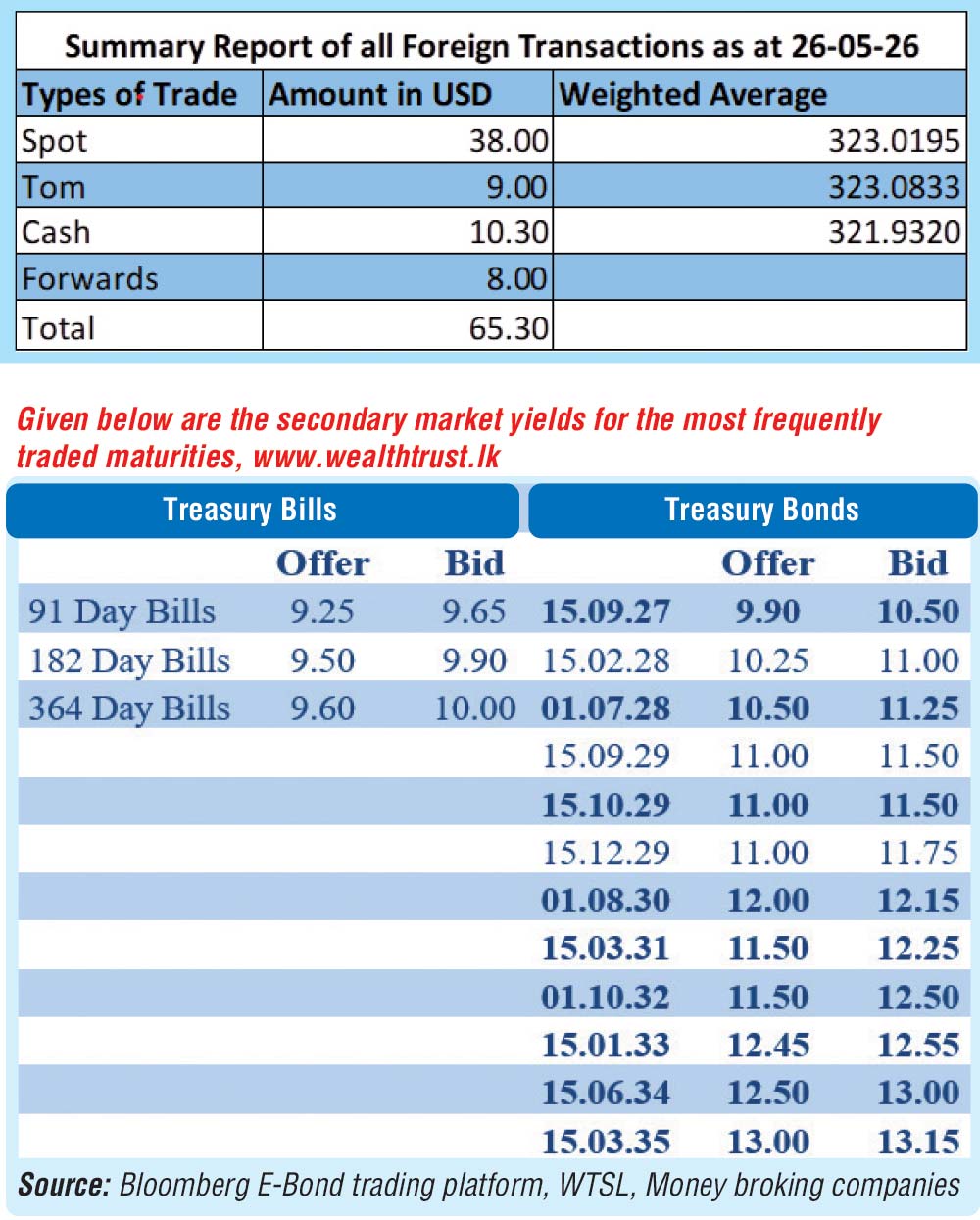

In the Forex market, the USD/LKR rate on spot contracts were seen closing the day at Rs.328.50/332 as against its previous day’s closing level of Rs. 324.50/326.

The total USD/LKR traded volume for 26 May 2026 was $ 65.30 million.

(References: Public Debt Management Office- Ministry of Finance, Central Bank of Sri Lanka, Bloomberg E-Bond trading platform, Money broking companies)