Tuesday Jul 28, 2026

Tuesday Jul 28, 2026

Wednesday, 25 February 2026 00:10 - - {{hitsCtrl.values.hits}}

By The Insurance Regulatory Commission of Sri Lanka

The insurance sector remains a key component of Sri Lanka’s financial system, particularly in an environment characterised by past economic uncertainty and the increasing impact of recurring natural disasters. By providing financial protection against unexpected losses, insurance plays a vital role in supporting households, businesses, and industries to recover from adverse events, while contributing to overall economic stability through effective risk transfer and mitigation.

A resilient and well-functioning insurance sector is essential to strengthening economic confidence, promoting investment, and safeguarding livelihoods. As Sri Lanka continues its path toward economic recovery and sustainable growth, the performance and stability of the insurance sector remain important to enhancing long-term national resilience.

As of 30 September 2025, the insurance sector’s performance was as follows:

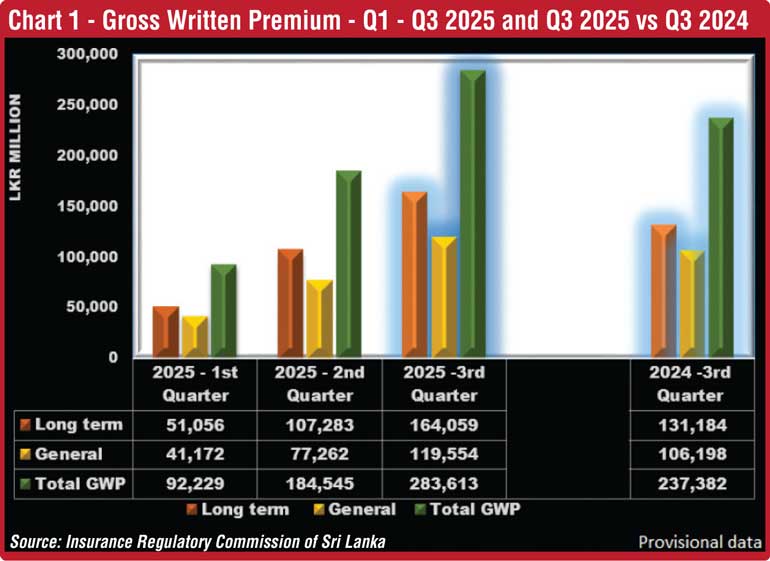

Gross Written Premium (GWP)

As illustrated in Chart 1, the insurance industry recorded a consistent and robust growth in Gross Written Premium (GWP) throughout the first three quarters of 2025, reflecting strengthening market activity across both long-term and general insurance segments.

In the first quarter of 2025, total GWP amounted to Rs. 92,229 million, comprising Rs. 51,056 million from the long-term insurance segment and Rs. 41,172 million from general insurance. During the second quarter of 2025, total GWP increased significantly to Rs. 184,545 million, with contributions of Rs. 107,283 million from long-term insurance and Rs. 77,262 million from general insurance, indicating broad-based growth across the sector.

The upward momentum continued into the third quarter of 2025, with a total GWP reaching Rs. 283,613 million. This growth was driven by Rs. 164,059 million from long-term insurance and Rs. 119,554 million from general insurance, marking the highest quarterly premium volume recorded during the period under review.

Total GWP in Q3 2025 increased by 19.48% compared to Rs. 237,382 million recorded in Q3 2024, representing an absolute increase of Rs. 46,231 million. The long-term insurance sector was the primary contributor to this growth, with GWP rising by 25.06% to Rs. 164,059 million in Q3 2025, compared to Rs. 131,184 million in the corresponding quarter of 2024. Meanwhile, the general insurance sector recorded a moderate but steady growth, with GWP increasing by 12.58% to Rs. 119,554 million in Q3 2025, up from Rs. 106,198 million in Q3 2024. Compared to Q3 2024, the growth in Q3 2025 was mainly driven by Motor insurance segment, which increased by 20.15% compared to Q3 2024. Motor insurance has regained its position as the largest contributor to General Insurance premiums, accounting for nearly 47% of the total GWP. In contrast, the Fire insurance segment showed minimal improvement, recording marginal growth of 0.22% compared to the same period last year. Meanwhile, specialised insurance lines demonstrated strong performance, with SRCC growing by 15.70% and Marine insurance by 13.09%, indicating increased demand for coverage related to trade activity and civil risk protection. In contrast, the health insurance segment registered a comparatively moderate growth of 5% against Q3 2024.

The sustained growth in GWP across both segments underscores the strengthening role of the insurance sector in supporting financial protection and economic resilience in Sri Lanka.

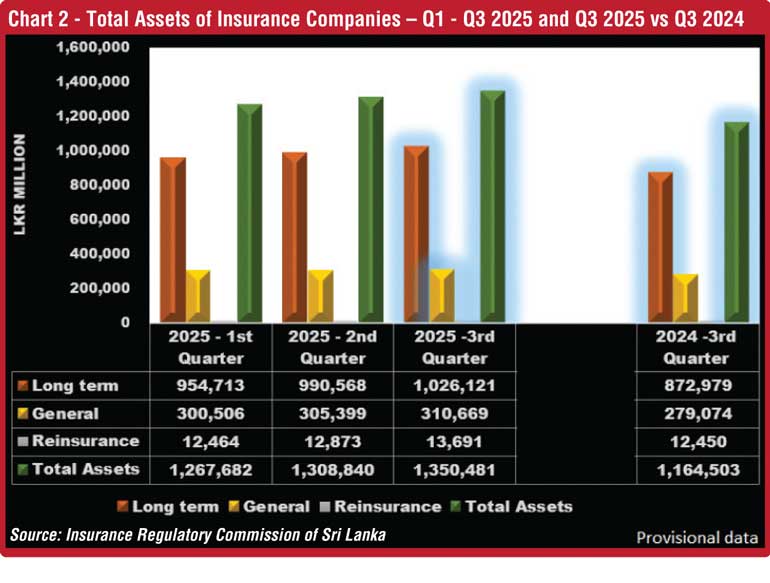

Total Assets

As illustrated in Chart 2, the insurance sector recorded steady and sustained growth in total assets throughout the first three quarters of 2025, reflecting continued strengthening of the sector’s financial base across all business segments.

In the first quarter of 2025, total assets amounted to Rs. 1,267,682 million, comprising Rs. 954,713 million in long-term insurance assets, Rs. 300,506 million in general insurance assets, and Rs. 12,464 million in reinsurance assets. During the second quarter of 2025, total assets increased to Rs. 1,308,840 million, driven by growth in long-term insurance assets to Rs. 990,568 million, general insurance assets to Rs. 305,399 million, and reinsurance assets to Rs. 12,873 million.

The upward trend continued in the third quarter of 2025, with the sector’s total assets expanding to Rs. 1,350,481 million. This increase was supported by Rs. 1,026,121 million in long-term insurance assets, Rs. 310,669 million in general insurance assets, and Rs. 13,691 million in reinsurance assets. Total assets in Q3 2025 recorded a notable growth of 15.97%, compared to Rs. 1,164,503 million in Q3 2024, reflecting an absolute increase of Rs. 185,978 million.

The long-term insurance sector remained the principal contributor to asset growth, with assets increasing by 17.54% to Rs. 1,026,121 million in Q3 2025, from Rs. 872,979 million in the corresponding quarter of 2024.

The general insurance sector also demonstrated healthy growth, with assets rising by 11.32% to Rs. 310,669 million, compared to Rs. 279,074 million in Q3 2024. The sustained expansion in total assets underscores the strengthening financial capacity and resilience of Sri Lanka’s insurance sector.

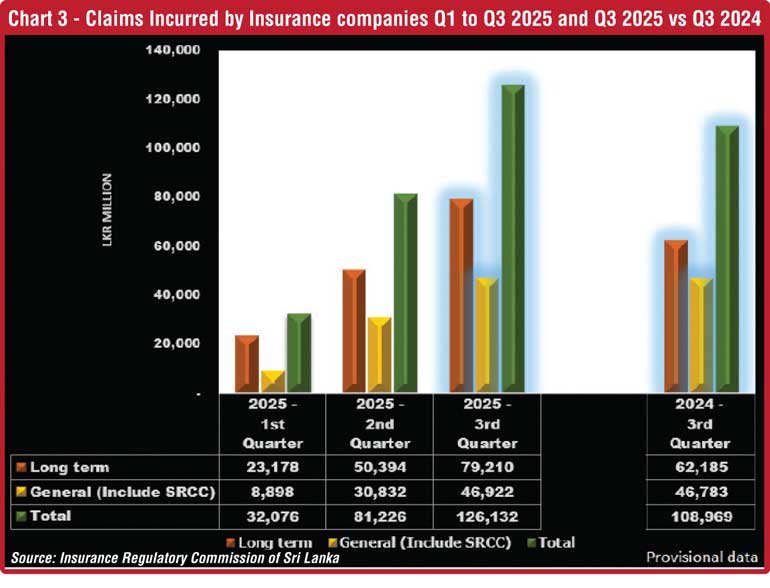

Claims Incurred by insurance companies

As detailed in Chart 3, the insurance sector recorded a steady increase in claims incurred across both the long-term and general insurance segments during the first three quarters of 2025, reflecting increased benefit payments and claims settlements to policyholders.

In the first quarter of 2025, total claims incurred amounted to Rs. 32,076 million, comprising Rs. 23,178 million from the long-term insurance segment and Rs. 8,898 million from the general insurance segment (including SRCC). During the second quarter of 2025, total claims increased significantly to LKR 81,226 million, supported by LKR 50,394 million in long-term insurance claims and Rs. 30,832 million in general insurance claims. The upward trend continued into the third quarter of 2025, with total claims incurred reaching Rs. 126,132 million. This comprised Rs. 79,210 million from long-term insurance and Rs. 46,922 million from general insurance. Total claims incurred in Q3 2025 increased by 15.75%, compared to Rs. 108,969 million recorded in Q3 2024.

Claims arising from the long-term insurance business, which primarily include maturity and death benefits, recorded a significant increase of 27.38%, rising to Rs. 79,210 million in Q3 2025 from Rs. 62,185 million in the corresponding quarter of the previous year. In contrast, claims incurred by the general insurance sector, covering Motor, Fire, Marine, and other classes of business (including SRCC), recorded a marginal increase of 0.3%, amounting to Rs. 46,922 million in Q3 2025, compared to Rs. 46,783 million in Q3 2024. The increase in claims incurred highlights the insurance sector’s growing financial commitments in meeting policyholder obligations and underscores the importance of maintaining strong operational capacity and financial resilience to support the sector’s long-term stability.

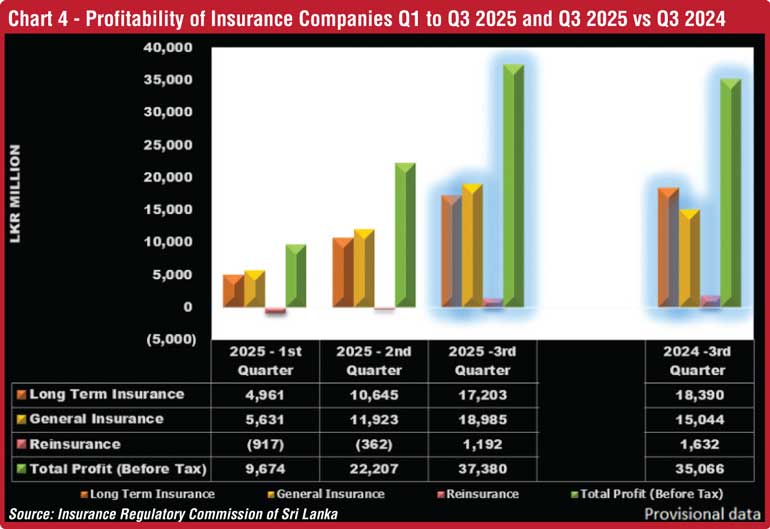

Profit (Before Tax) of insurance companies

The insurance industry exhibited a steady improvement in profitability across the first three quarters of 2025. The sector recorded a total Profit Before Tax (PBT) of Rs. 9,674 million in Q1, primarily supported by Long-Term Insurance (Rs. 4,961 million) and General Insurance (Rs. 5,631 million), despite a loss of Rs. 917 million in Reinsurance. Profitability strengthened in Q2, with total PBT rising to Rs. 22,207 million, and the Reinsurance loss significantly narrowed to Rs. 362 million. By Q3, sector performance increase, achieving a total PBT of Rs. 37,380 million, driven by strong figures from Long-Term (Rs. 17,203 million) and General Insurance (Rs. 18,985 million), alongside a positive turnaround in Reinsurance, which posted a profit of Rs. 1,192 million.

The combined PBT for the insurance industry increased from Rs. 35,066 million in Q3 2024 to Rs. 37,380 million in Q3 2025, reflecting a modest increase of 6.6% (Rs. 2,314 million). However, segmental performance was mixed. The Long-Term Insurance business reported a reduction in PBT, falling by 6.46% from Rs. 18,390 million in Q3 2024 to Rs. 17,203 million in Q3 2025. Conversely, the General Insurance business experienced significant growth, with its PBT rising by 26.2% from Rs. 15,044 million to Rs. 18,985 million over the same period.

Investment in Government Securities

In terms of asset allocation, industry-wide investments in Government Debt Securities showed a consistent increase throughout the first three quarters of 2025. Total investments by both Long-term and General insurance sectors were recorded at Rs. 611,017 million in the first quarter (Q1), rose to Rs. 628,407 million in the second quarter (Q2), and further increased to Rs. 672,203 million in the third quarter (Q3).

As at the end of Q3 2025, the total value of investments in Government Debt Securities amounted to Rs. 672,203 million, representing a significant overall increase of 13.47% compared to the Rs. 592,396 million recorded in the corresponding period of Q3 2024. A segmental analysis indicates that the Long-Term Insurance business was the primary driver of this growth, with its investments increasing by 16.15% to Rs. 562,044 million, accounting for 60.01% of its total investments. In contrast, the General Insurance business recorded a relatively marginal increase of 1.53% in its investments in Government Debt Securities, amounting to Rs. 110,159 million, which represented 54.47% of its total investments.

Insurance brokers

The insurance brokering segment demonstrated robust growth. As of September 30, 2025, eighty-two (82) insurance brokering companies were registered with the Commission. The total assets of these brokers increased substantially to Rs. 19,550 million by the end of Q3 2025, compared to Rs. 14,774 million in Q3 2024, signifying a strong growth rate of 32.32%.