Saturday Jul 18, 2026

Saturday Jul 18, 2026

Monday, 22 April 2024 00:08 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

Activity in the secondary bond market remained moderate during the week ending 19 April 2024, with the market maintaining a holding pattern for much of the week. Yields were observed moving sideways, with trading fluctuating within a narrow band. As market participants were seen adopting a wait-and-see approach.

This was against the back-drop of the news that Sri Lanka’s recent debt restructuring talks with international bondholders had not reached a finalized conclusion and that despite progress, points of contention still persist, reported on the 16 of April (last Tuesday). The news generated mixed reactions as optimism was shared that negotiations are still ongoing and likely will be concluded in the next few coming weeks. However, international sovereign bond prices were seen declining on the news. In addition, it was also stated by government officials that the bilateral debt aspect of external debt restructuring had seen considerable progress and was nearing conclusion.

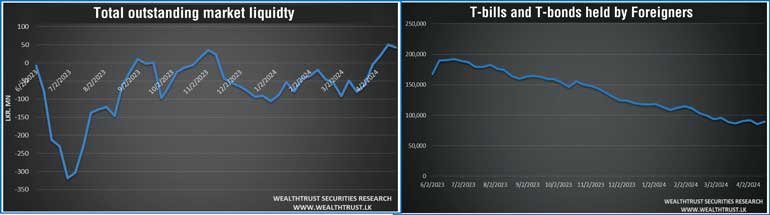

Interestingly, the foreign holding in Rupee bonds and bills for the week ending 18 April 2024 recorded a net inflow, amounting to Rs. 3.86 billion. As a result, the total holding increased to Rs. 89.27 billion.

Initially, the local bond market participants too responded positively to the news with yields dropping at first. However subsequently yields were seen increasing marginally at the tail end of the week; with closing two-way quotes moving up on a week-on-week basis.

Trading was predominantly on the short end of the yield curve, with a particular emphasis on 2025 to 2028 durations. The short tenor 01.07.25 was seen changing hands within the range of 10.60% to 10.55%. The liquid 2026 tenors of 01.06.26, 15.05.26 and 01.08.26 were seen hitting intraweek lows of 11.10% as against intraweek highs of 11.20%. Similarly, the relatively longer 2026 tenor of 15.12.26 was seen declining to an intraweek low of 11.30% before moving back up to intraweek highs of 11.35%. Meanwhile the popular 2028 tenors (15.03.28, 01.05.28, 01.07.28 and 15.12.28) dropped to intraweek lows of 12.10% before moving back to intraweek highs of 12.20%. Additionally, the shorter 2027 tenor 15.01.27 maturity was seen moving up to 11.38% from lows of 11.35%, while the longer 2027 tenors of 01.05.27 and 15.09.27 was seen moving up to 12.00% from lows of 11.76%. Overall transaction volumes also remained moderate.

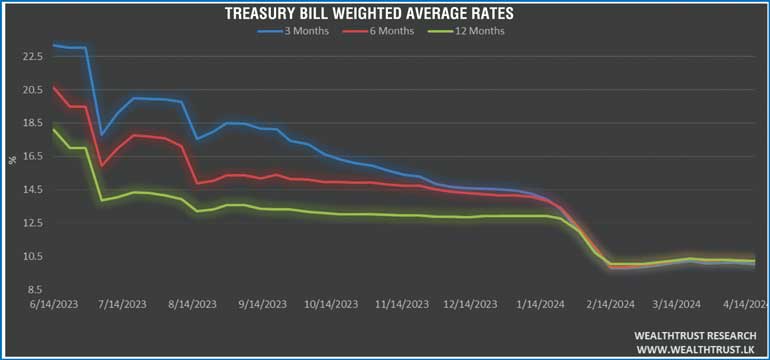

At the weekly Treasury bill auction conducted last Wednesday (17 April 2024), the weighted average yields were seen decreasing across all three maturities for a second consecutive week. The 91-day maturity reduced by 07 basis points to 10.03%, while the 182-day maturity decreased by 05 basis points to 10.22% and the 364-day maturity dropped by 04 basis point to 10.23%. The entire offered amount of Rs. 78.00 billion was taken up at the 1st phase, with bids received exceeding the offered amount by 2.5 times. Subsequently the 2nd phase of subscription was opened across all tenors at the weighted averages determined at the 1st phase. Where an additional amount of Rs. 7.80 billion was raised across all three maturities being the maximum amount offered, out of total market subscription of a staggering Rs. 75.94 billion.

The daily secondary market Treasury bond/bill transacted volumes for the first four days of the week averaged at Rs. 24.46 billion.

In money markets, the total outstanding liquidity surplus recorded at Rs. 43.03 billion by the week ending 19 April, down from the previous week’s surplus of Rs. 49.81 billion. The Domestic Operations Department (DOD) of Central Bank continued to inject liquidity during the week by way of overnight and seven-day term reverse repo auctions at weighted average yields ranging from 8.59% to 8.85%.

The Central Bank of Sri Lankas (CBSL) holding of Government Securities was registered at Rs. 2,675.62 billion as at 19 April 2024, unchanged against its previous week’s level.

In the Forex market, the USD/LKR rate on spot contracts was seen depreciating during the week to close at Rs. 302.00/302.50. This is as against its previous weeks closing level of Rs. 298.50/298.55 and subsequent to trading at a high of Rs. 298.50 and a low of Rs. 302.00.

The daily USD/LKR average traded volume for the first four trading days of the week stood at $ 34.75 million.

(References: Central Bank of Sri Lanka, Bloomberg E-Bond trading platform, Money broking companies)