Monday Jul 13, 2026

Monday Jul 13, 2026

Monday, 13 July 2026 02:38 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

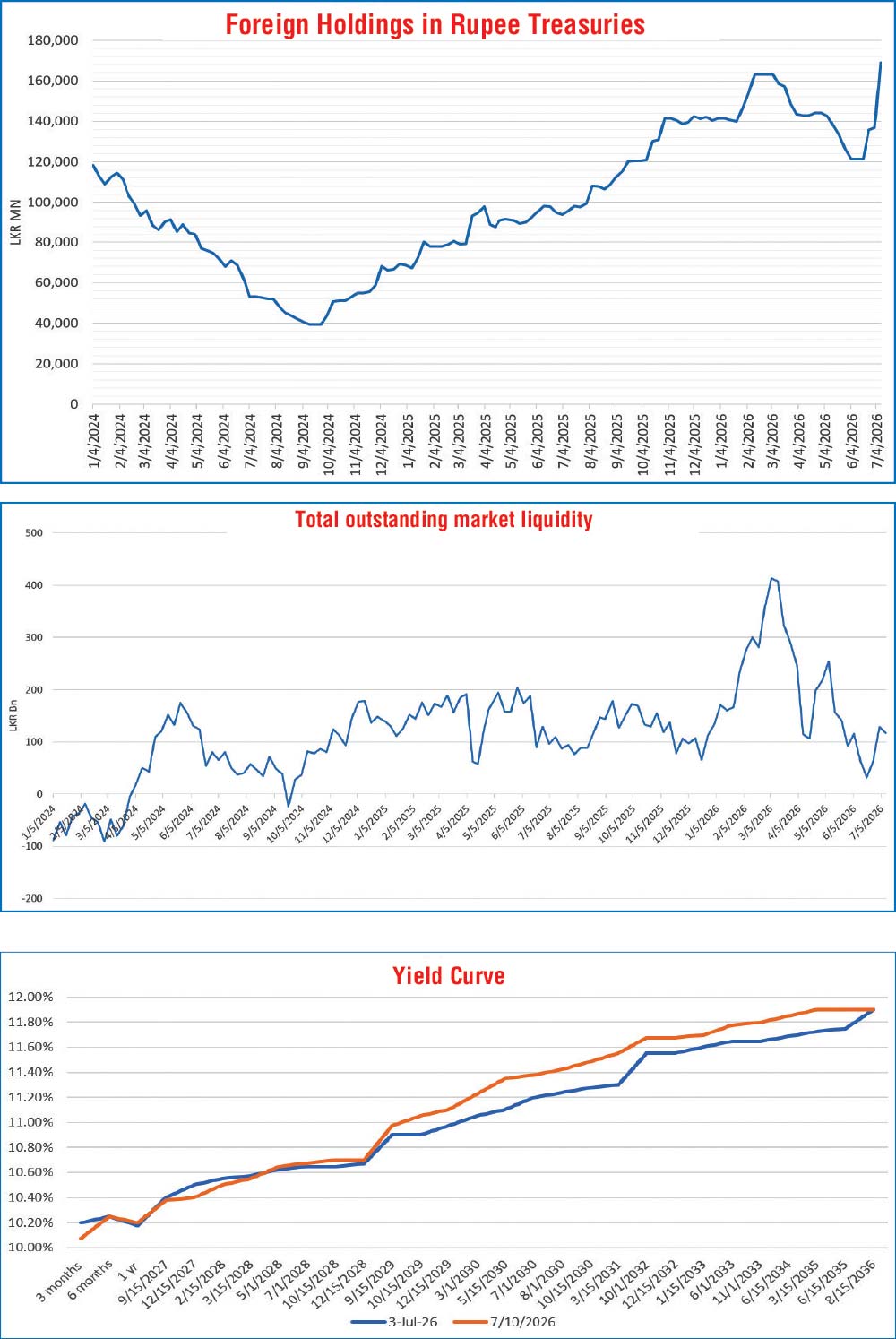

The foreign portfolio demand for rupee-denominated Government securities saw its highest weekly inflow since February 2013, at Rs 32.04 billion for the week ending 9 July.

The foreign portfolio demand for rupee-denominated Government securities saw its highest weekly inflow since February 2013, at Rs 32.04 billion for the week ending 9 July.

As a result, foreign holdings in Government securities hit its highest level in nearly three years since August 2023, at Rs 168.90 billion. This reflected five consecutive weeks of net foreign inflows. Notably, the recent re-entry by foreign portfolios has offset the decline observed since the breakout of the Middle East conflict- resulting in a V-shaped recovery.

Meanwhile, the secondary Bond market started off the trading week ending 10 July on a subdued note as market participants stayed on the sidelines and as yields consolidated from its previous weeks closing levels.

Sentiment shifted mid-week as renewed geopolitical tensions in the Middle East, including escalating US-Iran hostilities and re-imposed sanctions on Iranian oil exports, pushed global oil prices higher. The deterioration in the external backdrop prompted an upward adjustment in yields.

On Thursday, yields remained elevated but stabilised as renewed buying interest emerged at the higher levels, helping absorb selling pressure. Activity and transaction volumes improved to healthy levels- spurred by a partial recovery in global oil prices.

By Friday, market participants adopted a cautious wait-and-see approach ahead of the Treasury Bond auctions, resulting in slower trading activity, while secondary market two-way quotes finished the week higher, reflecting the overall upward re-pricing in yields and a parallel shift upwards of the yield curve.

In trading during the week, on the two-year duration of 2028’s, 15.02.28, 15.03.28, 01.05.28, 01.07.28 and 15.10.28 maturities changed hands at the rates of 10.5%, 10.55%,10.6%, 10.65%–10.7% and 10.7%, respectively.

Moving into the 2029 segment, the 15.12.29 changed hands at the rate of 11%.

In the 2030 space, the 01.03.30 maturity traded at the rate of 11.10%, while the 01.07.30, 01.08.30 and 15.10.30 maturities changed hands from intraweek lows 11.25% each and 11.30% respectively to highs of 11.4%, 11.45% and 11.5%.

Further along the curve, the 01.10.32 maturity changed hands at the rate of 11.65% and the 15.12.32 traded at the rate of 11.6%. The 15.01.33 maturity traded up from an intraweek low of 11.6% to a high of 11.7%, while the 01.11.33 traded up from an intraweek low of 11.66% to a high of 11.8%. The 15.06.34 traded within the range of 11.8% to 11.85%.

At the longer end, the 15.03.35 maturity traded up from an intraweek low of 11.7% to a high of 11.8%, while the 15.06.35 changed hands at the rate of 11.75%.

In the money market, the total outstanding liquidity surplus was recorded at Rs. 116.72 billion at the end of the week, as against its previous week’s Rs. 128.47 billion- remaining above Rs. 100 billion throughout the week. The weighted average interest rates on Call Money and Repo eased to 9.01% and 9.05%, respectively, at the close of the week as against the previous week’s closing levels of 9.2% and 9.24%.

At the weekly Treasury Bill auction, the weighted average yields held broadly steady, breaking a two-week streak of across-the-board increases prior. Accordingly, the rate on the 91-day tenor reduced by two basis points to 10.21%, the 182-day tenor remained unchanged at 10.3% and the 364-day tenor edged up marginally by one basis point to 10.21%.

The auction successfully raised the full Rs. 100 billion offered at the first phase of competitive bidding. However, the bulk of the quantity raised was from the 91-day tenor, which raised more than its offered amount, while the other two tenors raised the same or less than their respective offered amounts. Total bids received amounted to 2.3 times of the offered amount up from 1.66 times the week before.

Notably, Secondary Market T-Bill buying saw rates decline – with October Bills (3 months) trading down the range of 10.15%-10% post-auction on the back of considerable volumes.

This comes ahead of today’s Bond auctions. The round of auctions will have a total offered amount of Rs. 150 billion across three available maturities.

The auction will be comprised of: Rs. 70 billion from a 15 October 2030 maturity bearing a coupon rate of 11%; Rs. 50 billion from a 15 October 2034 maturity bearing a coupon rate of 11.7%; Rs. 30 billion from a 1 July 2037 maturity bearing a coupon rate of 10.75%, the settlement for which will be held on 15 July.

For context, the previous Treasury Bond auction conducted on 26 June saw the 15.10.30 maturity record a weighted average yield of 11.44%, while the 15.03.35 maturity was issued at 11.88%.

Forex market

In the forex market, the USD/LKR rate on spot contracts was seen closing the week depreciating to Rs. 335.70/335.85 as against its previous weeks closing of Rs. 335.20/335.30. This was subsequent to trading from at an intraweek high of Rs. 334.70 and a low of Rs.336.

The daily USD/LKR average traded volume for the first four trading days of the week stood at $ 67.88 million.

(References: Public Debt Management Office - Ministry of Finance, Central Bank of Sri Lanka, Bloomberg E-Bond Trading Platform, Money Broking Companies)