Thursday Aug 06, 2026

Thursday Aug 06, 2026

Wednesday, 10 June 2026 05:16 - - {{hitsCtrl.values.hits}}

The Insurance Regulatory Commission of Sri Lanka (IRCSL) presents an overview of the performance of Sri Lanka’s insurance sector for the period 2021 to 2025, together with a comparative analysis of sector developments during 4Q 2025 in comparison with 4Q 2024 reflecting the insurance sector’s evolving contribution to Sri Lanka’s economic and financial landscape.

Sri Lanka’s insurance industry has demonstrated remarkable resilience from 2021 through 2025, successfully navigating the challenges posed by the COVID-19 pandemic and the severe economic crisis of 2022. A significant turning point came with the Ditwa cyclone at the end of 2025, which underscored the critical role of insurance in supporting recovery and rebuilding efforts across the country.

The impact of the Ditwa cyclone highlighted the importance of risk protection, as insurers played a vital role in assisting affected communities and reinforcing financial stability. Despite these challenges, the sector remained robust, reaffirming its commitment to protecting policyholders and ensuring business continuity. As the regulator, the IRCSL worked closely with the insurance industry to support national recovery by facilitating the timely and efficient settlement of Ditwa-related claims.

As of May 25, 2026, the insurance sector has recorded a total of 24,757 Ditwah disaster-related claims. The estimated total value of claims reported to the insurance industry has reached approximately Rs. 56 billion, underscoring the severe financial impact of the disaster.

Out of the total motor insurance claims reported, 79% have already been settled, reflecting the insurance industry’s continued commitment to supporting timely recovery efforts and maintaining financial stability. In relation to non-motor insurance claims reported, 44% have been settled.

The comparatively lower settlement rate for non-motor claims is primarily due to the complexity of these claims, which often require detailed loss assessments, property inspections, valuation of damages, and the submission of supporting documentation before settlements can be finalised.

In 2025, both life and general insurance sectors recorded improvements supported by proactive regulatory measures from the IRCSL. Over the past five years, the industry has made significant progress toward sustainability, with the positive momentum continuing into the fourth quarter of 2025, marked by a steady increase in Gross Written Premiums (GWP).

These developments highlight the insurance sector’s vital contribution to Sri Lanka’s economic recovery and emphasise the ongoing need for innovation and regulatory support to expand insurance coverage across all segments of society.

As of 31 December 2025, fifteen (15) companies were operating in the Long-Term (Life) Insurance sector, while fourteen (14) companies were engaged in the General Insurance Sector.

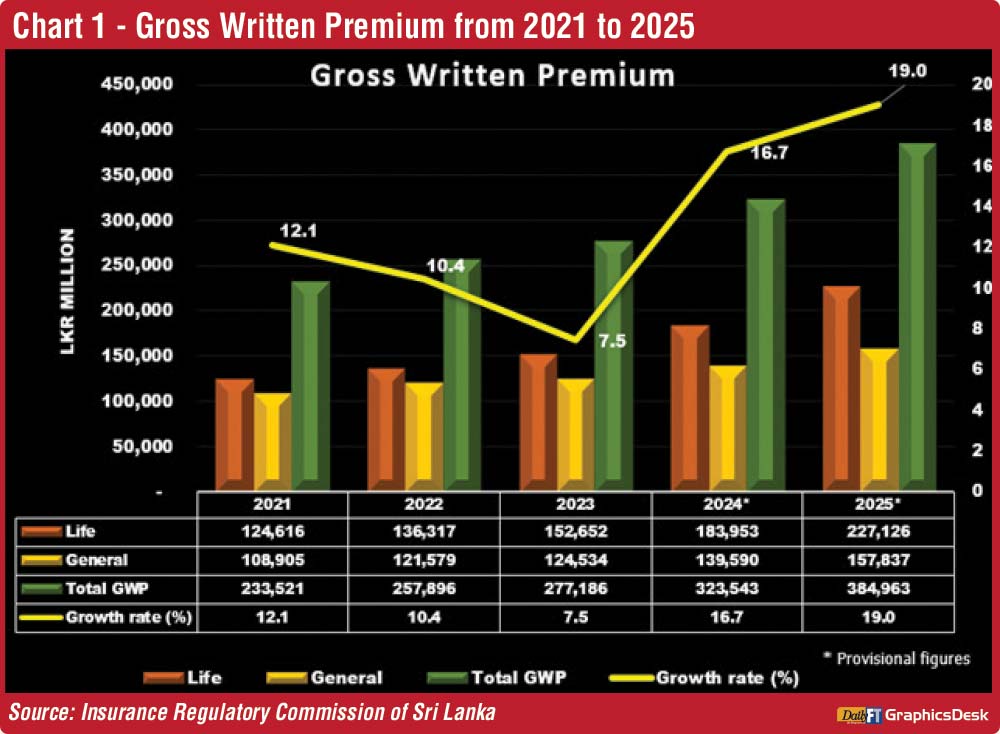

Gross Written Premium (GWP)

Chart 1 illustrates the performance of the insurance industry from 2021 to 2025. Total GWP increased significantly, reaching Rs. 384,963 million in 2025 compared to Rs. 233,521 million in 2021, representing a strong growth of 64.9%.

The Long-Term (Life) Insurance sector recorded a robust growth in GWP, increasing from Rs. 124,616 million in 2021 to Rs. 227,126 million in 2025. This upward trend highlights the sector’s growing attractiveness and the increasing awareness among policyholders of the importance of long-term financial protection and security.

Similarly, the General Insurance sector recorded growth during this period, with GWP increasing from Rs. 108,905 million in 2021 to Rs. 157,837 million in 2025. This upward trend signifies enhanced public awareness and acceptance of insurance products across Sri Lanka.

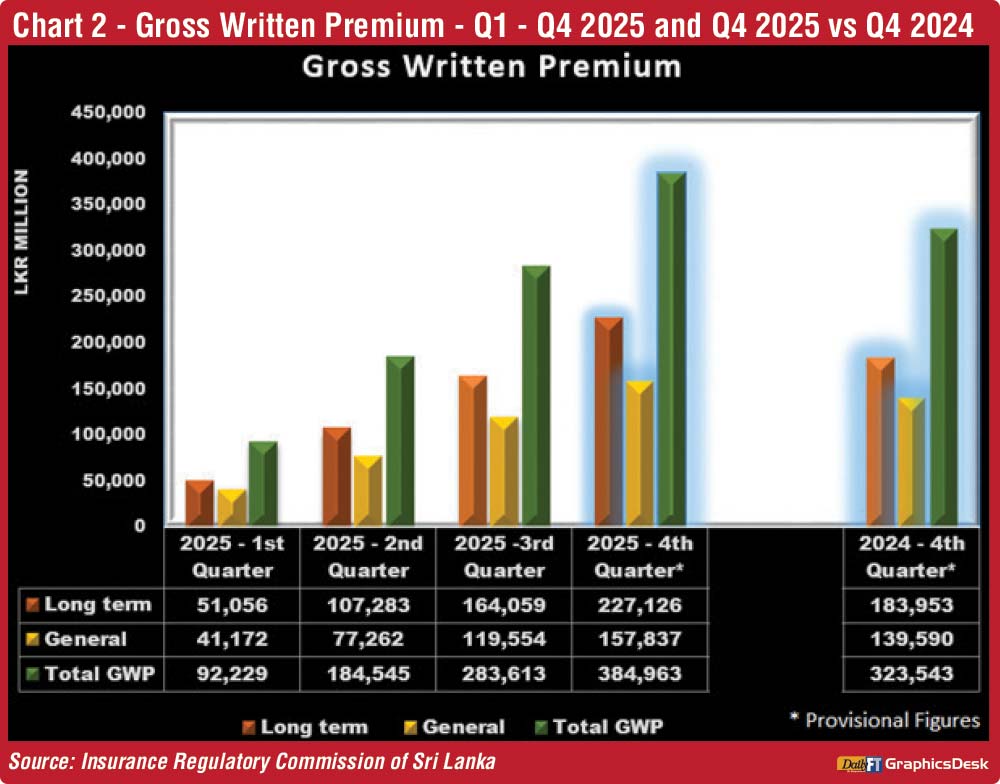

As shown in Chart 2, the Gross Written Premium for the fourth quarter of 2025 stood at Rs. 384,963 million, marking a 19% increase compared to Rs. 323,543 million recorded in the fourth quarter of 2024. This reflects a year-on-year growth rate of 18.98%.

The Long-Term Insurance Business contributed significantly to this growth, recording a GWP of Rs. 227,126 million in 4Q 2025, representing a substantial increase of 23.47% from Rs. 183,953 million in the corresponding quarter of 2024.

Conversely, the General Insurance Business recorded moderate growth, with GWP at Rs. 157,837 million in the fourth quarter of 2025, representing an increase of 13.1% compared to Rs. 139,590 million during the same period in 2024.

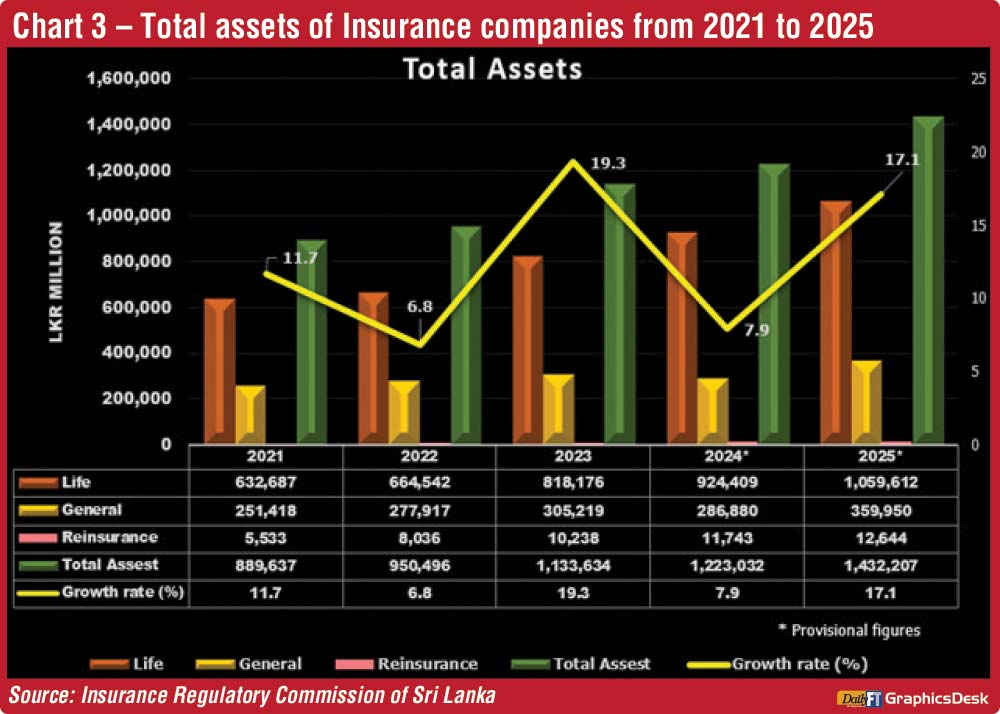

Total assets

Chart 3 illustrates the total assets of insurance companies in Sri Lanka from 2021 to 2025. The industry’s total assets grew significantly, increasing from Rs. 889,637 million in 2021 to Rs. 1,432,207 million by the end of 2025.

The Long-Term (Life) Insurance sector recorded substantial asset growth, rising from Rs. 632,687 million in 2021 to Rs. 1,059,612 million in 2025. Meanwhile, the General Insurance sector recorded moderate growth, with assets increasing from Rs. 251,418 million in 2021 to Rs. 359,950 million in 2025.

Year-on-year asset growth rates reflect an overall positive trend, with notable increase of 19.3% in 2023 and 17.1% in 2025. Although the growth was more moderate in 2022 and 2024, the sector maintained steady asset accumulation, supported by annual growth rates of 11.7% in 2021, 6.8% in 2022, and 7.9% in 2024, contributing to sustained overall growth.

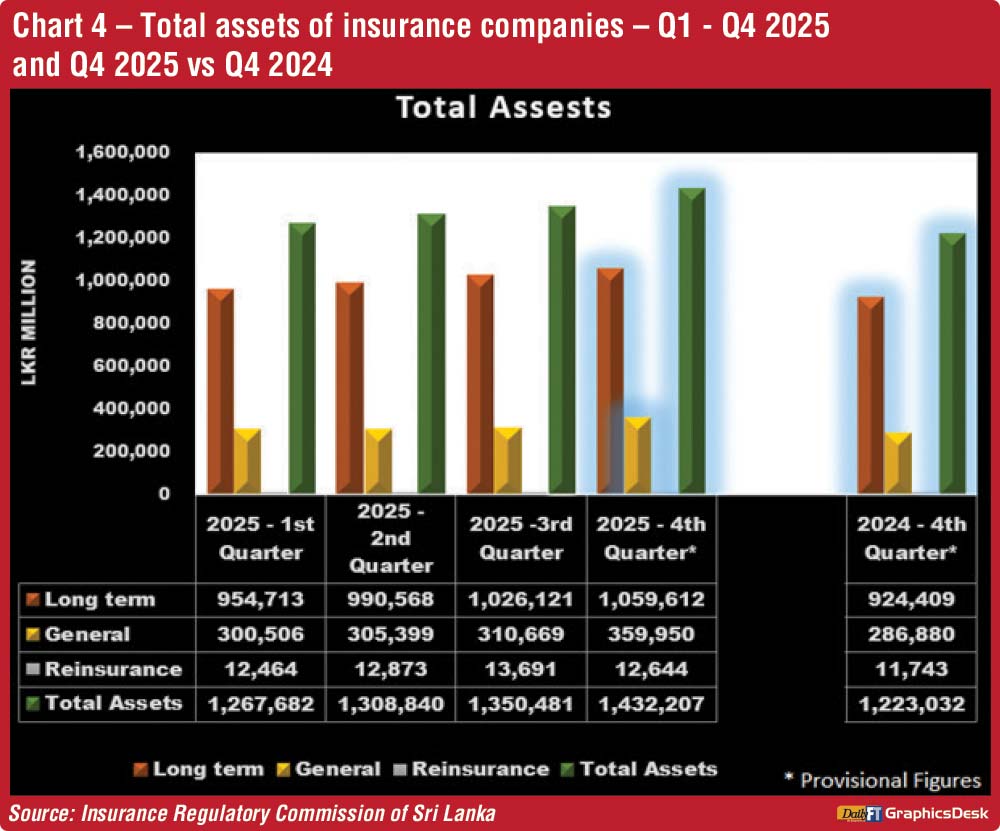

As presented in Chart 4, total assets increased to Rs. 1,432,207 million in the fourth quarter of 2025, representing a robust growth of 17.1% compared to Rs. 1,223,032 million in 4Q 2024. Assets in the Long-Term Insurance business grew by 14.6%, reaching Rs. 1,059,612 million, up from Rs. 924,409 million in the same period of the previous year. The General Insurance business also recorded strong asset growth of 25.5%, with total assets amounting to Rs. 359,950 million compared to Rs. 286,880 million in 4Q 2024.

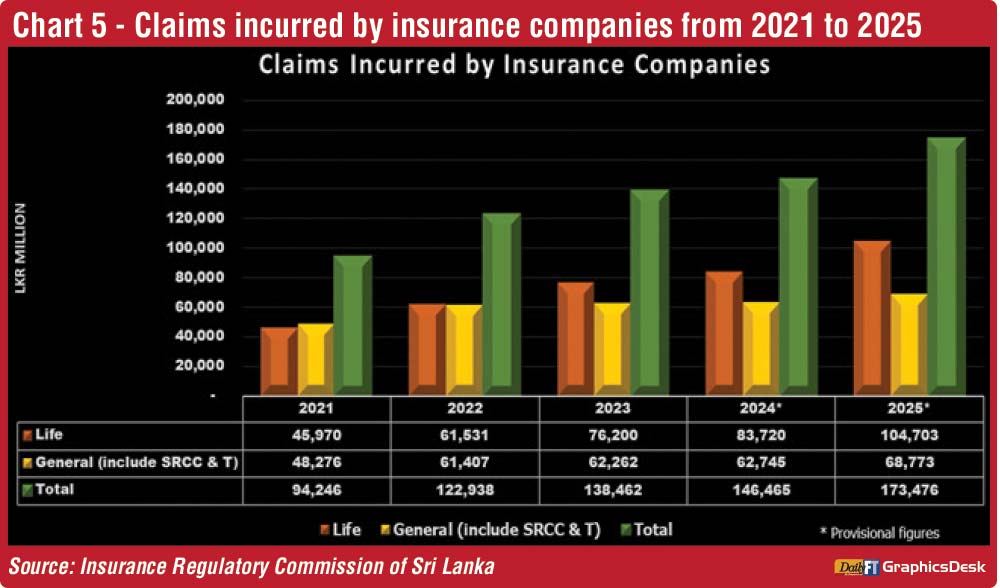

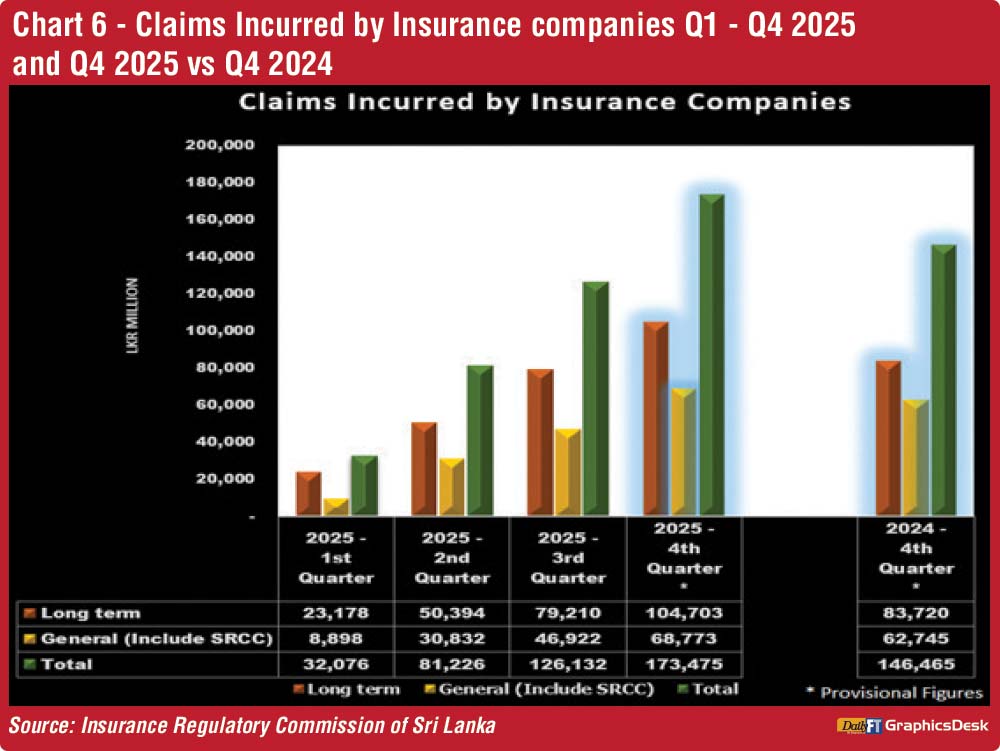

Claims incurred by insurance companies

Chart 5 presents an analysis of claims incurred by insurance companies in Sri Lanka from 2021 to 2025. The Life Insurance sector recorded more than double growth in claims, rising from Rs. 45,970 million in 2021 to Rs. 104,703 million in 2025. This represents a substantial increase of 127.8% over five years, reflecting increased reliance on life insurance products and a corresponding rise in policyholder benefit payments.

Claims incurred in the General Insurance sector also exhibited an upward trend during this period. Starting at Rs. 48,276 million in 2021, claims increased to Rs. 61,407 million in 2022, followed by a further increase to Rs. 62,262 million in 2023. The upward trend continued at a more moderate pace in 2024, before a sharp rise in 2025, with claims reaching Rs. 62,745 million and Rs. 68,773 million, respectively. Overall, total claims increased by approximately 84.07%, from Rs. 94,246 million in 2021 to Rs. 173,476 million in 2025.

As detailed in Chart 6, total claims incurred by both Long-Term and General Insurance businesses in the fourth quarter of 2025 amounted to Rs. 173,475 million, marking an 18.4% increase compared to Rs. 146,465 million in 4Q 2024. Claims from the Long-Term Insurance business, including maturity and death benefits, rose by 25.1 % to Rs. 104,703 million, up from Rs. 83,720 million in the same period of the previous year. Claims from the General Insurance business, covering Motor, Fire, Marine, and other lines, recorded a moderate increase of 9.6%, totaling Rs. 68,773 million compared to Rs. 62,745 million in 4Q 2024.

These figures highlight the growing financial responsibilities borne by the insurance sector in meeting policyholder needs and underscore the importance of sustained operational resilience within the industry.

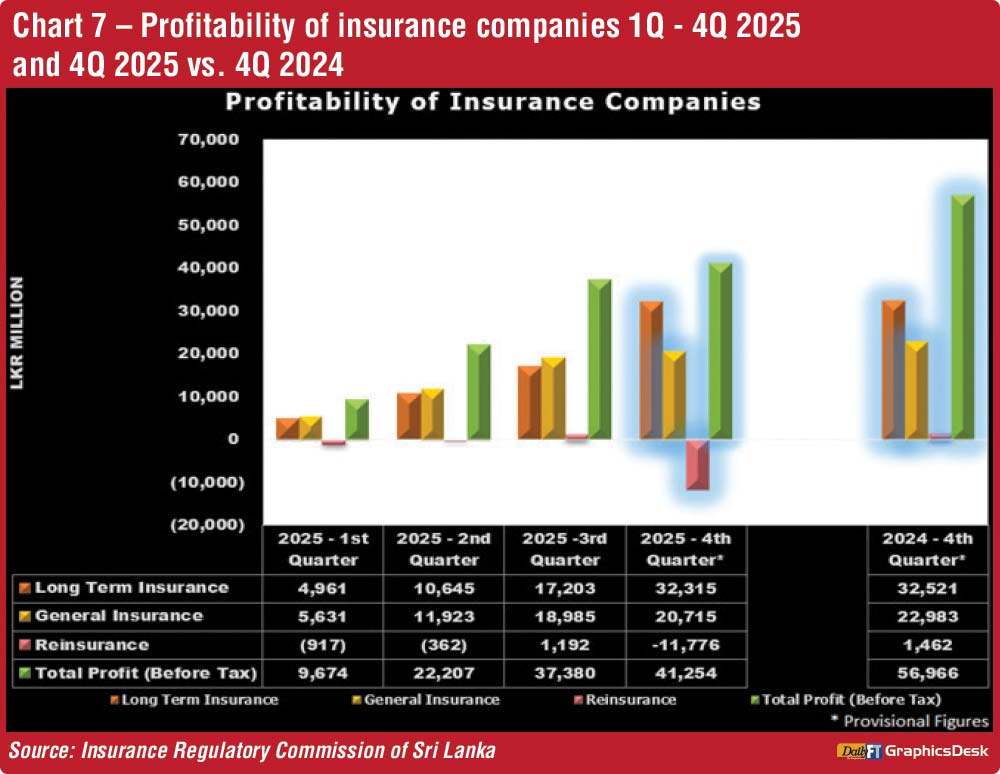

Profit Before Tax of insurance companies

As shown in Chart 7, the insurance industry recorded a decline in total Profit Before Tax (PBT) in the fourth quarter of 2025 compared to the same period in 2024.

The Long-Term Insurance business recorded a decline in PBT, decreasing from Rs. 32,521 million in 4Q 2024 to Rs. 32,315 million in 4Q 2025, representing a decline of 0.63%. The decrease in profitability mainly due to the significant increase in net benefit claims paid, underwriting and acquisition costs, and other expenses, which increased by Rs. 25,755 million (14%), Rs. 8,431 million (36%), and Rs. 8,356 million (17%), respectively, compared to the previous year.

Meanwhile, the General Insurance business also recorded a considerable decline, with PBT decreasing from Rs. 22,983 million in 4Q 2024 to Rs. 20,715 million in 4Q 2025, a decline of 9.87%.

The decline in profitability was mainly due to an increase in net benefit claims paid by Rs. 6,027 million (10%), a decrease in investment income by Rs. 2,262 million, an increase in other operating, investment, and administrative expenses by Rs. 1,338 million, and the impact of the unearned premium reserve compared to 2024.

The reinsurance business recorded a severe decline in PBT, shifting from a profit of Rs. 1,462 million in 4Q 2024 to a loss of Rs. 11,776 million in 4Q 2025, representing a decline of 905.4%.This decline was primarily driven by the increase in the IBNR provision of Rs. 12.4 billion recognised in relation to the Ditwa claim during the last quarter.

Investment in Govt. securities

As at the end of 4Q 2025, the total value of investments in Government Debt Securities amounted to Rs. 661,522 million, representing a significant increase of 8.65% compared to the Rs. 608,842 million recorded in the corresponding period of 4Q 2024. The Long-Term Insurance business recorded growth, with its investments increasing by 11.26% to Rs. 550,842 million, accounting for 56.91% of total industry investments. In contrast, the General Insurance business recorded a decline by 2.7% in its investments in Government Debt Securities, which amounted to Rs. 110,680 million and represented 53.68% of its total investments.

Insurance brokers

The insurance brokering segment demonstrated robust growth. As of 31 December 2025, 82 insurance brokering companies were registered with the Commission. The total assets of these brokers increased substantially to Rs. 21,700 million by the end of 4Q 2025, compared to Rs. 16,723 million in 4Q 2024, signifying a strong growth rate of 29.76%.

(The review was compiled by the Insurance Regulatory Commission of Sri Lanka)