Wednesday Jul 15, 2026

Wednesday Jul 15, 2026

Tuesday, 14 July 2026 06:32 - - {{hitsCtrl.values.hits}}

The insurance industry recorded steady growth in Gross Written Premiums (GWP) during the first quarter of 2026 compared with the corresponding period of 2025, reflecting the sector’s continued resilience and its ability to operate effectively despite the prevailing economic and environmental challenges

Insurance Regulatory Commission of Sri Lanka said the industry demonstrated resilience during the first quarter of 2026, recording steady performance despite the prevailing macroeconomic conditions and the impact of Cyclone Ditwah, which affected several provinces across the country in late 2025.

The industry’s performance should also be viewed in the context of the cumulative effects of challenges, including the COVID-19 pandemic, the 2022 economic crisis and political instability, high inflation, currency depreciation, and recurring climate-related events such as floods and droughts, which have continued to influence the operating environment of the insurance sector.

During the review period, the insurance industry continued to provide financial protection to policyholders through the settlement of valid insurance claims, including claims arising from Cyclone Ditwah. The Insurance Regulatory Commission of Sri Lanka (IRCSL) continued to monitor the industry’s operations to promote the fair and efficient handling of insurance claims and to safeguard the interests of policyholders.

The insurance industry recorded steady growth in Gross Written Premiums (GWP) during the first quarter of 2026 compared with the corresponding period of 2025, reflecting the sector’s continued resilience and its ability to operate effectively despite the prevailing economic and environmental challenges.

As at 31 March 2026, fifteen (15) insurance companies were licensed to conduct Long-Term (Life) Insurance business, while fourteen (14) companies were licensed to conduct General Insurance business in Sri Lanka.

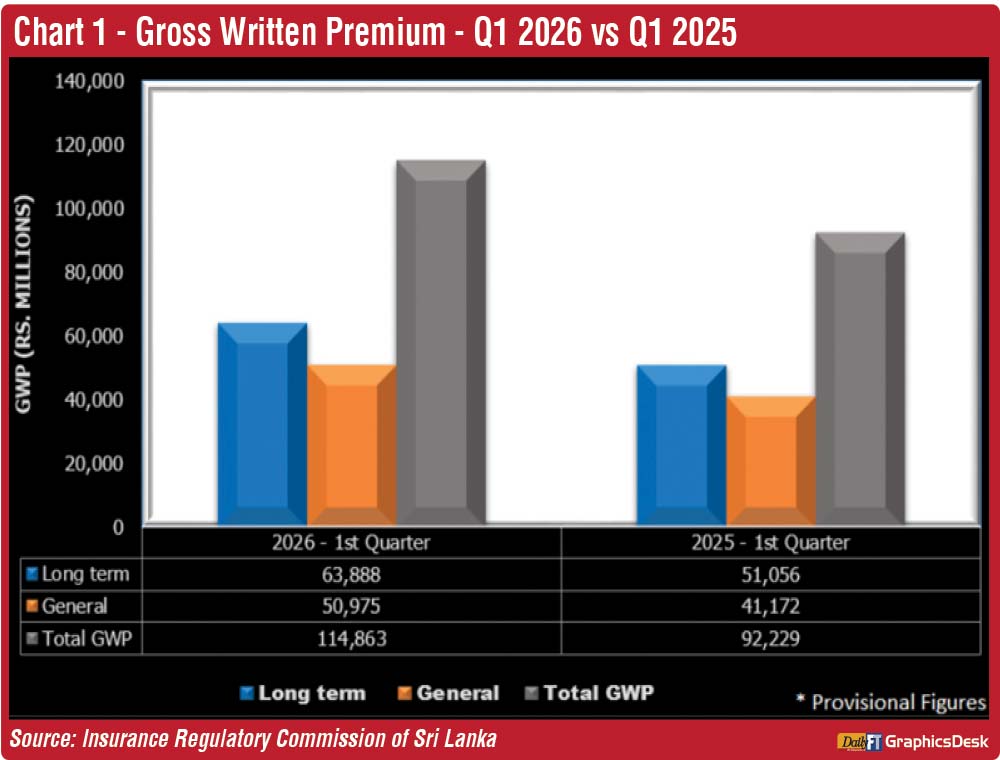

Gross Written Premium (GWP)

Chart 1 presents the performance of the insurance industry during the first quarter of 2026 compared to the corresponding period of 2025.

Total Gross Written Premium (GWP) increased from Rs. 92,229 million in 1Q 2025 to Rs. 114,863 million in 1Q 2026, representing a growth of 24.54%.

The Long-Term (Life) Insurance sector recorded Gross Written Premium of Rs. 63,888 million in 1Q 2026, compared to Rs. 51,056 million in 1Q 2025, reflecting a growth of 25.13%. This performance contributed significantly to the overall growth of the insurance industry during the review period.

The General Insurance sector also recorded positive growth, with Gross Written Premium increasing from Rs. 41,172 million in 1Q 2025 to Rs. 50,975 million in 1Q 2026, representing a growth of 23.81%. This growth reflects the continued expansion of General Insurance business during the review period.

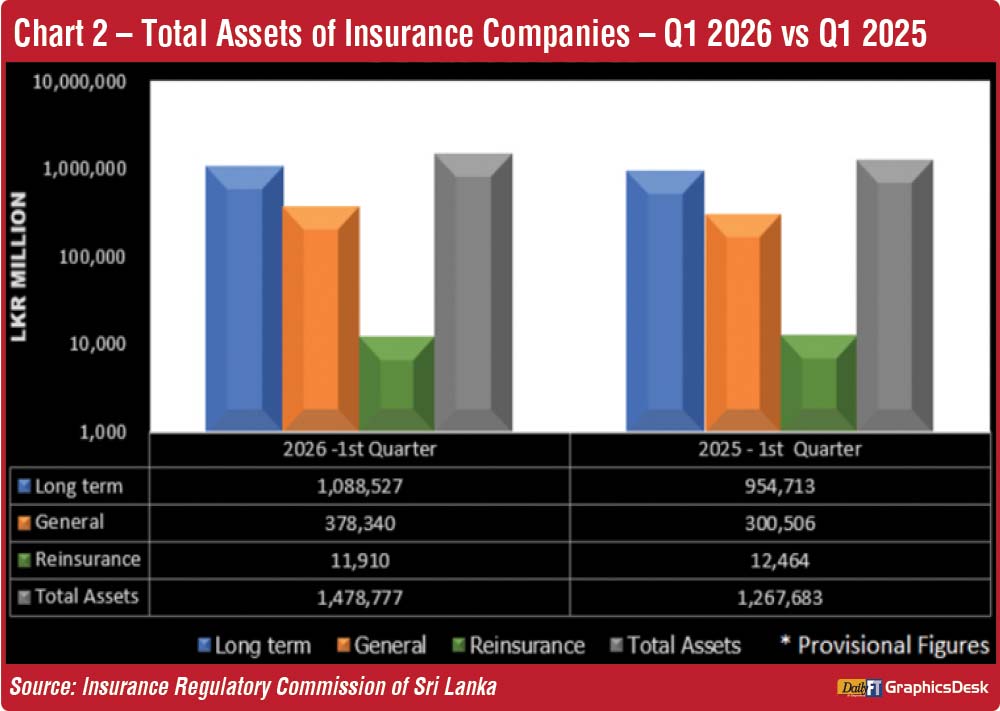

Total assets

Chart 2 presents the total assets of the insurance industry as at 31 March 2026 compared to the corresponding period in 2025.

The insurance industry’s total assets increased from Rs. 1,267,683 million in 1Q 2025 to Rs. 1,478,777 million in 1Q 2026, representing an overall growth of 16.65%.

The Long-Term (Life) Insurance sector recorded total assets of Rs. 1,088,527 million as at 31 March 2026, compared to Rs. 954,713 million as at 31 March 2025, reflecting a growth of 14.02%. The Life Insurance sector continued to account for the largest share of the industry’s total assets.

The General Insurance sector recorded total assets of Rs. 378,340 million as at 31 March 2026, compared to Rs. 300,506 million as at 31 March 2025, representing a growth of 25.90%.

Meanwhile, the Reinsurance sector recorded total assets of Rs. 11,910 million as at 31 March 2026, compared to Rs. 12,464 million in the corresponding period of 2025, representing a decrease of 4.45%.

The increase in total assets reflects the continued growth of the insurance industry during the review period.

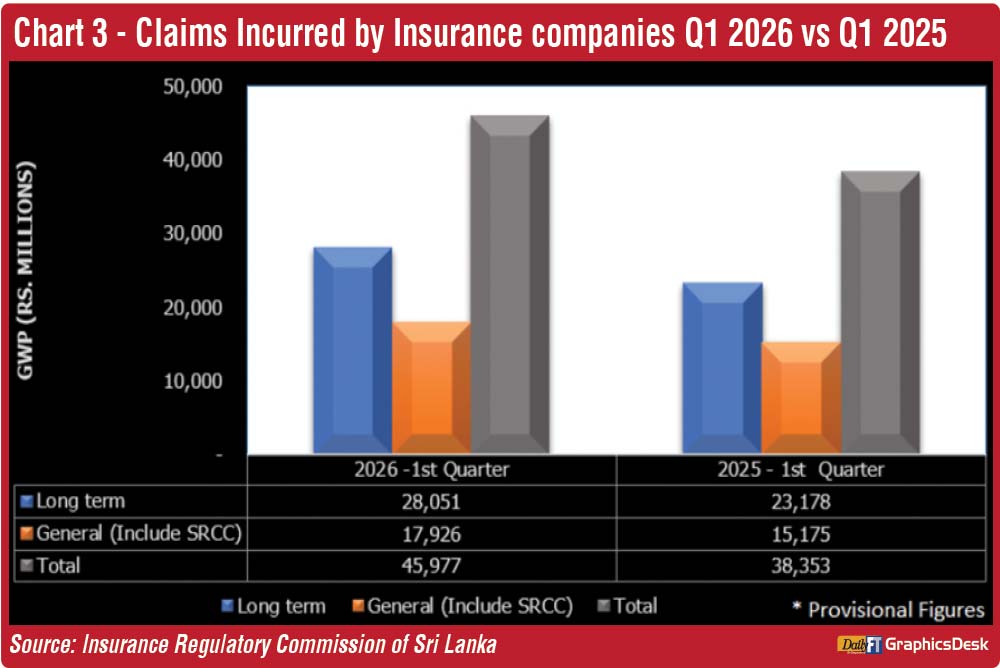

Claims incurred by insurance companies

Chart 3 presents a comparison of claims incurred by insurance companies during the first quarter of 2026 and the corresponding period of 2025.

Total claims incurred increased from Rs. 38,353 million in 1Q 2025 to Rs. 45,977 million in 1Q 2026, representing a growth of 19.88%. The increase reflects the insurance industry’s continued fulfilment of its obligations to policyholders through the settlement of insured claims.

The Long-Term (Life) Insurance sector recorded claims incurred of Rs. 28,051 million in 1Q 2026, compared to Rs. 23,178 million in 1Q 2025, reflecting a growth of 21.03%. The increase in claims is broadly in line with the continued growth of the Life Insurance business during the review period.

The General Insurance sector recorded claims incurred of Rs. 17,926 million in 1Q 2026, compared to Rs. 15,175 million in 1Q 2025, representing a growth of 18.13%. The increase in claims includes settlements arising from insured events during the period, including those associated with Cyclone Ditwah, together with the overall growth of General Insurance business.

Overall, the increase in claims incurred across both sectors demonstrates the insurance industry’s continued commitment to providing financial protection and meeting its contractual obligations to policyholders.

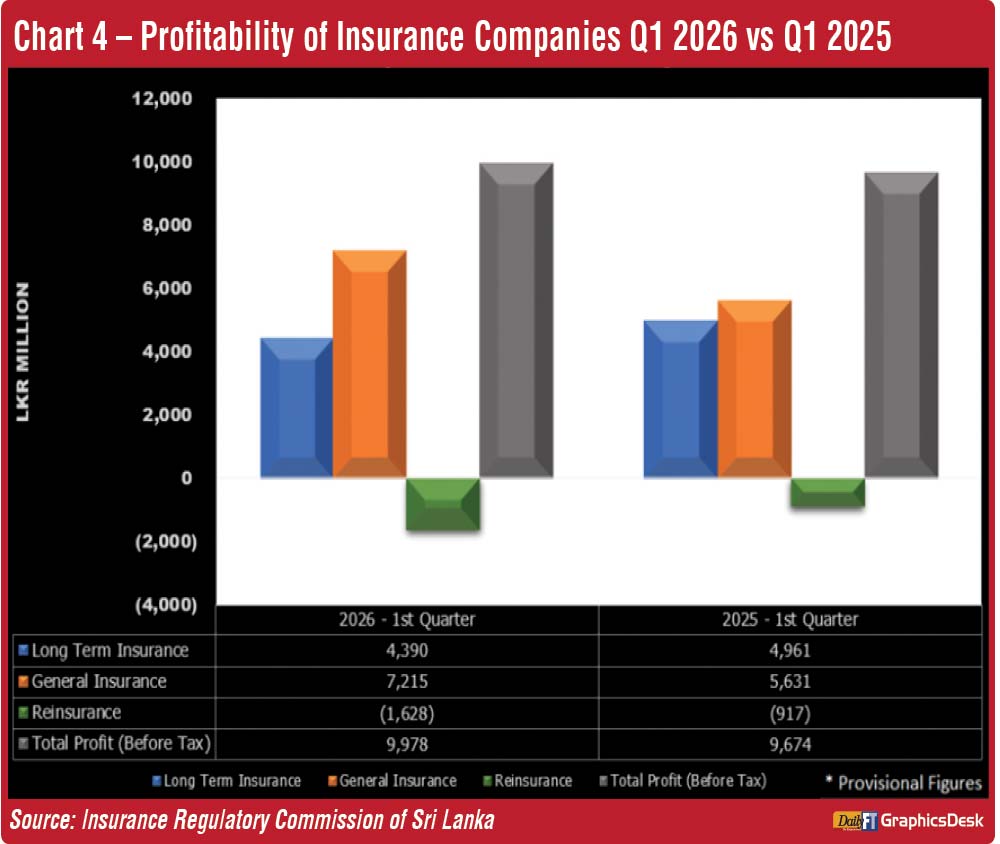

Profit Before Tax of insurance companies

Chart 4 presents the Profit Before Tax (PBT) of the insurance industry for the first quarter of 2026 in comparison to the corresponding period of 2025.

The insurance industry recorded a total Profit Before Tax (PBT) of Rs. 9,978 million during the first quarter of 2026, reflecting a growth of 3.14% compared to Rs. 9,674 million recorded during the corresponding period of 2025.

The Long-Term (Life) Insurance business recorded a PBT of Rs. 4,390 million in 1Q 2026, reflecting a decline of 11.51% from Rs. 4,961 million recorded during 1Q 2025.

In contrast, the General Insurance business recorded a PBT of Rs. 7,215 million during 1Q 2026, reflecting an increase of 28.13% from Rs. 5,631 million recorded during 1Q 2025.

Overall, the insurance industry remained profitable during the review period, although profitability trends differed between the Long-Term (Life) and General Insurance sectors.

Investment in Government debt securities

As at the end of the first quarter of 2026, total investments in Government debt securities amounted to Rs. 668,786 million, reflecting an overall increase of 9.45% compared to Rs. 611,017 million recorded in 1Q 2025.

Investments by the Long-Term Insurance Business in Government Debt Securities amounted to Rs. 556,766 million (1Q 2025: Rs. 499,695 million), representing 56.25% of its total investments and indicating a growth of 11.42%. Meanwhile, the General Insurance Business invested Rs. 112,020 million in Government debt securities (1Q 2025: Rs. 111,322 million), accounting for 53.52% of its total investments and showing a growth of 0.63%.

The increase in Government debt securities investments was primarily driven by the Long-Term Insurance Business, which recorded the highest growth during the period. Government Debt Securities continued to remain a significant component of insurers’ investment portfolios, reflecting the sector’s preference for relatively stable and secure investment instruments to support long-term financial obligations and investment management requirements