Sunday Jul 12, 2026

Sunday Jul 12, 2026

Monday, 6 July 2026 04:42 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

The secondary Bond market witnessed a constructive week, with sentiment improving markedly throughout the week, driven by foreign portfolio allocations towards Sri Lankan Rupee Bonds. The week commenced on the back of a flattened yield curve following the outcome of the bond auctions held on 26 June 26.

The secondary Bond market witnessed a constructive week, with sentiment improving markedly throughout the week, driven by foreign portfolio allocations towards Sri Lankan Rupee Bonds. The week commenced on the back of a flattened yield curve following the outcome of the bond auctions held on 26 June 26.

However, the market subsequently staged a strong two-day rally on Wednesday and Thursday, underpinned by persistent demand from large foreign portfolio buyers. Buying was concentrated primarily on the 15.10.30 (4-year tenor) and 15.03.35 (10-year tenor) maturities. The positive momentum subsequently spilled over to the rest of the yield curve, although the downward adjustment in yields across the remaining maturities was to a lesser extent. The downward rally in the bond market was despite the upward movement in T-Bill yields at the weekly auction. Activity and transaction volumes remained robust throughout the rally, with several sizeable block trades executed.

On Friday, the market paused to consolidate following the sharp gains recorded earlier in the week. Reduced foreign demand and mild profit-taking pressure saw yields edge marginally higher, although overall sentiment remained constructive. In conclusion, secondary market two-way quotes on the 4-year and 10-year bonds were markedly lower, week on week, while the rest of the yield curve noted more modest gains.

Trades were witnessed across the yield curve, with the 15.10.27 maturity changing hands at the rate of 10.50%. In the 2028 space, the 15.03.28, 01.05.28, 01.07.28, 01.09.28 and 15.10.28 maturities traded at the rates of 10.60%, 10.65%, 10.70% and 10.65% each respectively.

Moving into the 2029 segment, the 15.09.29 and 15.10.29 maturities changed hands at the rates of 10.95% and 11.00%–10.97% respectively, while the 15.12.29 maturity traded down from an intraweek high of 11.05% to a low of 10.95%.

In the 2030 space, the 01.03.30 and 15.05.30 maturities changed hands at the rates of 11.15% and 11.15%–11.12% respectively. The 01.08.30 maturity traded down from an intraweek high of 11.35% to a low of 11.23%, while the 15.10.30 maturity traded down from an intraweek high of 11.45% to a low of 11.23%.

Further along the curve, the 15.03.31 and 01.10.32 maturities traded at the rates of 11.30% and 11.55% respectively. The 15.12.32 maturity traded down from an intraweek high of 11.65% to a low of 11.55%. The 01.11.33 maturity traded down from an intraweek high of 11.70% to a low of 11.65%, while the 15.06.34 maturity traded down from a high of 11.75% to 11.67%.

At the longer end, the 15.03.35 maturity traded down from an intraweek high of 11.85% to a low of 11.70%, while the 15.08.36 maturity traded down from an intraweek high of 11.94% to a low of 11.90%.

At the weekly Treasury bill auction held last Wednesday, weighted average yields increased across all three maturities for a second consecutive week. The sharpest upward adjustment was recorded at the shorter end, with the 91-day and 182-day bills rising by 09 basis points each to 10.23% and 10.30%, respectively. In comparison, the 364-day bill edged up by just 03 basis points to 10.20%, reinforcing the recent front-end bias in the repricing of the Treasury bill yield curve.

The auction successfully raised the entire Rs. 100 billion offered at the first phase of competitive bidding. However, the bulk of the accepted amount was raised from the 91-day tenor, which saw acceptance exceed its offered amount, while the 182-day and 364-day maturities raised less than their respective offered amounts. An additional amount of Rs. 7.73 billion was raised at its phase 2 of the auction on the 182 day and 364-day bills.

In the money Market, the total outstanding liquidity surplus was recorded at Rs. 128.47 billion, improving notably by doubling against its previous weeks Rs. 61.62 billion. The weighted average interest rates on Call Money and Repo stood at 9.20% and 9.24% respectively at the close of the week as against the previous week’s closing levels of 9.22% and 9.24%.

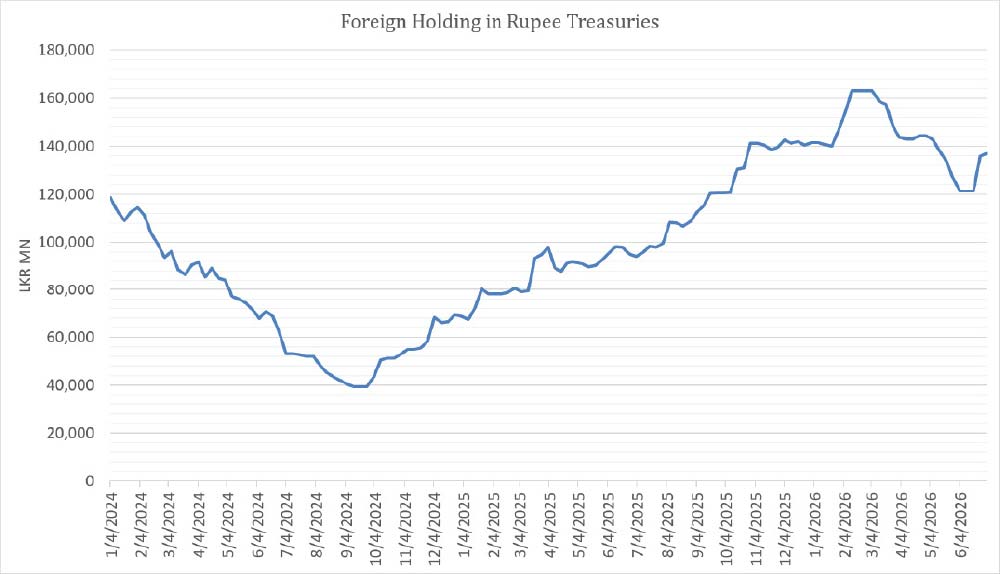

The foreign demand for rupee-denominated government securities continued to increase, with holdings rising for a fourth consecutive week. The week ending 02nd July recorded a net inflow of Rs. 1 billion, driving total foreign holdings up to Rs. 136.86 billion.

In the Forex market, the USD/LKR rate on spot contracts was seen closing the week appreciating to Rs. 335.20/335.30 as against its previous weeks closing of Rs. 336.40/336.70. This was subsequent to trading from at an intraweek high of Rs. 335.20 and a low of Rs.336.30.

The daily USD/LKR average traded volume for the first four trading days of the week stood at

$ 102.99 million.

(References: Public Debt Management Office - Ministry of Finance, Central Bank of Sri Lanka, Bloomberg E-Bond Trading Platform, Money Broking Companies)