Saturday Jun 13, 2026

Saturday Jun 13, 2026

Monday, 16 February 2026 01:13 - - {{hitsCtrl.values.hits}}

Liquidity remains heavily plus at Rs. 299 b; highest level in over 11 years

Liquidity remains heavily plus at Rs. 299 b; highest level in over 11 years

T-Bill rates drop for 4th straight week at auction

Rs. 51 b T-Bond auction records bullish outcome

Secondary Bond market extends rally; yields trend lower

By Wealth Trust Securities

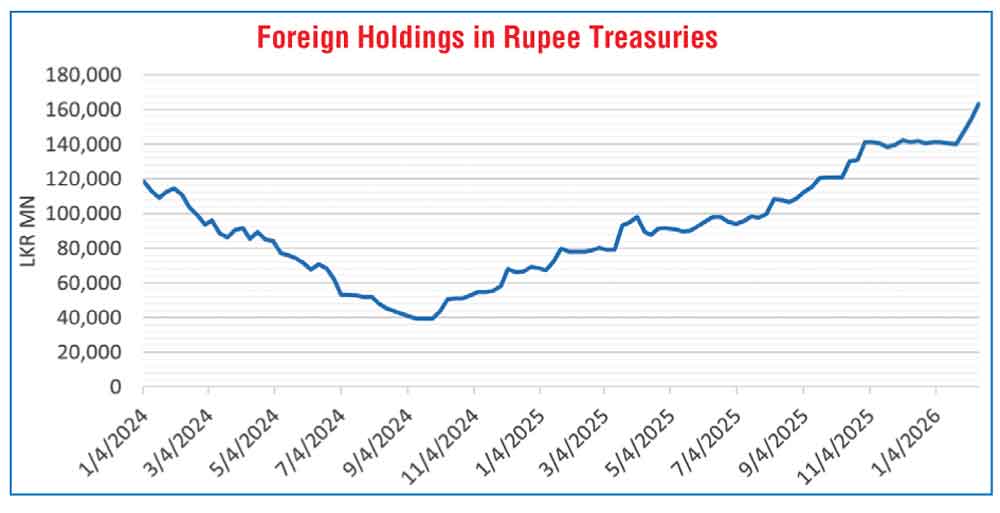

Foreign holdings of rupee-denominated Government securities rose for a third consecutive week, recording a sizeable net inflow of Rs. 9.21 billion and surpassing the Rs. 160 billion mark. As a result, total foreign holdings increased to Rs. 63.23 billion during the week ended 12 February, reflecting a 6% week-on-week increase and reaching the highest level in nearly two-and-a-half years, since early August 2023.

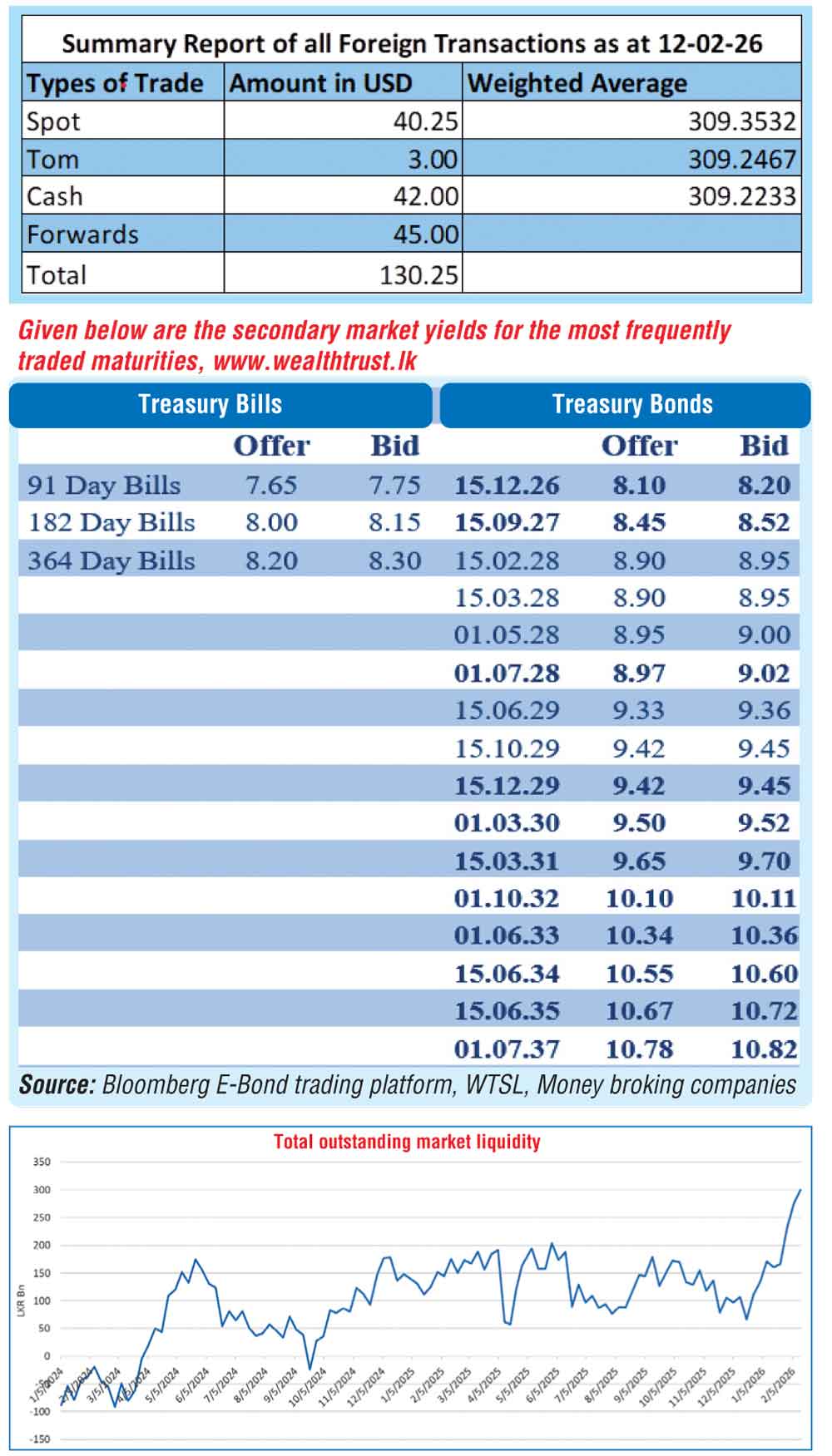

In the money market, the total outstanding liquidity surplus in the inter-bank market continued to remain elevated and stood at Rs. 299.68 billion as at the week ending 13 February 2026, increasing from Rs. 275.19 billion recorded in the previous week. Liquidity was seen rising to the highest level in over 11 years – since 23 January 2015. This in turn saw the weighted average interest rates on Call Money and Repo to drop lower to 7.66% and 7.70%, respectively, at the close of the week ending 13 February against its previous week’s closings of 7.70% and 7.75%. Interestingly on Friday, the Domestic Operations Department (DOD) of the Central Bank of Sri Lanka was seen draining out an amount of Rs. 20 billion by way of overnight repo auction at a weighted average rate of 7.65%.

Against this backdrop the weekly Treasury Bill auction held last Wednesday (11 February), registered a positive outcome, with yields continuing to trend downward. The weighted average rates declined across all maturities for the fourth consecutive week. The shorter-tenor maturities saw a more pronounced downward adjustment, with the rate on the 91-day Bill declining by 8 basis points to 7.72% and the rate on the 182-day bill dropping by 10 basis points to 8.07%. The 364-day bill saw its yield ease more modestly, by 2 basis points to 8.31%. The auction was fully subscribed, raising the entire Rs 90.00 billion offered. Total bids reached 3.16 times the offered amount.

This was followed by a Treasury Bond auction held last Thursday (12 February), which delivered a bullish outcome. The Public Debt Management Office successfully raised the full Rs. 51 billion on offer across two available maturities. Weighted average yields were in line with or below prevailing market levels, while demand was robust, reflected by a bid-to-acceptance ratio of 4.86 times.

Maturity wise: The 01.03.30 maturity was fully taken up at the first phase at a weighted average yield (WAYR) of 9.52%, in line with pre-auction levels; the newly introduced 15.08.36 maturity was also fully subscribed at the first phase at a WAYR of 10.73%, coming in well below comparable market benchmarks.

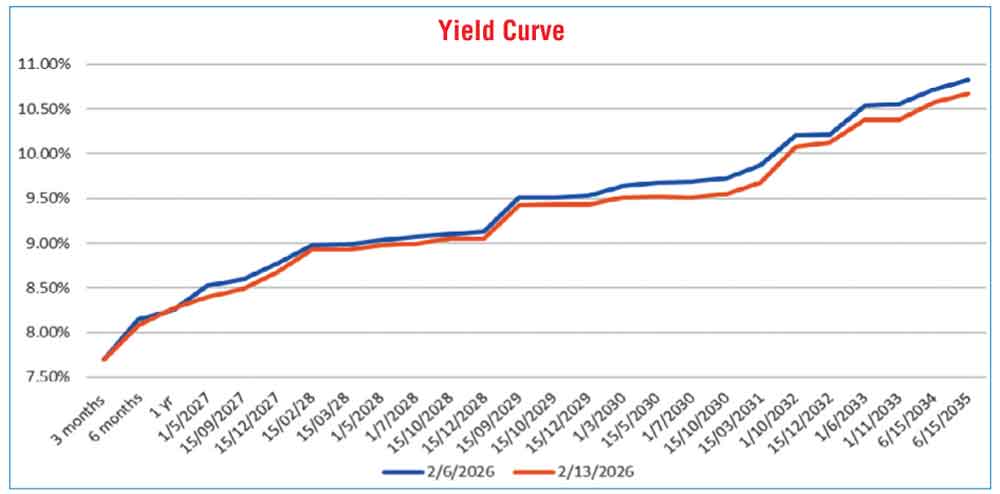

The secondary Bond market remained firmly bullish throughout last week, with rates trending lower across the yield curve amid robust trading volumes. The decline in yields was more pronounced at the belly-to-long end, particularly across the 2029–2037 maturities, driven by strong investor demand. Market sentiment was supported by elevated liquidity conditions, compressed money market rates, and bullish outcomes at back-to-back primary auctions. While the short end also edged lower, movements there were relatively modest compared to the rest of the curve. Overall, secondary Bond market two-way quotes closed lower week on week, resulting in a downward shift of the yield curve.

In terms of the Secondary Bond market trade summary:

During the week, the 01.08.26 maturity traded down from 8.12% to 8.10%, the 01.05.27 maturity traded down from 8.50% to 8.40% and the 15.09.27 maturity traded down from 8.64% to 8.50%. Moving into the 2028 tenors, the 15.10.28 maturity traded down from 9.17% to 9.05%, while the 15.12.28 maturity traded at a low of 9.12%.

Further along the curve, the 15.06.29 maturity traded down from 9.45% to 9.34%. The 15.09.29 maturity traded down from 9.48% to 9.41%, while the 15.10.29 maturity traded down from 9.50% to 9.43%. The 15.12.29 maturity traded down from 9.55% to 9.42%. On the medium end, the 01.03.30 maturity traded down from 9.68% to 9.50%, while the 01.07.30 maturity traded down from 9.68% to 9.55%. The 15.10.30 maturity traded down from 9.65% to 9.55%. The 15.03.31 maturity traded down from 9.88% to 9.70%.

Further out the curve, the 01.10.32 maturity traded down from 10.15% to 10.10%, while the 15.12.32 maturity traded down from 10.18% to 10.12%. The 01.06.33 maturity traded down from 10.50% to 10.35%, while the 01.11.33 maturity traded down from 10.46% to 10.35%.

At the long end, the 15.06.34 maturity traded down steeply from an intraweek high of 10.70% to 10.52%, while the 15.06.35 maturity also registered a notable decline from 10.83% to 10.68%. The 01.07.37 maturity traded down from 10.98% to 10.80%, while the 15.08.39 maturity traded down from 11.02% to 10.90%.

The daily secondary market Treasury Bond/Bill transacted volumes for the first four days of the week averaged at Rs. 26.15 billion.

Forex market

In the Forex market, the USD/LKR rate on spot contracts was seen closing the week depreciating to Rs. 309.20/309.25 as against the previous week’s closing level of Rs. 309.37/309.42. This was subsequent to trading at a high of Rs. 309.19 and a low of Rs. 309.57.

The daily USD/LKR average traded volume for the first four trading days of the week stood at $ 119.15 million.

(References: Public Debt Management Office - Ministry of Finance, Central Bank of Sri Lanka, Bloomberg E-Bond Trading Platform, Money Broking Companies)