Thursday Jun 04, 2026

Thursday Jun 04, 2026

Monday, 9 February 2026 00:58 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

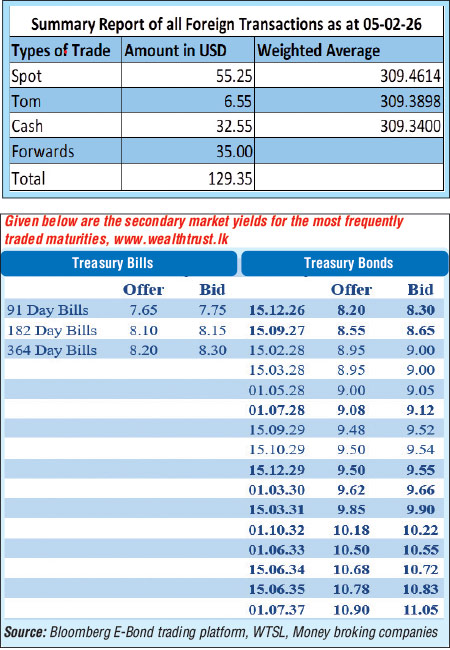

The foreign holdings of rupee-denominated Government securities surged upwards for the second consecutive week, recording a sizeable net inflow amounting to Rs. 7.46 billion and breaking the Rs. 150 billion threshold.

The foreign holdings of rupee-denominated Government securities surged upwards for the second consecutive week, recording a sizeable net inflow amounting to Rs. 7.46 billion and breaking the Rs. 150 billion threshold.

Consequently, total holdings increased to Rs. 154.02 billion during the week ending 5 February, reaching the highest level in over two years – since mid-October 2023. This extends the U-shaped recovery in foreign holdings, registering a 291% increase and rebounding from the low of Rs. 39.38 billion seen during mid-September 2024.

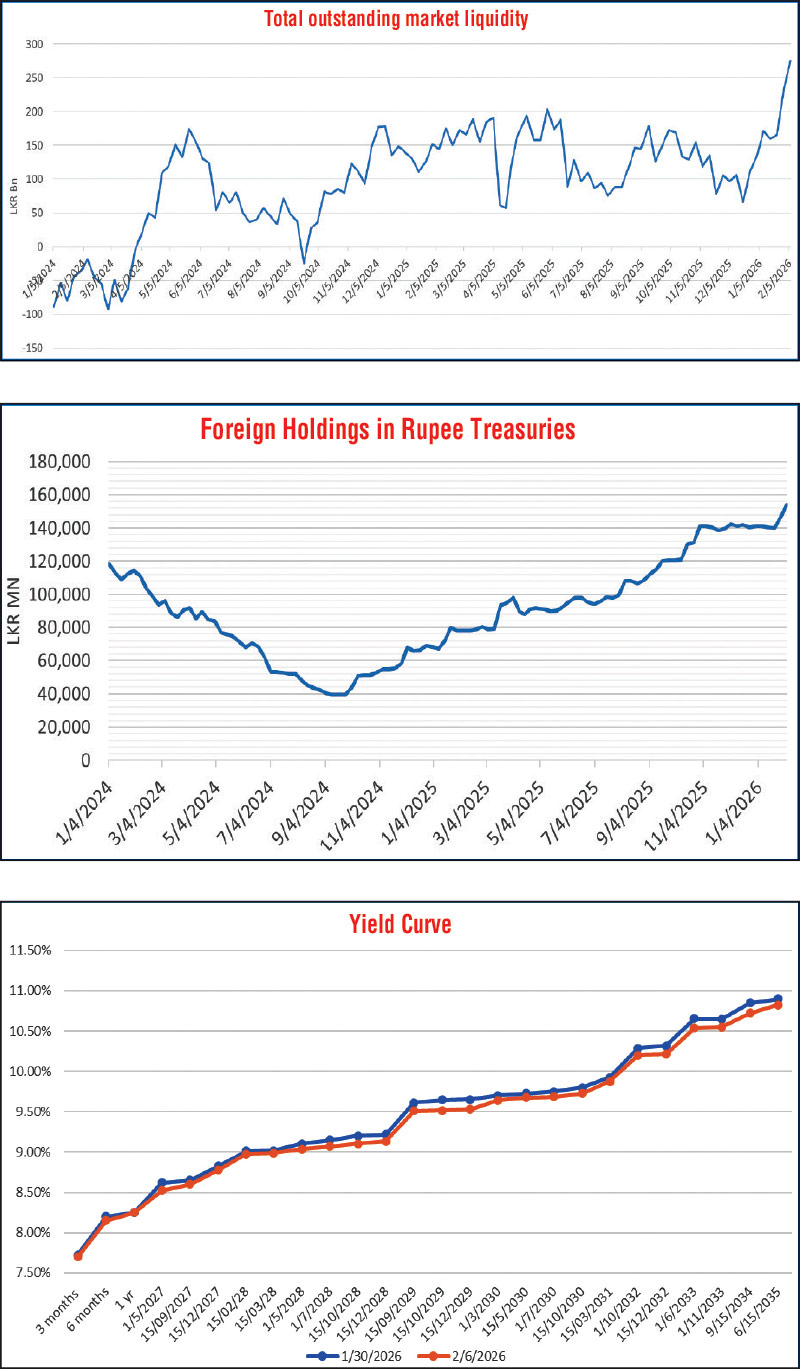

In the money market, the total outstanding liquidity surplus in the inter-bank market continued to remain elevated and stood at Rs. 275.19 billion as at the week ending 6 February 2026, increasing from Rs. 233.13 billion recorded in the previous week.

Liquidity was seen rising to the highest level in almost 11 years – since 13 March 2015. This in turn saw the weighted average interest rates on Call Money and Repo remain compressed at 7.70% and 7.75% respectively, at the close of the week ending 6 February against the previous week’s closings of 7.70% and 7.72%.

With the target average weighted call money rate tightly aligning with the Overnight Policy rate of 7.75%, easing notably from the temporary dislocation observed in December where Call Money and Repo rates were recorded at 8.04% and 8.06%, respectively.

Against this backdrop, the weekly Treasury Bill auction held last Tuesday (3) registered a positive outcome and saw yields continue to trend downwards. Accordingly, weighted average rates registered declines across all maturities for the third consecutive week.

The rate on 91-day Bill declined 4 basis points to 7.80%, while the rate on the 182-day Bill dropped 09 basis points to 8.17%. The 364-day Bill saw its yield ease by 3 basis points to 8.33%. However, the auction was undersubscribed, raising only Rs. 89.82 billion or 74.85% out of the Rs. 120 billion offered at the first phase in competitive bidding.

Nevertheless, demand extended to the second phase where Rs. 42.18 billion was raised, out of the total market subscription of a staggering Rs. 158.88 billion. Accordingly, the aggregate accepted amount of the issuance was Rs. 132 billion – not only bridging the shortfall at the first phase but also raising an additional 10% on top.

Meanwhile, the secondary Bond market sustained a strong bullish tone throughout last week, supported by elevated system liquidity and declining money market and T-Bill rates. Early in the week, yields edged lower on selected tenors, led by concentrated demand on the 2029 segment, while the broader yield curve remained largely range-bound. As sentiment improved, trading interest progressively shifted further along the curve, with investors seeking to capitalise on the prevailing steepness.

Mid-week activity saw increased focus on the belly of the curve, as participants targeted higher carry and roll-down opportunities. Persistently high excess liquidity continued to suppress and anchor short-end yields, prompting market participants to extend duration. Strong and consistent demand was observed across 2029–2033 tenors, with market activity and transaction volumes remaining healthy.

Bullish momentum strengthened towards the latter part of the week, reaching a crescendo, with aggressive buying interest extending from the belly into the long end of the curve. Yields declined further across 2029–2035 maturities as investors moved into higher relative value opportunities.

In summary, the rally was supported by elevated trading volumes and sustained liquidity-driven optimism. Compressed short-term rates and the full subscription at the second phase of the T-Bill auction further strengthened market confidence. In addition, demand–supply dynamics supported buying interest, as February is scheduled to see relatively low issuance at Treasury Bond auctions. As a result, secondary Bond market two-way quotes were seen closing lower, and the yield curve was observed registering a downward shift week-on-week.

In terms of the secondary Bond market trade summary: During the week, the 15.01.27 maturity traded at 8.41%. The 01.05.27 maturity traded down from an intraweek high of 8.60% to a low of 8.50%, and the 15.09.27 maturity traded down from 8.68% to 8.60%.

Moving into the 2028 tenors, the 15.02.28 maturity traded down from 9.02% to 8.97%, while the 15.03.28 maturity traded down from intraweek high of 9.04%% to a low of 9.00%. The 01.05.28 maturity traded down the range of 9.12%–9.02%, while the 01.07.28 maturity traded within 9.14%–9.08%. The 01.09.28 maturity traded down from 9.16%-9.10%, while the 15.12.28 maturity traded from 9.20% to 9.17%.

Further along the curve, the 15.06.29 maturity traded down from an intraweek high of 9.55% to a low of 9.45%. The 15.09.29 maturity traded down from 9.60% to 9.50%, while the 15.10.29 maturity traded down from 9.60% to 9.50%. The 15.12.29 maturity traded down from 9.60% to 9.51%.

On the medium-to-long end, the 01.03.30 maturity traded down from 9.70% to 9.62%, while the 01.07.30 maturity traded down the range of 9.75%–9.68%. The 15.03.31 maturity traded down from intraweek highs of 9.95% to a low of 9.88%.

Further out the curve, both the 01.10.32 and 15.12.32 maturities traded down the range of 10.32%–10.20%. The 01.06.33 maturity traded down the range of 10.65%–10.55% while 01.11.33 maturity traded at a low of 11.60%. The 15.06.34 maturity traded down from 10.85% to 10.70%, while at the long end, the 15.06.35 maturity traded down from intraweek highs of 10.91% to a low of 10.80%.

These developments come ahead of a relatively small Treasury Bond Auction with a total offered amount of Rs. 51 billion offered across 4-year and 10-year tenor maturities, due to be held on 12 February (this Thursday), as per the Tentative Treasury Bond and Treasury Bill Issuance/Settlement Calendar February – April 2026 by the Public Debt Management Office.

The daily secondary market Treasury Bond/Bill transacted volumes for the first four days of the week averaged at Rs. 28.11 billion.

Forex market

In the Forex market, the USD/LKR rate on spot contracts was seen closing the week depreciating to Rs. 309.37/309.42 as against the previous week’s closing level of Rs. 309.25/309.35. This was subsequent to trading at a high of Rs. 309.30 and a low of Rs. 309.60.

The daily USD/LKR average traded volume for the first four trading days of the week stood at $ 91.53 million.

(References: Public Debt Management Office - Ministry of Finance, Central Bank of Sri Lanka, Bloomberg E-Bond Trading Platform, Money Broking Companies)